Full Retirement Age (FRA), also known as "normal retirement age," is when an individual becomes eligible to receive full, unreduced Social Security retirement benefits. FRA is determined by the Social Security Administration (SSA) and is based on an individual's birth year. FRA is an important concept in retirement planning because it affects the amount of Social Security benefits an individual can receive.

The concept of the Full Retirement Age originated with the Social Security Act of 1935, which established the United States social insurance program. The act set the FRA at 65 years for most workers, as it was considered a reasonable age to retire and receive full benefits. Over time, the FRA has been adjusted in response to changes in life expectancy and the financial stability of the Social Security system. The 1983 Social Security Amendments gradually increased the FRA to 67 years for individuals born in 1960 or later. FRA varies across different countries, with most developed countries having an FRA between 65 and 67 years. Some countries have implemented gradual increases in their FRA, similar to the United States, to address demographic changes and the sustainability of their pension systems. Your birth year is the primary determinant of your FRA. The Social Security Administration provides a chart that lists the FRA based on birth year, making it simple to find your FRA. The FRA chart provides a clear breakdown of the FRA based on birth year, which ranges from 65 to 67 years. Below is a table summarizing the different FRAs based on birth year. As life expectancy increases, future policy changes may further adjust the FRA. These adjustments aim to maintain the financial sustainability of the Social Security system and reflect the changing retirement landscape. Maximum Social Security benefits refer to the full, unreduced monthly benefit amount an individual can receive based on their earnings record. Reaching one's Full Retirement Age is a key milestone in achieving these maximum benefits. In contrast, individuals who choose to claim Social Security benefits before reaching their FRA will experience a permanent reduction in their monthly benefit amount. The Social Security Administration imposes an earnings limit on individuals who claim Social Security benefits before reaching their Full Retirement Age. This earnings limit, also known as the retirement earnings test, restricts the amount of income an individual can earn from work without affecting their Social Security benefits. However, once an individual reaches their FRA, the earnings limit no longer applies. This means that individuals who have attained their FRA can continue to work and earn income without any impact on their Social Security benefits. They can receive their full Social Security benefit amount regardless of how much they earn from employment or self-employment. This flexibility allows individuals to supplement their retirement income and maintain financial security while continuing to work, if they choose to do so. The absence of an earnings limit at FRA gives retirees greater freedom to balance work and retirement according to their individual needs and preferences. Delayed Retirement Credits (DRCs) are a financial incentive offered by the Social Security Administration to encourage individuals to postpone claiming Social Security retirement benefits beyond their Full Retirement Age. DRCs are earned each month that an individual delays claiming benefits after reaching their FRA up until 70. The accumulation of DRCs permanently increases the individual's monthly Social Security benefit amount, leading to higher retirement income. The percentage increase in benefits due to DRCs varies depending on the individual's birth year. The longer the delay, the greater the increase, up to the maximum at age 70. By understanding the impact of DRCs, individuals can make informed decisions about when to claim benefits and optimize their retirement income. You can choose to retire early and start receiving Social Security benefits as early as age 62. However, this comes with certain consequences. If you retire early, your Social Security benefits will be permanently reduced. The reduction depends on how many months before your FRA you start receiving benefits. When considering early retirement, weighing the reduced benefits against factors such as your health, life expectancy, financial needs, and personal preferences is essential. Carefully evaluating these factors will help you make an informed decision about early retirement. You can increase your monthly Social Security benefits by delaying retirement beyond your FRA. This is due to the accumulation of Delayed Retirement Credits. For every year you delay retirement beyond your FRA, your Social Security benefits increase by a certain percentage up to age 70. This can result in a significantly higher monthly benefit. When considering delayed retirement, evaluating your financial needs, life expectancy, health, and personal preferences is important. Delaying retirement may not be suitable for everyone, so making a decision that aligns with your circumstances is essential. Understanding your FRA can help you better calculate your retirement needs. This includes estimating your expected Social Security benefits and considering other sources of retirement income and expenses. Your FRA should be a factor in your overall savings and investment strategies. This can help ensure you have enough financial resources to support your desired retirement lifestyle. Health care and long-term care costs can be significant expenses during retirement. Your FRA may impact your ability to cover these costs, so it is crucial to plan for them in your retirement planning. Understanding the Full Retirement Age (FRA) is crucial for effective retirement planning and optimizing Social Security benefits. FRA is the age at which individuals become eligible to receive full, unreduced Social Security retirement benefits. Considering FRA in retirement calculations, savings and investment strategies, and planning for healthcare costs are essential for a well-rounded retirement plan. By understanding the benefits and implications of FRA, individuals can make informed decisions to secure a comfortable and financially stable retirement.What Is Full Retirement Age (FRA)?

Claiming Social Security benefits before reaching FRA results in a permanent reduction in the monthly benefit amount, while delaying benefits beyond FRA can result in an increase in the monthly benefit amount due to Delayed Retirement Credits.Historical Background of Full Retirement Age

Social Security Act of 1935

Evolution of FRA in the United States

International Comparison of FRA

Determining Your Full Retirement Age

Birth Year as a Determinant

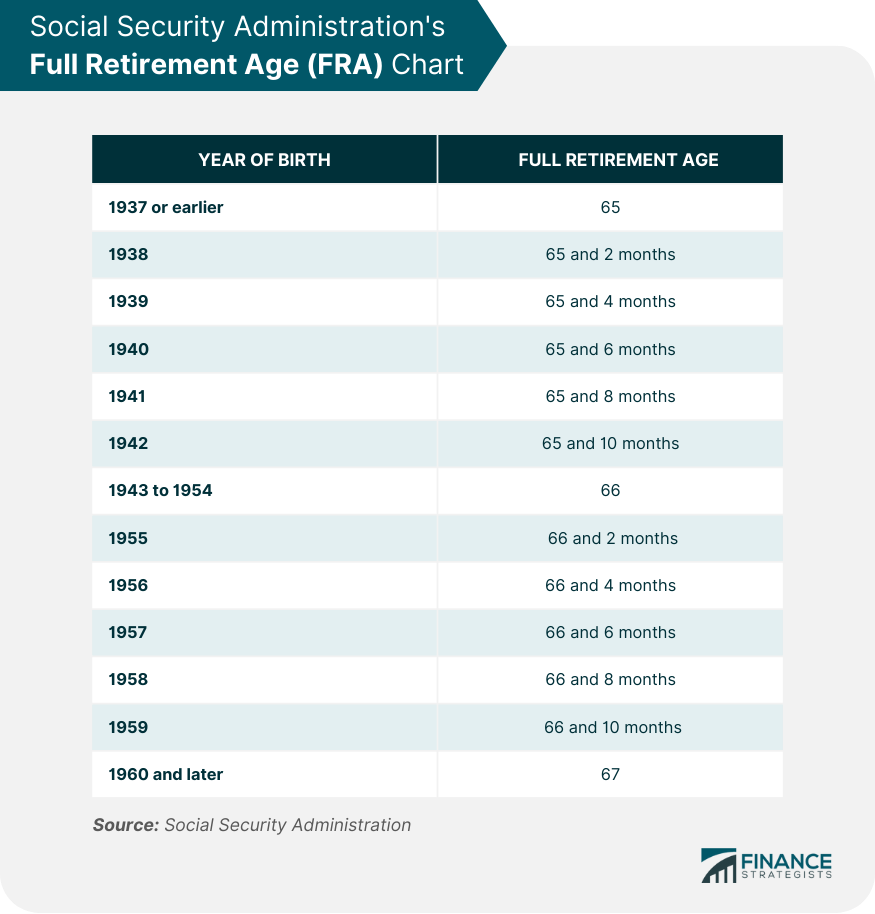

Social Security Administration's FRA Chart

Impact of Changes in Life Expectancy on FRA

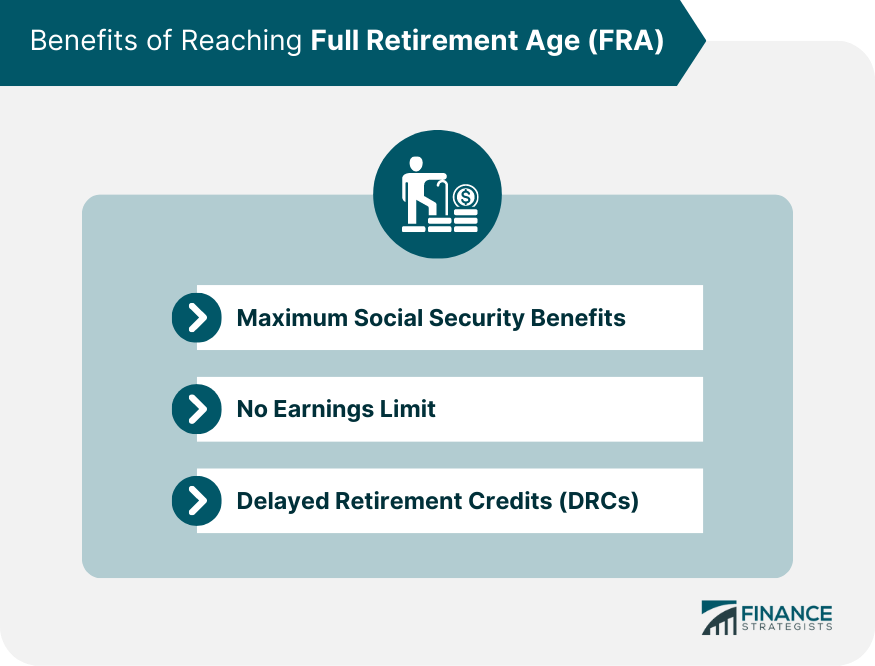

Benefits of Reaching Full Retirement Age

Maximum Social Security Benefits

By waiting until FRA to claim Social Security benefits, individuals can ensure they receive their full benefit amount, known as the Primary Insurance Amount (PIA), without any permanent reductions.

The PIA is calculated using a formula that accounts for an individual's highest 35 years of earnings and represents the highest monthly benefit they are entitled to at FRA.

This reduction is based on the number of months they claim benefits before their FRA, and it can significantly impact their retirement income.

Therefore, understanding one's FRA and the implications of claiming benefits early or at FRA is essential for making informed decisions about retirement planning and maximizing Social Security benefits.No Earnings Limit

If an individual's earnings exceed the annual limit, their Social Security benefits may be temporarily reduced. The earnings limit is adjusted annually and varies depending on whether the individual is below FRA, in the year they reach FRA, or has already reached FRA.Delayed Retirement Credits (DRCs)

This financial incentive can be especially beneficial for individuals who are in good health, have a longer life expectancy, and wish to maximize their lifetime Social Security benefits.

Early Retirement vs Full Retirement Age

Early Retirement Eligibility

Reduction in Social Security Benefits

Factors to Consider for Early Retirement

Delaying Retirement Beyond Full Retirement Age

Increased Monthly Benefits

Earning Delayed Retirement Credits

Factors to Consider for Delayed Retirement

Planning for Retirement With Full Retirement Age in Mind

Calculating Your Retirement Needs

Savings and Investment Strategies

Factoring in Health Care and Long-Term Care Costs

Conclusion

Reaching FRA has several benefits, including the ability to receive maximum Social Security benefits without any permanent reductions.

Additionally, individuals who reach FRA can continue to work and earn income without any earnings limit impacting their Social Security benefits, providing flexibility in retirement decisions.

Delaying retirement beyond FRA can result in increased monthly benefits due to Delayed Retirement Credits, which can significantly enhance retirement income. However, claiming benefits before FRA leads to a permanent reduction in the monthly benefit amount. |

It is important to carefully evaluate the factors associated with early retirement or delaying retirement, such as health, life expectancy, financial needs, and personal preferences.

Full Retirement Age (FRA) FAQs

Full Retirement Age (FRA) is when an individual becomes eligible to receive full, unreduced Social Security retirement benefits. FRA is important because it affects the amount of Social Security benefits a person receives, with reduced benefits for claiming early and increased benefits for delaying beyond FRA.

Your Full Retirement Age (FRA) is determined by the Social Security Administration (SSA) based on your birth year. For individuals born in 1937 or earlier, the FRA is 65. For those born between 1938 and 1959, the FRA gradually increases from 65 to 67. For individuals born in 1960 or later, the FRA is 67.

Yes, you can claim Social Security retirement benefits as early as age 62, regardless of your Full Retirement Age (FRA). However, claiming benefits before FRA results in a permanent reduction in your monthly benefit amount. The earlier you claim, the greater the reduction.

If you delay claiming Social Security benefits beyond your Full Retirement Age (FRA), you can earn Delayed Retirement Credits, which increase your monthly benefit amount. These credits accrue until age 70, after which there is no additional increase for delaying benefits.

You can find out your specific Full Retirement Age (FRA) by using the retirement age calculator provided by the Social Security Administration (SSA) on its website. The calculator allows you to input your birth year and determine your FRA based on SSA guidelines.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.