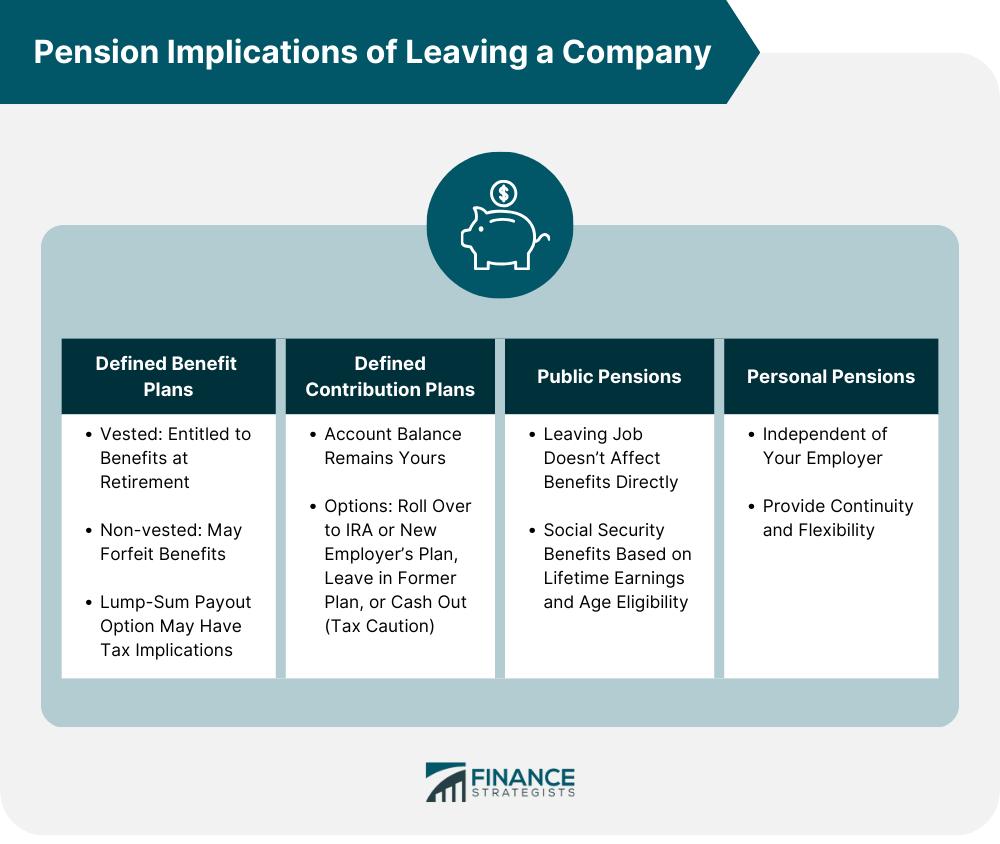

Pensions are retirement plans that aim to provide a consistent income stream during one's post-work years. They are a vital component of a well-rounded retirement strategy. Several types of pensions exist, notably defined benefit plans, which guarantee a set monthly payment determined by salary and years of service, and defined contribution plans, where the ultimate payout depends on contributions and investment outcomes. In addition, public pensions, like Social Security, and personal pensions, such as Individual Retirement Accounts (IRAs), provide supplementary retirement savings avenues. Pensions are financed through contributions from employers, employees, or a combination of both, and are subject to regulations designed to safeguard participants' interests. While they offer financial security in retirement and potential tax benefits, pensions face certain challenges, including longevity risk, investment risk, and potential regulatory shifts. The specifics of what happens to your pension are contingent on the type of pension plan you hold and its particular terms and conditions. Your pension benefits are influenced by your vested status and the plan's specific terms. If you are vested, meaning you have met the required service period (often around five years), you are entitled to receive benefits upon reaching the plan's retirement age, even if you no longer work for the company. These benefits are typically calculated based on your salary, years of service, and age. However, if you leave before becoming vested, you may forfeit your pension benefits, although you might receive a refund of any personal contributions you made. Defined benefit plans are usually not portable, meaning you cannot transfer the accrued value to another employer’s plan. Some plans offer a lump-sum payout option, allowing you to take a one-time payment instead of receiving monthly benefits in retirement. While this option can provide immediate funds, it often comes with tax implications and the challenge of managing the lump sum to ensure long-term financial security. The money in your account, including your contributions, employer contributions, and investment earnings, remains yours. One common option is to roll over your account balance into an Individual Retirement Account or another employer’s retirement plan. This preserves the tax-deferred status of your savings and allows for continued growth without immediate tax consequences. Rolling over to an IRA can provide more investment options and potentially lower fees, while rolling over to a new employer's plan can consolidate your retirement savings and simplify management. Alternatively, you may leave your money in your former employer’s plan, especially if your account balance exceeds a certain threshold, although you won’t be able to make additional contributions. Finally, you can opt to cash out your account balance, but this should be done cautiously, as it can result in significant tax liabilities and early withdrawal penalties if you are under retirement age. Public pensions in the United States, such as Social Security, provide retirement benefits based on cumulative contributions made through payroll taxes over your working life. When you leave a job, these benefits are not directly affected, as they are calculated based on your total lifetime earnings and contributions. Social Security benefits depend on your highest-earning 35 years of work, and you become eligible for benefits based on your age and the amount you've contributed. Changing jobs or retiring does not impact the benefits you've accrued, provided you continue to meet contribution requirements. The system is designed to offer a baseline income level in retirement, independent of any private pension plans you may have. Personal pensions, such as Individual Retirement Accounts, offer flexibility and control independent of your employer. When you leave a job, these accounts remain under your management, allowing you to continue making contributions and choosing your investments. Since personal pensions are not tied to your employment status, they provide continuity and flexibility, allowing you to maintain a consistent retirement savings strategy regardless of job changes. Vesting is the process that defines your right to employer-contributed pension funds. The vesting schedule can vary from immediate full vesting to a gradual, time-based system, impacting your eligible amount. Immediate vesting means you are entitled to 100% of your employer's contributions regardless of how long you've been with the company. This is more common in certain types of plans, like some 401(k) plans. This type of vesting is beneficial as it provides full pension benefits without the need for prolonged employment. It offers a clear and immediate addition to your retirement savings. In graded vesting, the percentage of vested benefits increases over a set period, often spanning several years. For example, an employee might be 20% vested after two years, 40% after three, and so on. Graded vesting encourages longer tenure with the employer. The gradual increase in vested benefits can significantly impact the total retirement benefit, especially for long-term employees. With cliff vesting, you become fully vested after a specific period, such as three or five years. If you leave before this period, you forfeit the employer-contributed portion of the pension. Cliff vesting is a high-stakes arrangement. Employees must be aware of their vesting schedule, as leaving just before reaching the cliff can result in significant financial loss. Begin by thoroughly understanding your pension plan benefits. Obtain and review the summary plan description to determine whether you are vested and what that means for your benefits. Contact the plan administrator to clarify any questions you have about your benefits, payout options, and decision-making deadlines. This step is essential for ensuring you make informed choices about your pension. Ensure your former employer and any retirement plan administrators have your current contact information to receive important communications about your benefits. Review and update beneficiary designations for your pension and retirement accounts to reflect any changes in your personal circumstances, such as marriage, divorce, or childbirth. Maintaining up-to-date information is vital for ensuring your benefits are correctly managed and distributed. Be aware of the tax implications of different pension and retirement plan options. Understanding these can help you make informed decisions and avoid unexpected tax burdens. If you decide to take a lump-sum payout, plan for withholding requirements and ensure you have a strategy to cover any potential tax liabilities. This knowledge is crucial for managing your finances effectively during the transition. Maintain organized records of all communications, statements, and documents related to your pension and retirement accounts. This includes plan descriptions, account balances, and any correspondence with plan administrators. Track important dates and deadlines for making decisions about your retirement accounts to avoid penalties and ensure you make the best choices for your situation. Keeping your financial records in order will help you stay informed and prepared for any future decisions. Seeking professional advice from a financial advisor can help you navigate the complexities of pension options, rollovers, and tax implications. A financial advisor can assist in developing a comprehensive retirement strategy that aligns with your long-term goals. Additionally, they can help you evaluate your overall retirement plan in light of your new employment status and make any necessary adjustments to ensure you stay on track toward your retirement goals. Understanding the implications of leaving a company on your pension is crucial for safeguarding your retirement. Defined benefit and defined contribution plans have distinct impacts on your benefits, depending on your vesting status and your choices upon leaving a company. Public pensions like Social Security provide a stable foundation unaffected by job changes, while personal pensions offer flexibility and continuity. Immediate steps such as reviewing your pension plan, updating personal information, understanding tax implications, organizing financial records, and consulting a financial advisor are essential for making informed decisions. Proactively managing your pension and retirement savings ensures that you maintain financial security and achieve your long-term retirement goals, regardless of your career transitions. Overview of Pensions

Pension Implications of Leaving a Company

Defined Benefit Plans

Defined Contribution Plans

Public Pensions

Personal Pensions

Vesting and Its Impact on Pensions

Immediate Vesting

Graded Vesting

Cliff Vesting

Immediate Steps to Take Upon Leaving a Company

Review Your Pension Plan

Update Your Personal Information

Understand Tax Implications

Organize Your Financial Records

Consult a Financial Advisor

Final Thoughts

What Happens to Your Pension When You Leave a Company? FAQs

If you leave a company before retirement, the fate of your pension depends on your vesting status. Fully vested employees retain their entire pension, while those partially vested or not vested may lose some or all employer contributions.

Vesting determines your entitlement to an employer's contributions to your pension. If you're fully vested, you keep the entire pension. Partially vested or non-vested individuals may forfeit a portion or all of the employer-contributed funds.

In a defined contribution plan, like a 401(k), you retain all the funds you have contributed, plus any vested employer contributions, regardless of when you leave the company.

You can roll over your pension into an IRA or a new employer's plan when you leave a company. This can provide more control over investments and potential tax benefits, but be aware of possible early withdrawal penalties and tax implications.

Opting for a lump-sum payout means receiving all your vested pension funds at once. While this offers immediate access to cash, it can also have significant tax implications and may affect your long-term retirement planning.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.