When starting a business, one of the most important decisions that entrepreneurs need to make is choosing the right business entity and tax status. Limited Liability Company (LLC) and S Corporation (S Corp) are two popular options. Both provide liability protection for business owners and are treated differently for tax purposes. Choosing the right tax status for a business can have significant financial implications, making it important for business owners to understand the differences between LLCs and S Corps. LLC is a business structure that blends features of sole proprietorship, partnership, and corporation. It provides protection against personal liability for business owners, shielding their personal assets from business-related obligations. An S Corp is a type of corporation that has elected a special tax status with the IRS. S Corps also provides personal liability protection for their owners and offer pass-through taxation. LLCs that elect to be taxed as S Corps will have a different tax treatment compared to LLCs that have default pass-through taxation. The owner of an LLC taxed as a partnership is not an employee of the LLC for tax purposes. They are simply business owners. In contrast, an S corporation owner who performs more than minor services for the corporation will be its employee for tax purposes and an owner. An active owner in an S corporation wears at least two hats: as a shareholder or owner of the entity and as an employee of that entity. By default, the income of the LLC passes through to the personal tax returns of the owner, and the owners pay self-employment taxes on the income at a rate of 15.3%. By electing to be taxed as an S Corporation, the income of the LLC can be split between salary and distributions, which can result in significant tax savings for the owners. Consider the scenario where you are the only proprietor of an LLC with a $200,000 annual profit. Let us say that $50,000 is a fair wage in your location for someone doing the same job as you. You must pay self-employment taxes on the entire $200,000 profit under the default LLC taxation. But, if your company is taxed as an S-corp, you will only be responsible for paying payroll taxes on your fair wage of $50,000. The remaining $150,000 will not be liable to Medicare or Social Security taxes but will still be subject to income tax. Owners of S Corps have historically benefited from this tax break by categorizing their income as 100% distributions and 0% compensation, wholly evading payroll taxes. LLCs do not have a required tax classification and are taxed using the tax system that applies to other entity types. The IRS applies the pass-through taxation system to LLCs by default, which means that the LLC's income passes through to the owners, and the owners pay taxes on their individual tax returns. The default tax classification of a single-member LLC is a disregarded entity, while a multi-member LLC is taxed as a partnership. In both cases, the LLC does not pay taxes separately from its owners, and the pass-through system avoids the double taxation that applies to C corporations. It is worth noting that an LLC with more than one owner can be treated as a single-member LLC for tax purposes, even though it is treated as a multi-member LLC for all other purposes. LLC owners can choose the tax classification that is most advantageous to them. If an LLC owner wants to change the default tax classification, they can elect to have the LLC taxed as an S corporation by filing Form 2553, Election by a Small Business Corporation, with the IRS. The LLC must meet certain requirements to qualify for S Corp status, including: Having no more than 100 shareholders Only one class of stock No nonresident alien or corporate shareholders These requirements are usually easy for most small businesses to meet, but business owners must ensure that their LLC qualifies before filing Form 2553. The LLC must make the election within two months and 15 days of the beginning of the LLC's taxable year when the election is to go into effect. Unlike electing to be taxed as a C corporation, there is no need to file Form 8832, Entity Classification Election, first. Filing Form 2553 collapses the steps so that the LLC is treated as both changing its status to a corporation and making a subchapter S election for the corporation. LLC owners choose to be taxed as an S corporation to save self-employment taxes. It is important to note that LLCs are usually formed to avoid being taxed as a C corporation, and the only real choice is between accepting the default classification or electing to be taxed as an S corporation. When deciding on the right tax status for your business, there are several factors to consider, including: When considering the right tax status for a business, business owners should factor in their long-term goals. If the business goal is to grow and potentially go public or take on outside investors, a corporation may be a better fit due to its more formal structure and ability to issue different classes of stock. On the other hand, if the goal is to maintain a smaller business with a more flexible structure, remaining on the default LLC may be a better choice. One of the most important factors to consider when choosing a tax status is the tax implications. Business owners should weigh the advantages and disadvantages of each tax status and determine which one will be the most tax-efficient for their business. For example, if a business owner wants to minimize their self-employment taxes, an S Corp may be a better choice. However, if a business owner wants to retain more profits in the business, an LLC with default pass-through taxation may be a better option. The number of owners and how they want to structure management can also impact the decision between LLC default and S Corp tax status. S Corps have restrictions on the number of owners and the types of ownership, while LLCs allow for more flexibility. For example, an S Corp can only have up to 100 shareholders and all shareholders must be individuals or certain types of trusts. LLCs, on the other hand, can have an unlimited number of owners and can have different classes of ownership, such as voting and non-voting units. Both LLCs and S Corps offer personal liability protection to their owners. However, LLCs may be a better choice for businesses with higher liability risks, such as those in the construction or medical industries. This is because LLCs offer more flexibility in terms of management structure and have fewer formal requirements than corporations. It is important to note that personal liability protection is not absolute, and business owners should still take steps to mitigate risks, such as obtaining adequate insurance coverage. Choosing the right tax status for your business can be a complicated decision, and consulting with a financial advisor or tax professional can help. These professionals can help you weigh the pros and cons of each tax status and determine which one will be the most advantageous for your business. A financial advisor or tax professional can also help you with the legal and financial requirements of forming and maintaining an LLC or S Corp. They can help you file the necessary paperwork and ensure that you are in compliance with state and federal regulations. Choosing the right tax status for your business can have significant financial implications, and it is important to understand the differences between the default LLCs and S Corps. Both offer advantages and disadvantages, and business owners should consider factors such as their long-term goals, tax implications, ownership and management, and liability protection when making a decision. LLCs offer personal liability protection, pass-through taxation, and simplicity of operation, while S Corps offers the potential for reduced self-employment taxes and avoiding double taxation. However, S Corps have limitations on the number of owners and classes of shareholders and may be subject to additional administrative costs and record-keeping requirements. Business owners should carefully weigh the advantages and disadvantages and consult with a financial advisor or tax professional before making a decision. These professionals can help with the legal and financial requirements of forming and maintaining an LLC or S Corp, and ensure compliance with state and federal regulations.Understanding LLC and S Corp

How LLCs Taxed as S Corps Work

Business Owner Employment Status

Tax Comparison

Default LLC Tax Classification Rules

Changing Default LLC Tax Classification to S Corporation

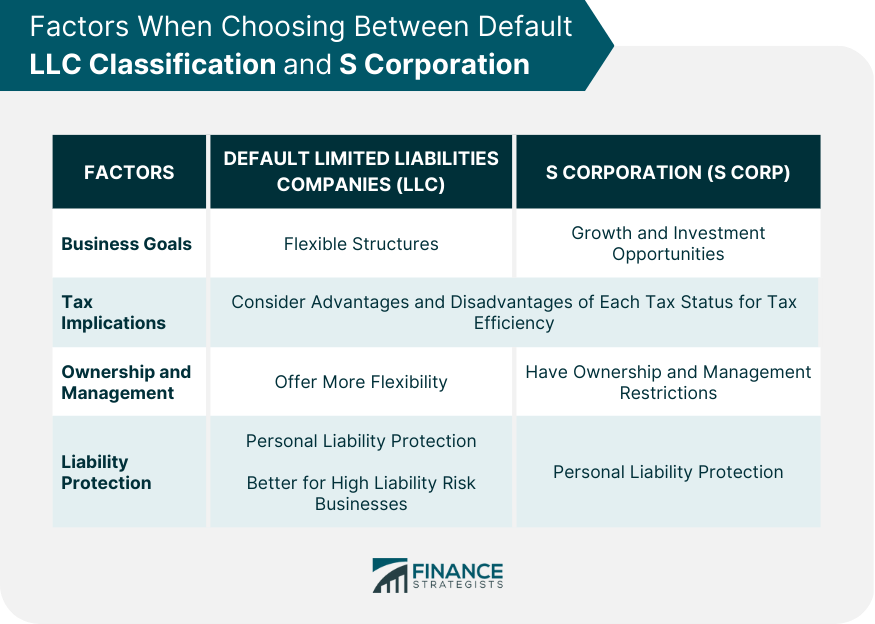

Factors When Choosing Between Default LLC Classification and S Corporation

Business Goals

Tax Implications

Ownership and Management

Liability Protection

The Bottom Line

LLC Taxed as S Corp FAQs

An LLC, or limited liability company, is a type of business structure that offers personal liability protection to its owners while maintaining a flexible management structure.

An S Corporation is a type of corporation that has elected a special tax status with the IRS. S Corps provide personal liability protection to their owners and offer pass-through taxation, which can result in significant tax savings.

An LLC can elect to be taxed as an S Corp by filing Form 2553, Election by a Small Business Corporation, with the IRS. The LLC must meet certain requirements to qualify for S Corp status, including having no more than 100 shareholders and only one class of stock.

LLCs that elect to be taxed as S Corporations can benefit from reduced self-employment taxes while still enjoying the flexibility and ease of operation that come with the LLC structure. S Corps can also avoid double taxation, and owners can take a salary as an employee of the corporation and receive the remaining profits as distributions, which can result in significant tax savings.

Business owners should consider their long-term goals, tax implications, ownership and management structure, and liability protection when choosing S Corp tax status. Consulting with a financial advisor or tax professional can also help make an informed decision.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.