Pension income refers to regular payments made to retirees from a pension fund they contributed to during their working years. It provides financial stability, ensuring that retirees can cover their living expenses even without a regular paycheck from employment. Pension income can come from various sources, including employer-sponsored pension plans, Social Security benefits, and private retirement accounts. Securing a mortgage on a pension is not only possible but also a common scenario for many retirees. Lenders are willing to offer mortgages to retirees who can demonstrate the ability to make regular payments, typically through stable pension income and other retirement funds. The process involves proving the consistency and sufficiency of pension income, maintaining a good credit score, and meeting the lender’s eligibility criteria. While there is no strict age limit for obtaining a mortgage, lenders often have specific guidelines. Typically, lenders are willing to offer mortgages to individuals up to 75. However, some lenders extend this to 85 or older, depending on the applicant's financial health and pension income stability. When exploring mortgage options, retirees should inquire about the maximum age limit, as some lenders may offer products specifically designed for older borrowers. A good credit score leads to favorable mortgage terms. A higher credit score indicates reliable financial behavior and a lower risk for lenders. Retirees should regularly check their credit scores and work on factors that negatively impact their scores. This includes paying down existing debts, making timely payments, and avoiding new debt. Retirees can also improve their credit scores by correcting inaccuracies on their credit reports and maintaining a low credit utilization ratio. Mortgage lenders assess a retiree's ability to consistently make payments by requiring documentation of a steady income. To streamline the application process, retirees should compile evidence of their income sources. This typically includes statements detailing pension payouts, letters confirming Social Security benefits, and annuity contracts. Providing evidence of reliable income is essential in building trust with the lender. Furthermore, some lenders may factor in other income streams, like rental income or investment dividends, as long as they are consistent and supported by documentation. Standard mortgages are available to retirees much like they are to working individuals. These mortgages typically require proof of income, a solid credit score, and a down payment. Retirees often prefer fixed-rate mortgages for their stability and predictability, as they offer a constant interest rate throughout the loan term. It is important to compare different lenders and mortgage products to find the best terms and rates. It's also advisable to consider the loan term. For example, shorter mortgage terms mean higher monthly payments but generally result to lower overall costs. Reverse mortgages are financial tools specifically for older homeowners, usually 62 and above, allowing them to access home equity as cash. This provides an income boost without the need for monthly mortgage repayments. Repayment occurs when the homeowner sells their home, moves out, or passes away. For retirees needing additional funds for living costs, healthcare, or home renovations, reverse mortgages can be a viable option. However, the long-term consequences, such as decreased home equity and potential effects on inheritance, should be understood. It's crucial for retirees to weigh their financial objectives and seek professional financial advice before opting for a reverse mortgage. Equity release options, like home equity loans and lines of credit (HELOCs), offer retirees a way to tap into their home's value without selling. This can be a helpful solution for covering major expenses like home renovations or medical bills. Home equity loans provide a lump sum with fixed monthly repayments, while HELOCs offer flexible access to funds as needed. Before choosing either option, retirees should carefully review the terms, interest rates, and repayment plans. It's also important to be aware of the potential risks involved, such as the possibility of losing your home if the loan is not repaid as agreed. Banks remain a popular choice for securing a mortgage. They provide different mortgage products and typically have robust processes for assessing retiree applications. Building a relationship with a bank, especially where the retiree already holds accounts, can sometimes result in more favorable terms. Retirees should compare mortgage rates, fees, and terms from multiple banks to ensure they are getting the best deal. It's also helpful to work with a loan officer who understands retirees' unique financial situations. Credit unions often provide competitive mortgage rates and personalized service. As member-owned institutions, they usually have better and more flexible terms and are more willing to work with retirees to find suitable mortgage solutions. Credit unions tend to focus on their members' financial well-being, which can result in more favorable loan conditions. If retirees are not already members, they should consider joining a credit union, as the benefits can extend beyond mortgage products to other financial services. Online lenders provide a convenient way to shop for mortgages and compare rates. They often have streamlined application processes and can offer competitive rates. However, it's crucial to research and choose reputable online lenders to avoid potential scams. Retirees should read reviews, check ratings, and verify the lender's credentials before proceeding. Lenders specializing in mortgages for retirees recognize their distinct financial circumstances and provide tailored loan options. Partnering with such a lender can streamline the application process and increase the likelihood of approval. Retirees should consider lenders who have experience with pension income and other retirement funds. These lenders may have more adaptable underwriting guidelines and offer personalized assistance, helping retirees secure the most favorable mortgage terms. Assessing long-term affordability involves more than just calculating monthly mortgage payments; it requires a comprehensive understanding of all income sources and expenses. Retirees should develop a comprehensive budget encompassing their pension income, Social Security benefits, annuity payments, and any additional income sources. On the expenditure side, it's crucial to account for current living expenses as well as potential rises in property taxes, homeowners insurance, and maintenance costs. Additionally, healthcare expenses, which tend to rise with age, should be carefully estimated and included in the budget. Ensuring that mortgage payments fit comfortably within this budget can prevent financial strain and allow retirees to maintain their desired lifestyle without compromising their financial security. It's essential for retirees to assess their complete financial picture, including any outstanding debts, the amount saved for emergencies, and anticipated future expenses. Existing debts like credit card balances, personal loans, or other mortgages can influence their capacity to take on new financial commitments. Before pursuing a new mortgage, it's often wise to prioritize paying down high-interest debt. Moreover, having enough savings to cover at least six months of living costs is recommended. This acts as a buffer against unforeseen events like medical emergencies or major home repairs. A strong financial base offers peace of mind and minimizes the risk of financial hardship in the face of unexpected expenses. Retirees should think about their current and future health needs and whether the property will suit them as they age. It's essential to consider accessibility features such as single-level living, wider doorways, bathroom grab bars, and ramps instead of stairs. Proximity to healthcare facilities, grocery stores, and other essential services can significantly impact quality of life. Similarly, retirees should consider the home's maintenance requirements. A property that is easier to maintain can help ensure that the home remains suitable even as physical capabilities change. Planning for potential future needs can make the difference between a home that becomes a burden and one that supports a comfortable lifestyle. Being aware of the tax effects associated with mortgage payments and homeownership can offer financial advantages and help prevent unexpected tax issues. For instance, the interest paid on your mortgage might be deductible, potentially lowering your taxable income and overall tax bill. Furthermore, assessing the tax implications of various mortgage options, including reverse mortgages, allows retirees to make well-informed choices that align with their financial objectives and tax planning. Seeking advice from a financial advisor or mortgage broker can be immensely helpful for retirees. These experts can assess your financial situation, guide you through different mortgage options, and help you make well-informed decisions. Financial advisors can aid in crafting a holistic financial plan that encompasses all aspects of retirement, from daily living expenses to long-term care considerations. Mortgage brokers, on the other hand, can connect you with a variety of mortgage products and negotiate terms on your behalf. Their professional insights are particularly valuable when navigating complex mortgage terms and long-term financial planning. Finally, seeking legal counsel may be advisable to fully comprehend the implications of reverse mortgages or equity release options. Navigating the complexities of securing a mortgage on a pension requires careful planning, understanding, and consideration of various factors. Retirees must ensure they meet eligibility criteria, maintain a good credit score, and provide proof of stable income to gain lender confidence. Exploring different mortgage options, including standard mortgages, reverse mortgages, and equity release options, allows retirees to choose the best fit for their financial needs and lifestyle goals. Engaging with traditional banks, credit unions, online lenders, and specialized lenders for retirees can provide access to competitive rates and personalized service. Long-term affordability, financial stability, health and mobility, and tax planning are crucial considerations when committing to a mortgage during retirement. Retirees should create a detailed budget, assess their overall financial health, and plan for future health needs and home accessibility. Understanding the tax implications of mortgage payments and seeking professional advice from financial advisors, mortgage brokers, and legal experts can further enhance decision-making and financial security. By taking a comprehensive approach and utilizing available resources, retirees can successfully secure a mortgage on a pension, ensuring a stable and comfortable lifestyle throughout their retirement years.Overview of Pensions and Mortgages

How to Get a Mortgage on a Pension

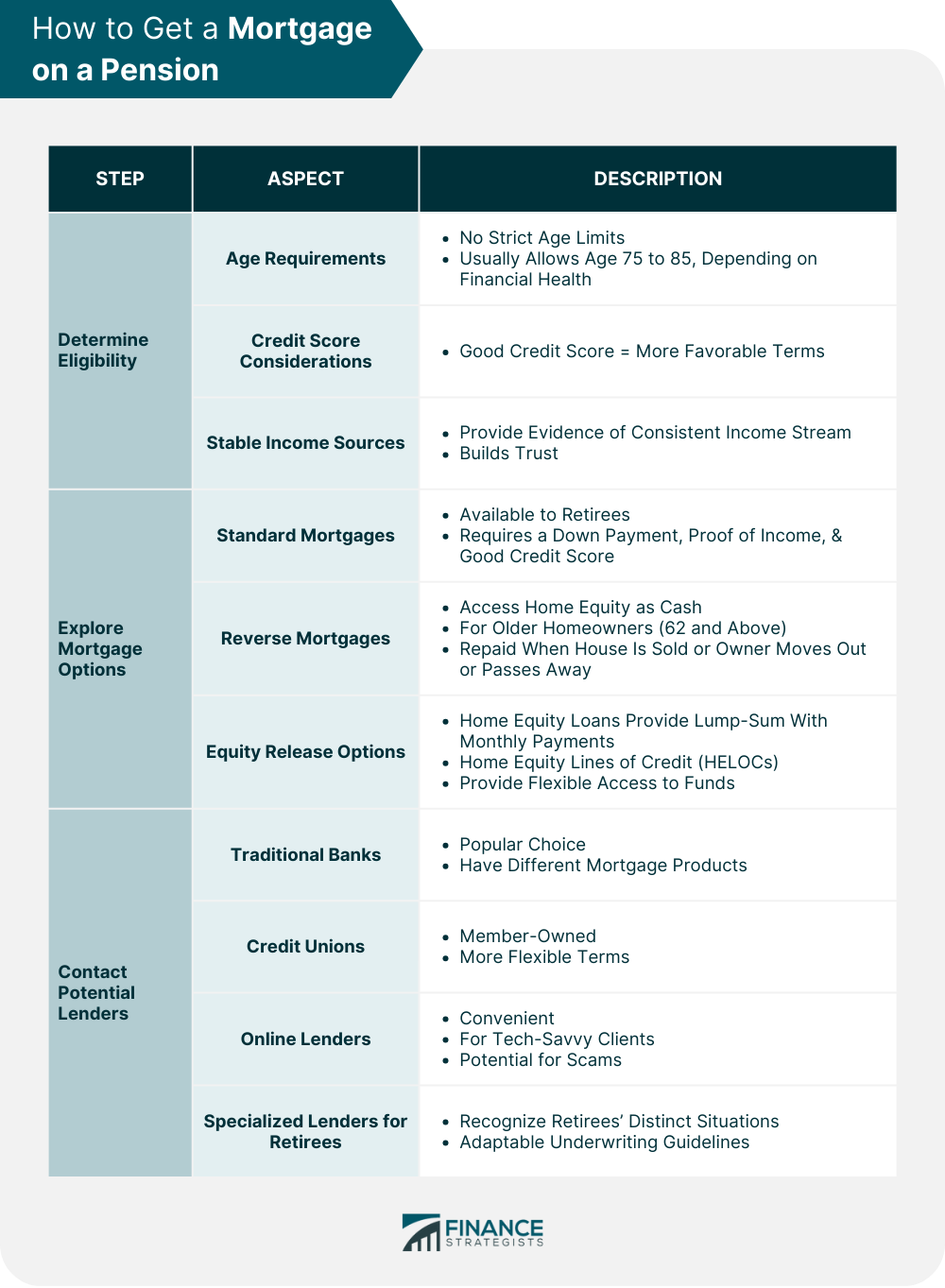

Determine Eligibility

Age Requirements

Credit Score Considerations

Stable Income Sources

Explore Mortgage Options

Standard Mortgages

Reverse Mortgages

Equity Release Options

Contact Potential Lenders

Traditional Banks

Credit Unions

Online Lenders

Specialized Lenders for Retirees

Factors to Consider When Getting a Mortgage on a Pension

Long-Term Affordability

Financial Stability

Health and Mobility

Tax Planning

Professional Advice

Conclusion

Getting Mortgage on a Pension FAQs

Yes, lenders often approve mortgages for retirees with stable pension income, provided they meet other eligibility criteria such as credit score and income consistency.

While there is no strict age limit, most lenders offer mortgages to individuals up to 75 years old, and some may extend this to 85 or older based on financial health and income stability.

Improve your credit score, gather proof of stable income, and reduce existing debts. Demonstrating consistent financial behavior and sufficient income streams increases lender confidence.

Retirees can choose from standard mortgages, reverse mortgages, and equity release options like home equity loans or lines of credit, depending on their financial needs and goals.

Yes, consulting financial advisors, mortgage brokers, and legal experts can provide valuable insights, helping you make informed decisions and ensuring long-term financial stability.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.