Pension and Social Security benefits are two primary sources of retirement income for many individuals. Pension plans are employer-sponsored retirement plans that provide a predetermined monthly benefit or a lump-sum distribution upon retirement. Social Security is a government-sponsored program that offers monthly benefits to eligible retirees based on their earnings history and age at retirement. Coordinating pension and Social Security benefits is crucial for maximizing retirement income and ensuring financial security. Proper coordination can help individuals develop a comprehensive retirement income plan that meets their needs and goals. Defined benefit pension plans guarantee a specific monthly benefit based on factors such as salary, years of service, and age at retirement. Defined contribution plans, such as 401(k)s and 403(b)s, allow employees and employers to contribute to an individual account, with the retirement benefit depending on the account's value at retirement. Individuals become eligible for Social Security benefits after earning a minimum number of credits through work and paying Social Security taxes. The full retirement age for Social Security benefits ranges from 65 to 67, depending on the year of birth. Social Security benefits are calculated based on an individual's highest 35 years of earnings, adjusted for inflation. The benefit amount increases for each year that claiming is delayed, up to age 70. Various claiming strategies, such as early, full, or delayed retirement, can impact the amount of Social Security benefits received over a lifetime. Claiming pension and Social Security benefits early can result in reduced monthly benefits. However, for individuals with pressing financial needs or shorter life expectancies, early retirement may be the best option. Claiming benefits at full retirement age ensures that individuals receive their full pension and Social Security benefits. This strategy can provide a stable retirement income but may not maximize lifetime benefits. Delaying pension and Social Security benefits can result in higher monthly payments, maximizing lifetime benefits for individuals with longer life expectancies. Considering life expectancy is crucial when coordinating pension and Social Security benefits, as it affects the total amount of benefits received over a lifetime. Coordinating benefits with a spouse can help maximize joint lifetime benefits and ensure financial security for both partners. Understanding survivor benefits for both pension and Social Security can help provide financial protection for a surviving spouse. Accounting for COLAs in both pension and Social Security benefits can help maintain purchasing power during retirement. Delaying the claiming of Social Security benefits can result in higher monthly payments due to delayed retirement credits. Delaying Social Security benefits can also maximize spousal and survivor benefits, ensuring financial security for both partners. A lump-sum pension distribution can be used to cover living expenses while delaying Social Security benefits, allowing for higher monthly payments later in retirement. Pension annuity payments can also be used to bridge the gap between early retirement and full retirement age, enabling individuals to delay claiming Social Security benefits and receive higher monthly payments later in retirement. Coordinating pension and Social Security benefits with other income sources can help manage taxable income and reduce tax liability during retirement. Strategically converting traditional retirement accounts to Roth accounts can help minimize taxes on Social Security benefits and pension distributions. Evaluating income needs and goals in retirement is essential for coordinating pension and Social Security benefits effectively. Diversifying income sources by investing in various retirement accounts, such as IRAs and 401(k)s, can provide additional financial security and flexibility. Investment income, such as dividends and capital gains, can supplement pension and Social Security benefits, providing additional financial stability during retirement. Engaging in part-time work during retirement can help supplement pension and Social Security benefits, allowing for greater financial flexibility and the potential to delay claiming benefits. Individual circumstances, such as health status, family situation, and financial goals, should be considered when coordinating pension and Social Security benefits. Working with a financial professional can provide valuable guidance and assistance in coordinating pension and Social Security benefits, as well as developing a comprehensive retirement income plan. Selecting a financial advisor with expertise in retirement planning and knowledge of pension and Social Security benefits can help ensure that individuals receive personalized advice tailored to their unique needs and goals. Coordinating pension and Social Security benefits is essential for maximizing retirement income and ensuring financial security. By understanding the various factors that influence these benefits and employing strategic planning, individuals can develop a comprehensive retirement income plan that meets their needs and goals. Proper coordination of pension and Social Security benefits can have a significant impact on financial security and overall retirement planning. By considering personal circumstances, diversifying income sources, and working with a financial professional, individuals can optimize their retirement income and achieve greater financial stability during their golden years.Coordinating Pension and Social Security Benefits: Overview

Understanding Pension and Social Security Benefits

Types of Pension Plans

Defined Benefit Plans

Defined Contribution Plans

Social Security Benefits

Eligibility

Benefit Calculation

Claiming Strategies

Coordinating Pension Benefits With Social Security

Timing of Pension and Social Security Benefits

Early Retirement

Full Retirement Age

Delayed Retirement

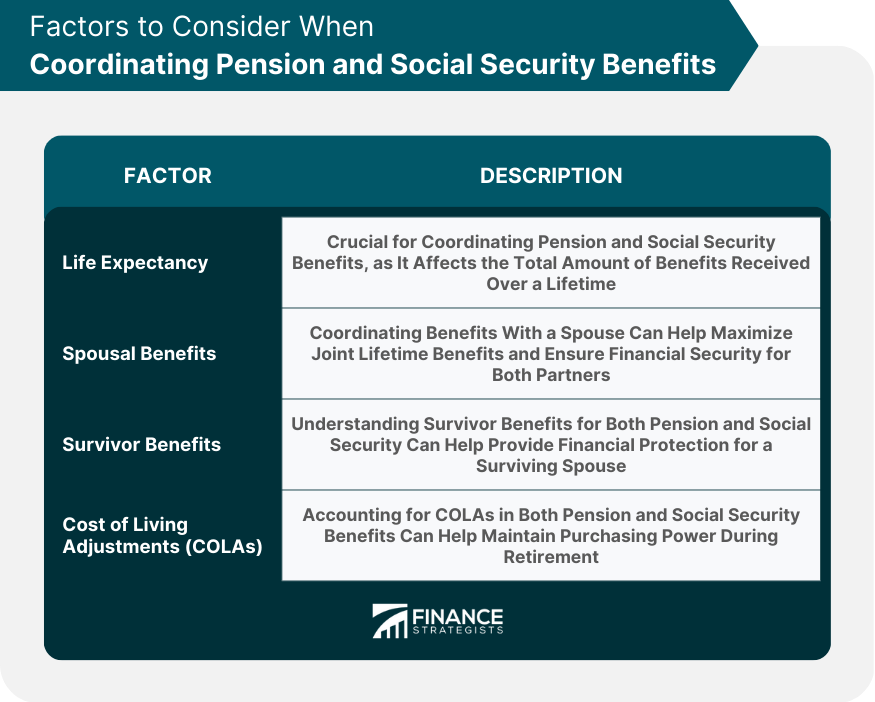

Factors to Consider

Life Expectancy

Spousal Benefits

Survivor Benefits

Cost of Living Adjustments (COLAs)

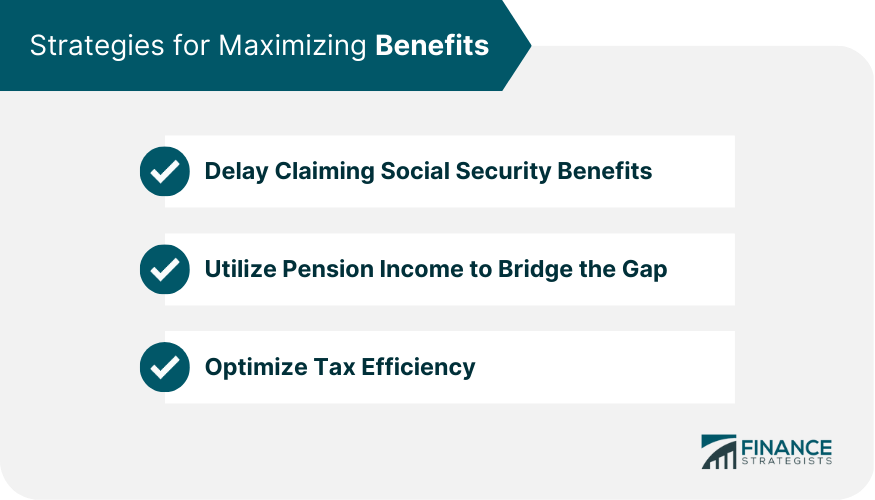

Strategies for Maximizing Benefits

Delay Claiming Social Security Benefits

Increase Monthly Benefit Amount

Maximize Spousal and Survivor Benefits

Utilize Pension Income to Bridge the Gap

Lump-Sum Distribution

Annuity Payments

Optimize Tax Efficiency

Managing Taxable Income

Roth Conversions

Creating a Comprehensive Retirement Income Plan

Assessing Income Needs and Goals

Diversifying Income Sources

Retirement Accounts

Investments

Part-Time Work

Adjusting Strategies Based on Personal Circumstances

Working With a Financial Professional

Benefits of Professional Guidance

Choosing the Right Financial Advisor

Conclusion

Coordinating Pension and Social Security Benefits FAQs

Coordinating pension and Social Security benefits involves structuring your retirement income to maximize your benefits from both sources while minimizing taxes.

Coordinating pension and Social Security benefits is important because it can help you maximize your retirement income and make the most of the benefits available to you.

The best way to coordinate your benefits depends on your individual situation, including your age, income, retirement goals, and tax situation. Consulting with a financial advisor can help you determine the best strategy for your specific needs.

Yes, it is possible to receive both a pension and Social Security benefits at the same time. However, your Social Security benefits may be reduced if you receive a pension from an employer who did not pay into Social Security.

Yes, it is possible to change your pension and Social Security benefit coordination strategy after you retire. However, changes may have tax implications, and it is important to work with a financial advisor to understand the potential impacts of any changes you make.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.