A rollover in retirement accounts refers to the process of moving funds from one retirement account to another. It is a way to consolidate retirement savings or transfer funds from an employer-sponsored plan, such as a 401(k), to an Individual Retirement Account (IRA) or another 401(k) plan. The purpose of a rollover is to maintain the tax-advantaged status of the funds and potentially give the account holder more control over their investments and lower fees. Rollover in retirement accounts is a crucial aspect of retirement planning, allowing individuals to transfer their retirement savings from one account to another.

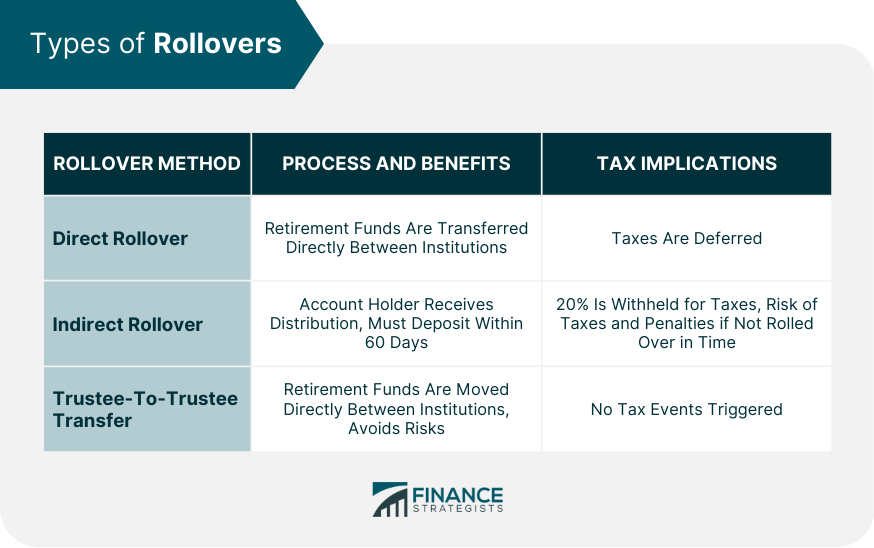

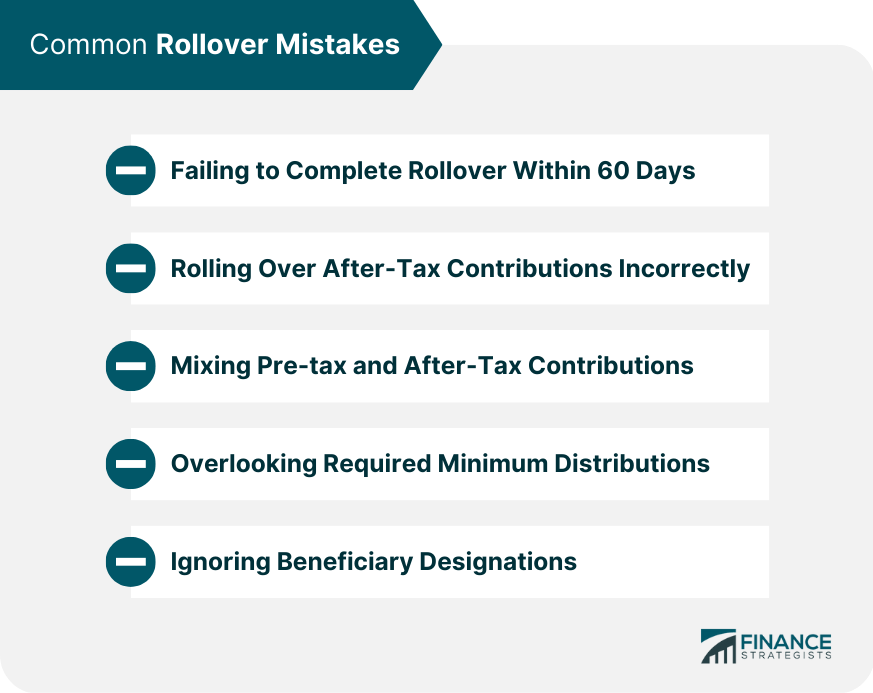

When individuals change jobs, they often have the option to roll over their old employer-sponsored retirement plan, such as a 401(k), to a new employer's plan or an individual retirement account (IRA). Rolling over multiple retirement accounts into one can simplify management, reduce paperwork, and provide a clearer view of one's overall retirement savings. A rollover may offer access to a wider range of investment options, including low-cost index funds or actively managed funds, that better align with an individual's investment strategy and risk tolerance. Transferring retirement savings to a lower-cost plan or provider can save on administrative fees and fund expense ratios, increasing the overall returns on investments. A direct rollover involves transferring retirement funds directly from one financial institution to another without the account holder ever taking possession of the funds. This option is typically faster, simpler, and eliminates the risk of early withdrawal penalties or taxes. In a direct rollover, taxes are deferred because the funds are transferred directly between institutions, maintaining the tax-advantaged status of the retirement account. An indirect rollover involves the account holder receiving a distribution of their retirement funds, which they must deposit into a new retirement account within 60 days. This method carries the risk of missing the 60-day deadline, resulting in taxes and early withdrawal penalties. With an indirect rollover, the distributing financial institution typically withholds 20% of the distributed amount for taxes. If the entire amount is not rolled over within 60 days, the withheld amount and any portion not rolled over are subject to taxes and potential penalties. A trustee-to-trustee transfer involves moving retirement funds directly between financial institutions, similar to a direct rollover, but is typically used for IRAs. This method avoids the risks associated with indirect rollovers and maintains the tax-advantaged status of the account. Trustee-to-trustee transfers do not trigger tax events, as the funds are transferred directly between institutions without any distribution to the account holder. Not all retirement accounts are eligible for rollovers. Common eligible accounts include 401(k), 403(b), and governmental 457(b) plans, as well as traditional and Roth IRAs. For indirect rollovers, account holders have 60 days to complete the rollover process. Failing to do so results in taxes and potential early withdrawal penalties. Individuals can only perform one indirect rollover per 12-month period for each IRA they own. This rule does not apply to direct rollovers or trustee-to-trustee transfers. In an indirect rollover, the distributing institution generally withholds 20% of the distributed amount for taxes. This amount must be replaced when completing the rollover to avoid taxes and penalties. Certain retirement plans, such as 401(k)s and some pension plans, may require spousal consent before initiating a rollover. It is essential to review the specific plan rules and consult with a financial professional if necessary. When considering a rollover, it is essential to evaluate the investment options available in the new plan or account. Factors to consider include the range of investment choices, the performance of available funds, and the alignment of investment options with one's financial goals and risk tolerance. Review the fees and expenses associated with the new retirement account, including administrative fees, fund expense ratios, and any transaction fees. Lower fees and expenses can significantly impact long-term investment growth. A rollover is an opportunity to reevaluate one's investment strategy and risk tolerance. Consider diversifying investments to strike a balance between risk and return, keeping in mind the time horizon until retirement. Understanding the tax implications of a rollover is critical. For example, rolling over pre-tax funds from a traditional 401(k) to a Roth IRA will trigger a taxable event. Consult with a tax professional to develop strategies to minimize taxes and maximize the benefits of the rollover. When executing a rollover, consider how the new account and investment options align with overall retirement goals and time horizon. The right choices should support the achievement of these goals and provide adequate growth and income in retirement. In an indirect rollover, missing the 60-day deadline can result in taxes and penalties. To avoid these consequences, consider using a direct rollover or trustee-to-trustee transfer. Rolling over after-tax contributions without properly tracking and reporting them can lead to double taxation. Ensure accurate record-keeping and consult with a tax professional to avoid tax-related issues. When consolidating retirement accounts, it is essential to avoid mixing pre-tax and after-tax contributions, as this can complicate tax reporting and potentially result in tax consequences. Account holders aged 72 or older must take required minimum distributions (RMDs) from their retirement accounts. Failing to do so can result in penalties. It is essential to consider RMDs when planning a rollover. Review and update beneficiary designations when executing a rollover to ensure that retirement assets are distributed according to one's wishes in the event of death. The process of rolling over retirement accounts is an essential component of effective retirement planning. It offers individuals the ability to adapt to changing circumstances, such as job changes, streamline their retirement savings, and fine-tune their investment approach. To make the most of a rollover, it is crucial to understand the various rollover types, adhere to applicable rules and limitations, and consider potential strategies while avoiding common pitfalls. Engaging with financial professionals can provide valuable guidance to ensure a successful rollover that aligns with one's long-term retirement objectives.What Is a Rollover in Retirement Accounts?

Reasons for Rollover

Changing Jobs

Consolidating Accounts

Access to Better Investment Options

Lower Fees and Expenses

Types of Rollovers

Direct Rollover

Process and Benefits

Tax Implications

Indirect Rollover

Process and Risks

Tax Implications

Trustee-To-Trustee Transfer

Process and Benefits

Tax Implications

Rollover Rules and Limitations

Eligible Retirement Plans

Rollover Period

One-Per-Year Rule

Mandatory Withholding

Spousal Consent

Rollover Strategies and Considerations

Evaluating Investment Options

Assessing Fees and Expenses

Balancing Risk and Return

Tax Implications and Strategies

Retirement Goals and Time Horizon

Common Rollover Mistakes

Failing to Complete Rollover Within 60 Days

Rolling Over After-Tax Contributions Incorrectly

Mixing Pre-tax and After-Tax Contributions

Overlooking Required Minimum Distributions

Ignoring Beneficiary Designations

Conclusion

Rollover in Retirement Accounts FAQs

A Rollover is the process of moving funds from one retirement account to another. It is a way to consolidate retirement savings or transfer funds from an employer-sponsored plan, such as a 401(k), to an Individual Retirement Account (IRA) or another 401(k) plan.

Yes, you can roll over your 401(k) to an IRA. This is a common choice for those who change jobs or retire. Rolling over your 401(k) to an IRA can give you more control over your investments and potentially lower fees.

Yes, there is a time limit for completing a rollover. In most cases, you have 60 days from the date you receive the funds to complete the rollover. If you miss this deadline, the funds will be considered a distribution, subject to taxes and penalties.

Yes, you can roll over a Roth IRA to a traditional IRA, but you will owe taxes on the conversion. This is because Roth IRA contributions are made with after-tax dollars, while traditional IRA contributions are made with pre-tax dollars.

Yes, there are restrictions on how many rollovers you can do in a year. For example, you can only do one rollover per year from the same IRA account. Additionally, some employer-sponsored plans may limit the number of rollovers you can do in a year. It is important to check the rules of your specific plan or account to ensure compliance.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.