Social Security Disability Insurance (SSDI) is a vital program that supports people with disabilities who can't work full-time. While the program provides monthly payments, its impact goes beyond finances. It can empower people with disabilities to achieve goals like homeownership. Homeownership is a milestone that holds both financial and personal significance. It provides a stable and secure living environment and a sense of independence and stability. For SSDI recipients, owning a home can become a tangible dream, and SSDI plays a pivotal role in helping them realize this aspiration. One fundamental way SSDI contributes to home ownership is by providing a reliable income source. A stable income is a fundamental requirement for purchasing and maintaining a home. The consistent cash benefits from SSDI can help cover mortgage payments and other housing-related expenses, making homeownership a feasible goal for those with disabilities. When on SSDI, your income is a critical factor in home-buying eligibility. Lenders typically scrutinize your income stability and capacity to manage mortgage payments. While SSDI provides a steady income, it is often lower than standard employment wages, which can limit borrowing capacity. Additionally, maintaining a strong credit score is vital. It signifies financial responsibility to lenders and can lead to better mortgage terms and rates. Programs like the HUD Homeownership Voucher Program or Federal Housing Administration (FHA) loans are particularly accessible to SSDI recipients. These programs often have more lenient requirements regarding income and credit scores, acknowledging the unique financial situations of individuals with disabilities. Specialized mortgage programs are tailored for individuals with disabilities, including those on SSDI. These programs often feature more lenient qualification criteria and favorable terms. Fannie Mae's HomeReady program and certain non-profit organization offerings fall into this category, providing unique opportunities for SSDI recipients. Conventional loans are a common choice for many homebuyers, including those on SSDI. These loans are not backed by the government and typically require a higher credit score and down payment than government-backed loans. However, they offer diverse terms and interest rates. SSDI recipients should compare offers from multiple lenders to find the most favorable terms that match their financial situation. SSDI recipients can enjoy an advantage when buying a home because of FHA loans. These loans require smaller down payments (as low as 3.5%) and are more flexible with credit scores. The Federal Housing Administration insures the loans, making them less risky for lenders and ultimately easier for people with lower incomes or limited credit histories to qualify for. For veterans receiving SSDI, VA loans offer an excellent opportunity with no down payment requirements and no minimum credit score, alongside competitive interest rates. Many states and localities offer homeownership assistance programs that can provide grants or low-interest loans for down payments and closing costs. Such programs often target low-income individuals or those with disabilities, making them a perfect fit for SSDI recipients. Organizations like the Department of Housing and Urban Development (HUD) and non-profits offer grants for individuals with disabilities. Budgeting is essential for realistically assessing what you can afford for mortgage payments, property taxes, insurance, and maintenance costs. A cautious approach to budgeting ensures long-term financial sustainability in your homeownership journey. The choice of location and property type has profound implications on affordability and suitability. Accessibility, proximity to healthcare facilities, and community support services should be high on your priority list. Additionally, the property type, whether a single-family home, townhouse, or condo, impacts maintenance responsibilities and costs. Long-term financial planning includes considering the potential changes in SSDI benefits, planning for home maintenance and unexpected expenses, and ensuring that your investment aligns with your long-term financial goals and health needs. Start by ensuring you have at least a couple of credit accounts, such as a credit card or a small loan. Use these accounts responsibly by making purchases and paying off the balance regularly. Your debt-to-income ratio (DTI) is a significant factor in mortgage applications. Aim to keep this ratio low, ideally below 36%. A lower DTI ratio indicates to lenders that you have a good balance between your debts and your SSDI income, enhancing your creditworthiness. Many local and state governments offer down payment assistance programs, especially for low-income or disabled individuals. Research programs in your area, as they can vary widely in terms of benefits and eligibility requirements. These programs can provide grants or low-interest loans to cover part or all of your down payment, making homeownership more accessible. Numerous non-profit organizations offer assistance specifically designed for individuals with disabilities, including grants for down payments, home modifications, or educational resources to help you navigate the home-buying process. Seek out housing counselors who specialize in working with individuals on SSDI or with disabilities. These professionals are familiar with your situation's unique challenges and opportunities, including understanding how SSDI income and benefits work in the context of home buying. Many non-profit organizations and government programs offer free or low-cost housing counseling services. These counselors can provide personalized advice on budgeting, choosing the right mortgage product, and navigating the home-buying process. Buying a home while on SSDI is certainly challenging, but it is not impossible. With the right approach, resources, and guidance, achieving homeownership is a realistic goal. The journey requires careful consideration of your financial status, eligibility for various programs, and a thorough understanding of the financing options available. Your eligibility for buying a home on SSDI hinges on your income stability, credit score, and ability to navigate government assistance and specialized mortgage programs. Financing options are diverse, ranging from traditional mortgages to specialized grants and assistance programs, each with its own criteria and benefits. Careful consideration of your financial situation, potential properties, and long-term plans is crucial. Factors like budgeting, location, property type, and long-term financial implications must be at the forefront of your decision-making process.SSDI and Home Ownership

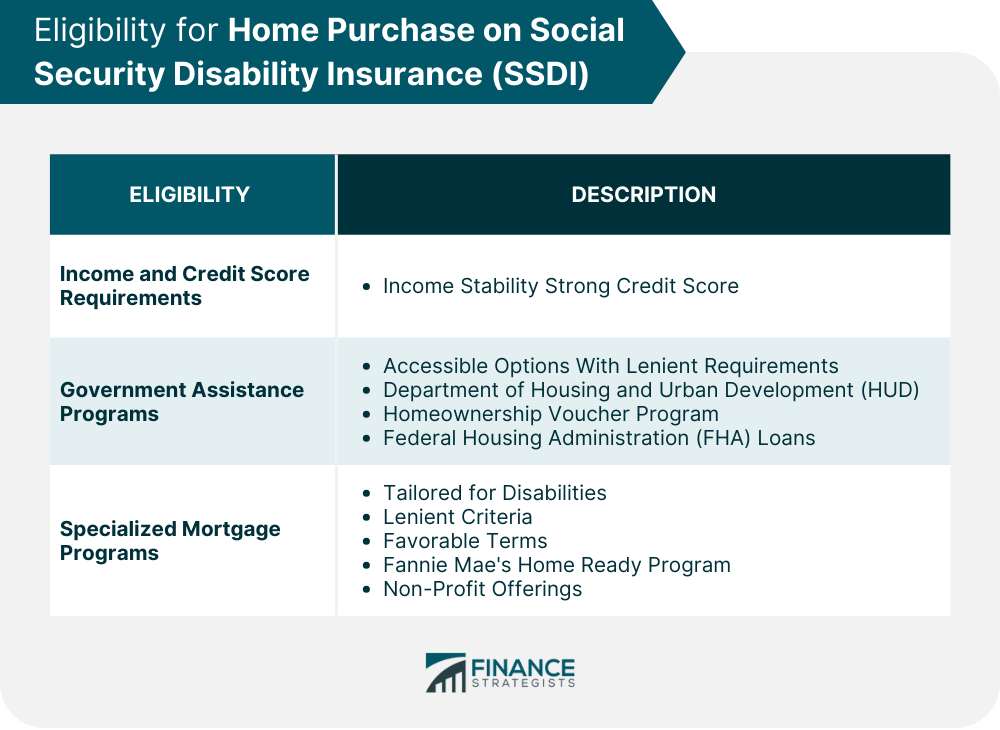

Eligibility for Home Purchase on SSDI

Income and Credit Score Requirements

Government Assistance Programs

Specialized Mortgage Programs

Financing Options for SSDI Recipients

Traditional Mortgage Loans

FHA Loans and Other Government Programs

Grants and Housing Assistance

Factors to Consider When Buying a Home on SSDI

Budgeting and Affordability

Location and Property Type

Long-Term Financial Planning

Tips for a Successful Home Purchase on SSDI

Build a Strong Credit Profile

Explore Down Payment Assistance

Work With Housing Counselors

Conclusion

Can You Buy a Home if You Are on SSDI? FAQs

SSDI income is considered stable and reliable, which can work in your favor during the mortgage approval process. However, the amount of SSDI income may limit the loan size you are eligible for.

Yes, there are mortgage programs and assistance designed for people with disabilities, including those on SSDI. These include government-backed loans and specialized programs from non-profit organizations.

Absolutely. Many SSDI recipients benefit from combining their mortgages with government assistance programs for down payments, renovations, or subsidized housing options.

While the required credit score can vary by lender and loan type, having a score of 620 or higher generally opens up more options. FHA loans are known for their more lenient credit requirements.

Begin by assessing your financial health, including your credit score and budget. Then, explore different mortgage options and assistance programs. Working with a housing counselor can also provide valuable guidance.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.