Limited Liability Companies (LLCs) are a popular business structure that combines the advantages of both corporations and partnerships. They offer limited liability protection to their owners (called members) and allow for flexibility in management and taxation. LLCs are particularly attractive for small businesses and entrepreneurs due to their simplicity and legal benefits. The main purpose of an LLC is to provide its members with limited liability protection, which means that they are not personally responsible for the company's debts and liabilities. Additionally, LLCs offer tax benefits, such as pass-through taxation and flexibility in management and ownership structures. This gives business owners more control over how their company operates and is taxed. LLCs are distinct from other business structures, such as sole proprietorships, partnerships, and corporations. Sole proprietorships and partnerships offer fewer liability protections and have different tax implications, while corporations provide limited liability but may be subject to more complex regulations and double taxation. LLCs strike a balance between these structures by offering limited liability protection, flexible management, and favorable tax treatment. When forming an LLC, selecting an appropriate name for the company is crucial. The name must include the phrase "Limited Liability Company" or an abbreviation such as "LLC" or "L.L.C." Additionally, the name must not be misleading or deceptively similar to other registered business names in the state where the LLC is formed. A name search must be conducted with the relevant state agency, usually the Secretary of State, to ensure that the desired LLC name is available. If the name is available, it may be reserved for a specific period, typically 30 to 90 days, for a nominal fee. Articles of Organization must be filed with the state to form an LLC officially. These documents generally include the LLC's name, purpose, duration, registered agent, and principal office address. The requirements for the content and format of Articles of Organization may vary by state. The filing process usually involves submitting the Articles of Organization to the state agency responsible for business filings and the required filing fee. Some states allow for online filing, while others may require paper submission. An Operating Agreement is a crucial document that outlines the LLC's internal governance and operating procedures. Although not always required by law, having a comprehensive Operating Agreement in place can help prevent disputes among members and provide guidance on various business matters. The Operating Agreement typically includes information on ownership interests, management structure, voting rights, profit, and loss distribution, and procedures for resolving disputes and dissolving the LLC. The Operating Agreement serves as the primary legal document governing the LLC's internal affairs. It can help establish the legitimacy of the company in the eyes of courts, creditors, and other parties, and can also provide additional protection for members' limited liability. Depending on the nature of the business, an LLC may require certain federal permits or licenses to operate. For example, businesses that deal with food, drugs, or firearms may need specific federal licenses. LLCs must also comply with state and local licensing and permit requirements, which vary depending on the type of business and the location. These may include professional licenses, health and safety permits, and zoning permits. LLCs can be either member-managed or manager-managed. In a member-managed LLC, all members actively participate in the daily management and decision-making of the business. This structure is common for small businesses with a limited number of members. In a manager-managed LLC, the members appoint one or more managers to oversee the daily operations, while the members take a more passive role. This structure is more common for larger LLCs or those with passive investors. When choosing between a member-managed and manager-managed structure, it is essential to consider the needs and preferences of the members. Factors to consider include the members' expertise, time commitments, and desired level of involvement in the business. The Operating Agreement should outline the LLC's voting rights and decision-making processes. Voting rights may be allocated based on the percentage of ownership interest or other agreed-upon terms. Some decisions may require a majority vote, while others, such as amending the Operating Agreement or dissolving the LLC, may require a supermajority or unanimous consent. LLCs should hold regular meetings to discuss and decide on important business matters. The Operating Agreement should specify the frequency and procedures for meetings and the requirements for maintaining accurate records of meeting minutes and other important company documents. Members and managers of an LLC owe a duty of care to the company, which requires them to act in the best interests of the LLC and exercise reasonable care and diligence in their decision-making. The duty of loyalty requires members and managers to act in good faith, avoid conflicts of interest, and not engage in self-dealing or activities that could harm the LLC or its members. Members can contribute capital to the LLC in various forms, such as cash, property, or services. The Operating Agreement should specify the value of each member's contribution and how it affects their ownership interest. Ownership interest in an LLC is typically allocated based on the value of each member's capital contribution. However, members can agree on a different allocation method, which should be documented in the Operating Agreement. Profits and losses can be distributed to LLC members in different ways, such as in proportion to their ownership interest or based on a predetermined formula. The chosen method should be outlined in the Operating Agreement. LLCs are generally subject to pass-through taxation, which means that the profits and losses are passed through to the members and reported on their individual tax returns. This structure helps avoid double taxation, a common issue for corporations. By default, LLCs are treated as pass-through entities for tax purposes. This means that the company itself does not pay income taxes; instead, the profits and losses are allocated among the members, who report them on their personal tax returns. In some cases, an LLC may choose to be taxed as a corporation by filing IRS Form 8832 (Entity Classification Election). This option may be advantageous for businesses that want to retain earnings within the company or provide fringe benefits to employees. Limited liability protection shields members from personal responsibility for the debts and liabilities of the LLC. This means that members' personal assets, such as their homes and bank accounts, are generally protected from claims by creditors or lawsuits against the LLC. There are some exceptions to limited liability protection, such as when members engage in fraudulent activities, personally guarantee company debts, or fail to maintain the LLC's legal and financial separation from their personal affairs. Members may be held personally liable for the company's debts or liabilities in these cases. Members should separate their personal and business assets to maintain limited liability protection. This can be accomplished by maintaining separate bank accounts and credit cards, using the LLC's name on all contracts and legal documents, and keeping accurate records of all business transactions. A well-drafted Operating Agreement can also provide additional protection for members' assets. For example, the agreement can include provisions that restrict the transfer of membership interests, limit the ability of creditors to seize a member's interest in the LLC or establish procedures for handling the bankruptcy of a member. Members may choose to voluntarily dissolve the LLC for various reasons, such as retirement, disagreements among members, or a desire to pursue other business ventures. In these cases, the members should follow the procedures outlined in the Operating Agreement for voluntary dissolution. Involuntary dissolution may occur due to bankruptcy, a court order, or the LLC's predetermined duration expiration. In these cases, state laws typically dictate the procedures for winding up the company. Members must settle the company's outstanding debts and liabilities when dissolving an LLC. This process generally involves notifying creditors, collecting outstanding accounts receivable, and liquidating assets to pay off debts. After all debts and liabilities have been settled, any remaining assets are distributed to the members according to the provisions of the Operating Agreement or, if not specified, in proportion to their ownership interests. To formally dissolve the LLC, members must file Articles of Dissolution with the state agency responsible for business filings, typically the Secretary of State. The Articles of Dissolution generally include information such as the name of the LLC, the effective date of dissolution, and a statement that all debts and liabilities have been resolved. One of the main advantages of an LLC is the limited liability protection it offers its members. This protection shields members' personal assets from the company's debts and liabilities, providing peace of mind and financial security. LLCs offer flexibility in management and taxation, allowing members to choose between member-managed or manager-managed structures and opt for pass-through or corporate taxation. This flexibility enables business owners to tailor their company's structure to suit their needs and preferences best. LLCs are subject to state-specific regulations, which can vary significantly from state to state. This can create confusion and additional administrative burdens, particularly for businesses operating in multiple states. In some states, an LLC may have a limited lifespan or may be dissolved upon the death or withdrawal of a member. Additionally, the transferability of ownership interests in an LLC can be more restricted compared to corporations, making it less attractive for investors or potential buyers. Limited Liability Companies have emerged as a popular choice for businesses due to their unique combination of limited liability protection, flexibility in management and taxation, and simplicity in formation and operation. However, business owners must consider the advantages and disadvantages of forming an LLC and the specific state regulations governing these entities. When forming an LLC, choosing an appropriate name, filing the Articles of Organization, drafting a comprehensive Operating Agreement, and obtaining the necessary permits and licenses are essential. Members should also carefully decide on the management structure, capital contributions, and profit and loss distribution methods that best suit their needs. LLCs offer significant benefits, such as limited liability protection and flexibility in management and taxation, making them an attractive option for many business owners. However, they also come with certain drawbacks, such as state-specific regulations and limited transferability of ownership. By carefully considering these factors and seeking professional guidance from tax services experts, entrepreneurs can determine if an LLC is the right choice for their business ventures.What Are Limited Liability Companies (LLCs)?

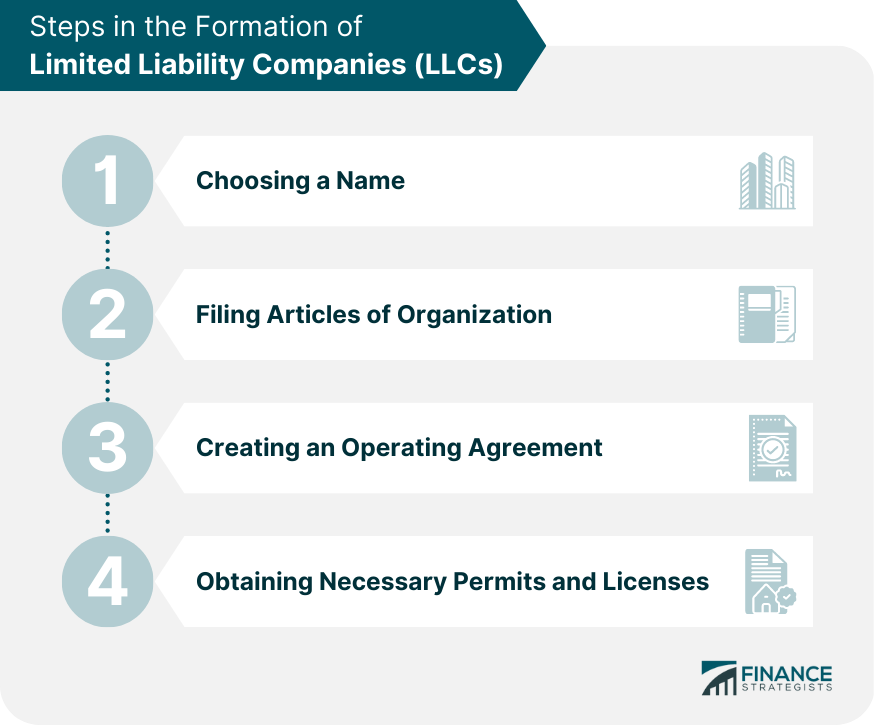

Formation of an LLC

Choosing a Name

Filing Articles of Organization

Creating an Operating Agreement

Obtaining Necessary Permits and Licenses

Management and Governance of LLCs

Member-Managed vs Manager-Managed LLCs

Decision-Making Process

Fiduciary Duties of Members and Managers

Financial Aspects of LLCs

Capital Contributions

Profit and Loss Distribution

Taxation of LLCs

Liability Protection in LLCs

Limited Liability for Members

Asset Protection Strategies

Dissolution and Winding Up of LLCs

Reasons for Dissolution

Winding Up Process

Filing Articles of Dissolution

Advantages and Disadvantages of LLCs

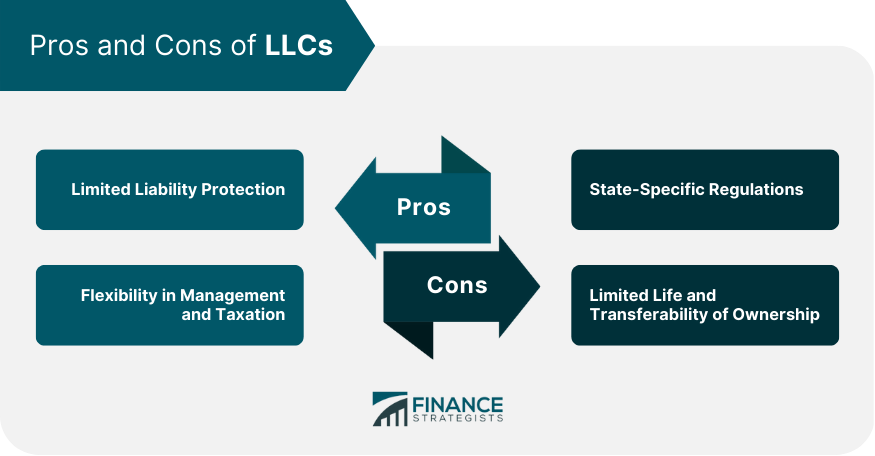

Advantages

Limited Liability Protection

Flexibility in Management and Taxation

Disadvantages

State-Specific Regulations

Limited Life and Transferability of Ownership

Conclusion

Limited Liability Companies (LLCs) FAQs

The key advantages of forming an LLC include limited liability protection for its members, flexibility in management and taxation, and a simpler formation process compared to corporations. These benefits make LLCs an attractive option for small businesses and entrepreneurs.

The management structure of an LLC is specified in the company's Operating Agreement. Members can choose between a member-managed or manager-managed structure, depending on their desired level of involvement in the daily operations and decision-making of the business.

To specify the name of a new LLC, first, ensure that the name meets the legal requirements, such as including "Limited Liability Company" or an abbreviation like "LLC." Next, conduct a name search with the relevant state agency to confirm the name's availability. Finally, reserve the desired name, if necessary, before filing the Articles of Organization.

The distribution of profits and losses in an LLC is specified in the Operating Agreement. Members can choose to allocate profits and losses based on their ownership interest, a predetermined formula, or any other method agreed upon by the members.

To specify the dissolution of an LLC, members must follow the procedures outlined in the Operating Agreement or state law, which typically include settling the company's debts and liabilities, distributing any remaining assets, and filing Articles of Dissolution with the appropriate state agency.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.