Foreign pensions refer to retirement savings plans established and managed outside the United States. These include government-sponsored pensions, employer-provided retirement plans, or individual retirement accounts set up in foreign countries. Like US-based retirement plans, foreign pensions aim to provide financial security during retirement. Due to the global reach of the US tax system, understanding the tax implications of foreign pensions is crucial. The United States requires citizens and residents to report and pay taxes on worldwide income, including foreign pensions. Failure to report this income can result in penalties and interest. Additionally, foreign pension income might be subject to double taxation—by the source country and the US. However, tax treaties between the US and other countries often provide provisions to mitigate or eliminate this issue. Taxpayers must navigate these treaties correctly to benefit from potential tax relief. A solid grasp of these rules is essential for compliance and tax optimization. The US tax system operates on a worldwide income basis, meaning US citizens and residents must report and pay taxes on all income, regardless of its origin. This includes income from foreign pensions. Whether you are a US citizen living abroad or a resident alien with foreign pension income, the IRS expects you to include this income on your US tax return. Foreign pensions can originate from various sources, including employer-sponsored plans, government pensions, and private retirement accounts. The IRS does not differentiate between these sources when it comes to taxability. All are treated as ordinary income, similar to distributions from US-based pensions, IRAs, or 401(k) plans. However, one must consider the nuances of foreign pension plans, as their structures and the tax treatment in their country of origin can vary significantly. For example, some countries allow for tax-free pension contributions or tax-free growth within the pension account, which might complicate the US tax treatment. Contributions to foreign pension plans can be made with pre-tax or after-tax dollars. Suppose contributions were made with pre-tax dollars (i.e., the contributions were excluded from taxable income in the foreign country). In that case, the entire distribution from the pension is typically taxable in the US. If contributions were made with after-tax dollars (i.e., taxed when contributed), only the earnings portion of the distribution is taxable. The growth or earnings within the foreign pension plan is usually taxable upon distribution. This includes interest, dividends, capital gains, and any other income generated within the pension plan. The Foreign Tax Credit (FTC) allows US taxpayers to offset foreign taxes paid on foreign pension income against their US tax liability. This credit is claimed on Form 1116 and can significantly reduce or eliminate double taxation. There are limitations and restrictions on the FTC and deductions for foreign taxes paid. For example, the FTC cannot exceed the amount of US tax attributable to foreign income, and certain types of income may be excluded from the FTC calculation. Tax treaties between the US and foreign countries may provide specific provisions that affect the taxable amount. Some treaties allow for partial or full exemption of foreign pension income, which can significantly impact the tax treatment. The primary US individual income tax return form where foreign pension income is reported. Foreign pension income should be included in the total income reported on Line 4c (IRA distributions) or Line 5a (pensions and annuities), depending on the type of pension. If the value of your specified foreign financial assets exceeds certain thresholds, you must file Form 8938 (Statement of Specified Foreign Financial Assets). This form provides the IRS with detailed information about your foreign financial accounts, including pension plans. To claim the Foreign Tax Credit for any foreign taxes paid on your pension income, you need to file Form 1116. This form helps you calculate the amount of foreign tax credit you can claim, reducing your US tax liability. If you are claiming benefits under a tax treaty, you may need to file Form 8833 (Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b)). This form discloses the treaty-based position and provides details about the treaty provisions you are claiming. Essential documents include statements from the foreign pension plan that detail distributions and contributions, proof of foreign taxes paid, and records of currency conversion rates used to report the income in US dollars. Additionally, copies of relevant tax treaty forms or statements, like IRS Form 8833, are necessary if claiming benefits under a tax treaty. These documents ensure accurate reporting, compliance with IRS regulations, and the ability to benefit from tax treaty provisions fully. The IRS requires all foreign income to be reported in US dollars. It allows the use of either the yearly average exchange rate or the spot rate on the date of each transaction. The yearly average exchange rate simplifies reporting for regular payments by averaging exchange rate fluctuations over the year. In contrast, the spot rate provides precise conversion for one-time or lump-sum distributions, reflecting the exact value at the time received. Choosing and consistently using the appropriate method is vital for accuracy. Detailed records of exchange rates and calculations should be maintained to substantiate reported amounts and avoid discrepancies. Proper currency conversion ensures compliance with IRS regulations, and consulting tax professionals can help optimize reporting strategies. Reporting foreign pension income requires adherence to specific deadlines to avoid penalties. The standard US tax filing deadline is April 15. However, there is an automatic two-month extension for US citizens and resident aliens living abroad, moving the deadline to June 15. This extension accounts for the complexities and additional time often needed to gather necessary documents from foreign sources. Despite this automatic extension, any taxes owed must still be paid by April 15 to avoid interest charges. If more time is needed beyond the automatic extension, taxpayers can request an additional extension until October 15 by filing Form 4868 (Application for Automatic Extension of Time to File US Individual Income Tax Return). This form must be submitted by June 15. While this extension grants more time to file the return, it does not extend the time to pay any taxes owed, which are still due by the original deadline, to avoid interest and penalties. Given the close economic ties between the two countries, the US-Canada tax treaty is among the most comprehensive and frequently referenced treaties. Under this treaty, pensions and other similar remuneration paid to a resident of one country are generally taxable only in the country of residence. This means that US citizens or residents receiving Canadian pensions would report the income on their US tax return but could avoid Canadian taxation on the same income. The treaty also includes provisions for social security benefits, which are usually taxable only in the country of residence. Taxpayers must file IRS Form 8833 to claim these benefits, disclosing the treaty-based position. The US-UK tax treaty provides detailed provisions regarding the taxation of pensions and annuities. Generally, pensions are taxable only in the country of residence. For example, a US resident receiving a pension from a UK source would report the pension income on their US tax return and not in the UK. This treaty aims to avoid double taxation and may allow for credits or exemptions to reduce tax liability. Social security benefits, government pensions, and other retirement incomes are covered under specific treaty articles, providing clarity and tax relief to individuals who split their working lives between the US and the UK. The US-Germany tax treaty states that pensions and similar remuneration are typically taxable only in the country of residence. This provision helps prevent double taxation for individuals receiving German pensions while living in the US. The treaty includes specific rules for social security benefits and government pensions, usually taxable in the country paying the benefit. This treaty also contains clauses that allow for the avoidance of double taxation through tax credits and deductions, ensuring that individuals do not face excessive tax burdens due to their international retirement income. The US-Australia tax treaty provides that pensions and other similar payments are generally taxable only in the country of residence. However, it includes specific provisions for superannuation payments (Australia's retirement savings system), often requiring careful navigation to avoid double taxation. The treaty aims to facilitate the fair treatment of retirement income, allowing taxpayers to claim foreign tax credits for taxes paid to Australia. Additionally, social security benefits are typically taxable only in the country of residence, further simplifying the tax obligations for retirees with ties to both countries. The US-Japan tax treaty addresses the taxation of pensions and other retirement income, stipulating that such income is generally taxable only in the country of residence. This arrangement helps prevent double taxation and provides clear guidelines for taxpayers. For example, a US resident receiving a Japanese pension would report the income on their US tax return but not in Japan. The treaty also covers social security benefits and government pensions, ensuring these are taxed appropriately and preventing excessive tax burdens. Taxpayers must maintain accurate records and follow specific procedures to claim treaty benefits. Understanding US taxation of foreign pension income is vital for US citizens and residents with international retirement plans. The US tax system requires reporting and taxation of all foreign pension income. Key factors include the nature of contributions, the treatment of earnings, and the potential to claim foreign tax credits. Proper documentation, accurate currency conversion, and timely filing of forms like Form 1040, Form 8938, Form 1116, and Form 8833 are essential. Tax treaties, such as those with Canada, the UK, Germany, Australia, and Japan, help mitigate double taxation, ensuring pension income is taxed fairly. Correctly applying these treaties can significantly reduce tax liabilities. Managing the tax implications of foreign pensions requires careful planning and a solid understanding of tax laws. Consult a financial advisor or tax professional for assistance. They can provide tailored advice based on your specific situation and planning goals.Overview of Foreign Pensions and US Taxes

How US Taxation of Foreign Pensions Work

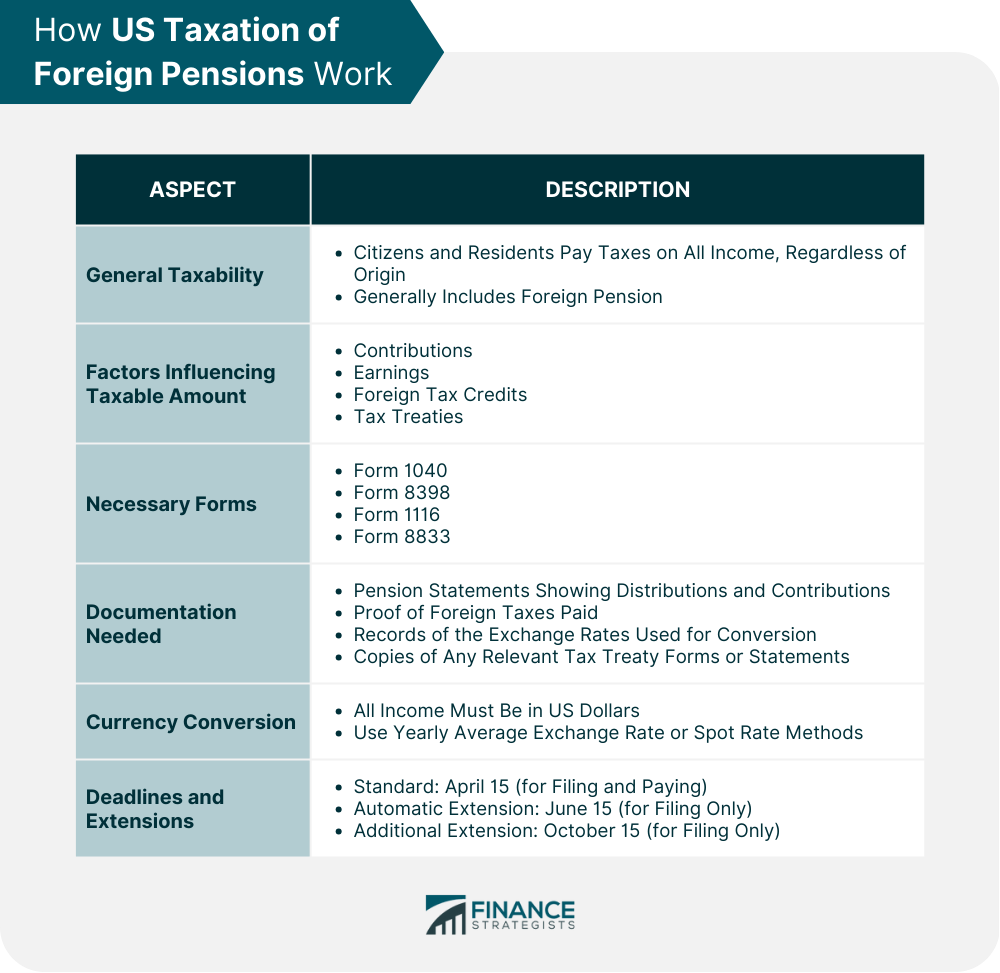

General Taxability

Factors Influencing Taxable Amount

Contributions

Earnings

Foreign Tax Credits

Tax Treaties

Necessary Forms

Form 1040

Form 8938

Form 1116

Form 8833

Documentation Needed

Currency Conversion

Deadlines and Extensions

Examples of Tax Treaties Affecting Foreign Pensions

US-Canada Tax Treaty

US-UK Tax Treaty

US-Germany Tax Treaty

US-Australia Tax Treaty

US-Japan Tax Treaty

Conclusion

Foreign Pensions and US Taxes FAQs

Yes, US citizens and residents must report all worldwide income, including foreign pension income, on their US tax returns.

Double taxation can often be mitigated by claiming foreign tax credits or deductions on your US tax return, or by utilizing provisions in tax treaties between the US and the foreign country.

Key forms include Form 1040 for reporting income, Form 8938 for specified foreign financial assets, Form 1116 for foreign tax credits, and Form 8833 for claiming treaty benefits.

You can use either the yearly average exchange rate or the spot rate on the date of each transaction. It is important to be consistent in your method.

You need pension statements showing distributions and contributions, proof of foreign taxes paid, exchange rate records, and any relevant tax treaty forms.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.