Family Limited Partnerships (FLPs) are legal entities that allow family members to pool their assets and manage an investment or business together. FLPs provide benefits such as asset protection, tax savings, and efficient succession planning. They consist of general partners with management responsibilities and unlimited liability and limited partners with limited liability who do not participate in day-to-day management. FLPs can be a powerful tool for preserving family wealth and maintaining family involvement in a business across generations.

There are legal requirements and other details involved in establishing a Family Limited Partnership. To establish an FLP, several steps must be taken: 1. Selecting a Jurisdiction: Choose the state or country where the FLP will be registered, considering the legal and tax implications. 2. Drafting the Partnership Agreement: This document outlines the rights and responsibilities of the partners, as well as the terms and conditions governing the partnership. An FLP consists of at least one general partner, who takes on management responsibilities and has unlimited personal liability, and one or more limited partners who have limited liability but do not participate in day-to-day management. Partners contribute capital to the FLP in exchange for partnership interests, which represent their ownership and share of the profits and losses. There are several advantages to Family Limited Partnerships. FLPs offer several benefits in terms of asset protection: Liability Protection for Limited Partners: Limited partners are not personally liable for partnership debts or obligations beyond their investment. Shielding Assets From Creditors: FLP assets are separate from personal assets, making it difficult for creditors to seize them. FLPs provide various tax advantages: Income Tax Advantages: Income is passed through to partners, avoiding double taxation. Estate and Gift Tax Planning: FLPs allow for tax-efficient transfer of assets to future generations. FLPs are a useful tool for succession planning: Transfer of Assets and Control: FLPs can facilitate the gradual transfer of ownership and control to younger generations. Continuity of Family Business: FLPs provide a structure for maintaining family involvement in the business. FLPs encourage effective business management: The Role of General Partners: General partners can focus on management without interference from limited partners. Involving Family Members in the Business: FLPs provide a platform for mentoring and training younger family members. Family Limited Partnerships also come with disadvantages. General partners face unlimited personal liability for partnership debts and obligations, which can be a significant risk. Establishing an FLP involves legal, accounting, administrative expenses, and ongoing compliance requirements. FLPs can be subject to IRS scrutiny, and improper use can lead to audits or legal challenges. FLPs can exacerbate family disputes, especially if the partnership agreement does not clearly address potential conflicts. Below are some points to consider so that one can establish a successful FLP. A well-drafted partnership agreement is essential for setting expectations and avoiding disputes among partners. Accurate and up-to-date records are necessary for tax, legal, and management purposes. Regularly reviewing and updating the FLP can help ensure it continues serving the family's needs and goals. Legal, tax, and financial professionals can help guide the establishment and management of an FLP. There are several excellent real-life examples and case studies of FLPs. Several examples demonstrate the successful use of FLPs in various industries, including real estate, manufacturing, and agriculture. These case studies highlight the benefits of FLPs in terms of asset protection, tax savings, and efficient transfer of family wealth. FLP failures can offer valuable insights into potential pitfalls and challenges. Common issues include inadequate partnership agreements, lack of communication among family members, and failure to adapt to changing circumstances. Family Limited Partnerships (FLPs) play a crucial role in helping family businesses achieve their objectives and preserve their wealth for future generations. As the landscape of FLPs continues to evolve, staying informed and adapting to the changing legal, tax, and economic environment is crucial. Ensuring clear communication and education among family members is also vital for the long-term success of an FLP. To navigate the complexities of establishing and managing an FLP, we recommend consulting with a tax services expert who can provide personalized guidance and support. What Are Family Limited Partnerships (FLPs)?

Establishing a Family Limited Partnership

Legal Requirements and Formation Process

3. Registering With Government Authorities: File the necessary paperwork and fees with the appropriate state or federal agencies.Choosing the General and Limited Partners

Capital Contributions and Partnership Interests

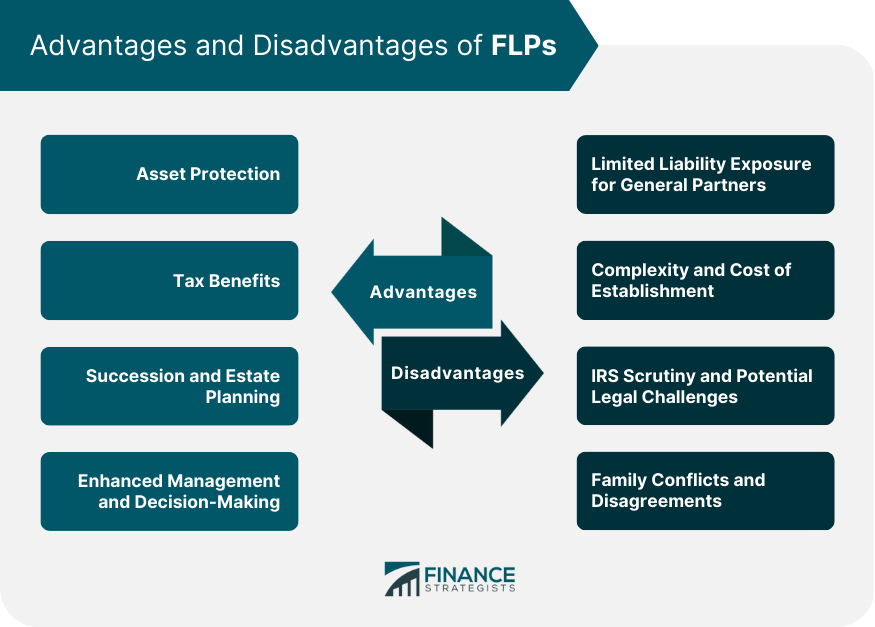

Advantages of Family Limited Partnerships

Asset Protection

Tax Benefits

Succession and Estate Planning

Enhanced Management and Decision-Making

Disadvantages and Risks of Family Limited Partnerships

Limited Liability Exposure for General Partners

Complexity and Cost of Establishment

IRS Scrutiny and Potential Legal Challenges

Family Conflicts and Disagreements

Key Considerations for a Successful FLP

Drafting a Comprehensive Partnership Agreement

Maintaining Proper Records and Documentation

Periodic Review and Updating of the FLP Structure

Seeking Professional Advice and Support

Case Studies and Real-Life Examples of FLPs

Successful FLPs in Various Industries

Lessons Learned From FLP Failures

Conclusion

By offering asset protection, tax savings, and efficient succession planning, FLPs provide a valuable tool for managing family assets and businesses.

However, it is essential to carefully weigh the pros and cons before establishing an FLP and to ensure it is structured effectively to serve your family's needs.

This may involve updating partnership agreements, reevaluating succession plans, and embracing new technologies and business models.

Do not miss out on the potential benefits of an FLP—contact a tax services professional today to help secure your family's financial future.

Family Limited Partnerships (FLPs) FAQs

A Family Limited Partnership (FLP) is a legal structure that allows family members to pool their assets and manage a business or investment together, offering benefits such as asset protection, tax savings, and efficient succession planning.

The main advantages of an FLP include asset protection for limited partners, income tax advantages, estate and gift tax planning opportunities, streamlined succession and estate planning, and enhanced management and decision-making for general partners.

Potential disadvantages and risks of FLPs include limited liability exposure for general partners, complexity and cost of establishment, IRS scrutiny and potential legal challenges, and the possibility of family conflicts and disagreements.

Key considerations for a successful FLP include drafting a comprehensive partnership agreement, maintaining proper records and documentation, periodically reviewing and updating the FLP structure, and seeking professional advice and support from legal, tax, and financial professionals.

FLPs can adapt to the needs of future generations by updating partnership agreements and succession plans, incorporating environmental, social, and governance (ESG) considerations into investment strategies, embracing new business models and technologies, and fostering education and communication among family members.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.