The S Corp and C Corp identifiers relate to tax categories available to corporations. S Corp and C Corp are named after sections of the Internal Revenue Code that regulate their taxation procedures. Under IRS standards, a company is categorized as a C Corporation by default. Companies under S Corporation have adopted special tax status, allowing them some tax advantages. The decision between C Corp and S Corp classification for a company can significantly impact its future, growth, and investor base. Here are some characteristics that both S Corporations and C Corporations share: S Corporations and C Corporations can provide limited liability protection to their shareholders, so they are usually not personally liable for the business entity's debts and obligations. Laws stipulate no distinction between S Corporations and C Corporations regarding compliance requirements. Both corporations must follow internal and external corporate protocols. S Corp and C Corp observe applying bylaws, distributing stocks, organizing shareholder and director meetings, establishing registered agents and offices, reporting annually, and settling annual fees. S and C Corporations have shareholders, directors, members, and officers. Shareholders own the corporation, but the corporation takes ownership of the business. The shareholders select the board of directors. The board of directors monitors and controls corporate affairs and decision-making but is not in charge of day-to-day operations. The board chooses the officers to oversee the daily operations of the company. Listed below are the elements that differentiate S Corp and C Corp from each other: Taxation difference usually nudges companies to choose an S Corp or a C Corp category. C Corps are taxed twice. The company must pay both corporate income tax and federal income taxes through their dividends. On the other hand, S Corps have pass-through taxation where they report income gains and losses with a personal tax return. There are no corporate tax obligations. An S Corp can only have 100 U.S. citizens as shareholders, while a C Corp caps no limit on the number of shareholders. This difference could be an important factor for businesses that plan to grow quickly or raise money from investors. When establishing a company, by default, it is classified as a C Corporation. No additional procedures are necessary to become a C Corp. If a company wants to be established as an S Corp, Form 2553 must be filed, and other documents must be accomplished to remain an S Corp. Let us look at some merits of choosing to be an S Corporation. A significant advantage of S Corp is that no corporate taxes are required. Income distribution to shareholders is taxed at an individual level. The losses incurred by an S Corp pass through to their shareholders. This means that shareholders can use business losses to offset other income. This way, they can reduce the overall tax burden. S Corporations have some disadvantages that should be considered as well. S Corporations are limited to only 100 shareholders and must strictly be U.S. citizens. This does not allow them to go public and limits the capacity to increase their capital from investors. Private equity funds and venture capitals are ineligible shareholders. S Corps cannot provide different classes of stock, and shareholders have the same rights and privileges. This discourages investors who have preferences. Shareholders tend to find it difficult to leave S Corporations because selling or transferring shares are often restricted. This policy ensures that S Corps do not end up with unqualified shareholders that might lead to the termination of the S Corp status. S Corp requires more steps during formation. Additional paperwork like Form 2553 is necessary, and each state might have different requirements that must be observed. Taxes of S Corporations are rigorously investigated, and an error might lead to the cancellation of the S Corp status. Dividends are strictly compared with salary payment balances. Below is a summary of some of the advantages and disadvantages of an S Corp. There are several reasons to choose a C Corporation. A C Corporation can have an indefinite number of shareholders. Businesses, non-U.S. citizens, basically anyone can own shares. This could be helpful if a company needs to raise money by selling shares. C Corps can also issue more than one class of stock, including stock with preferences to dividends and distributions, common and preferred shares. Corporate tax rates were lowered to the 21% flat rate after the 2017 Tax Reform Act was implemented. This is lower than the 37% maximum personal tax rate. C Corps can easily obtain equity financing because the code does not impose any ownership restriction. Selling stock to potential investors to raise capital is convenient. In terms of formation, upon filing the article of organization, the default status of a company is automatically a C Corp, so less paperwork is necessary. C Corps are allowed to claim benefits and donations as deductions. Charitable contributions and donations can be deducted from corporate tax returns as long as the donations are less than 25% of the company's income. The biggest drawback of C Corps is double taxation. Company revenues are taxed, and individuals are also taxed for personal returns. Owners lose money twice on their earnings. Writing-off corporate losses on personal income taxes are prohibited in C Corps. Owners cannot offset other income. The table below lists a summary of the advantages and disadvantages of a C Corp. S Corps are a friendly option, especially for small businesses, because of the savings they can get from avoiding double taxation. S Corps are also ideal for startups because losses can pass through to owners and be written off on individual tax returns. Additionally, S Corp makes sense for owners who draw a salary since self-employment taxes can be minimized in this type. On the other hand, businesses seeking to raise capital through angel investors or venture capitalists may choose a C Corp because it has no ownership restrictions. This allows the company to expand considerably enough for them to go public. In addition, C Corp is reasonable when a business reinvests its profits instead of allocating them as dividends, as this avoids double taxation. There are other various company models or classifications. Here are some more choices that owners might consider: B Corporations or Benefit Corporations, also known as Public Benefit Corporations (PBCs), are for-profit companies that are trying to balance public benefit and obligations to their shareholders. It is important to note that this is a state label and not a federal tax designation. Nonprofit corporations are formed for reasons other than shareholder profit. These people are eligible for important tax breaks at state and federal levels, including exemption from federal income tax. LLCs fall between the corporate and partnership models. LLCs can be taxed similarly to C-corps and S-corps. Owners, referred to as members, benefit from limited liability protection while not being subject to the same rules and administrative obligations as a corporation. While LLCs are simpler for small business owners to organize and operate, they are not as receptive to easy outside investment. Sole proprietorships are the most basic company form, providing a single owner with little regulatory obligations and a high degree of control and freedom. These are exclusively taxed at the individual level and do not permit the selling of stock, the presence of shareholders or business partners, or any responsibility limits. Regarding taxes and responsibility, partnerships are identical to sole proprietorships but entail an agreement between two or more owners. Depending on the industry and other qualifying circumstances, a limited partnership (LP) or limited liability partnership (LLP) may also be considered. The choice between C Corp and S Corp classification may substantially impact a company's capacity to attract investors and save money on taxes. However, there is no one-size-fits-all solution. The advantages and disadvantages of each must be weighed to pick the best for every specific firm, Decisions concerning incorporation or business registration should be based on the specific circumstances of each firm, and owners should speak with legal and tax specialists throughout the business formation process. Regardless, it is critical to have a basic awareness of the alternatives available and to keep in mind that many organizations transition from one structure to the next as they develop.S Corp vs C Corp: An Overview

S Corp vs C Corp: Similarities

S Corp vs C Corp: Differences

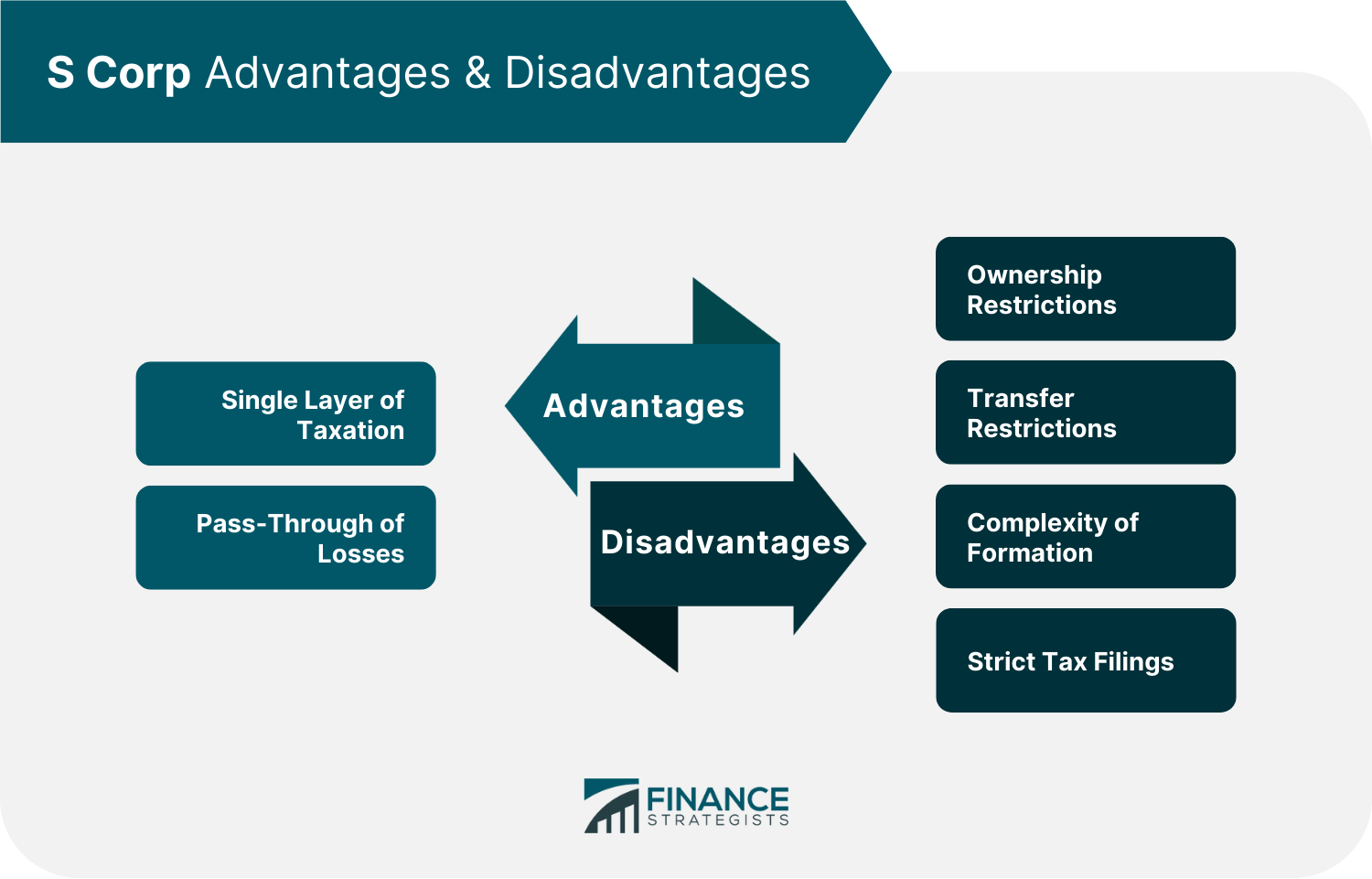

S Corp Advantages

S Corp Disadvantages

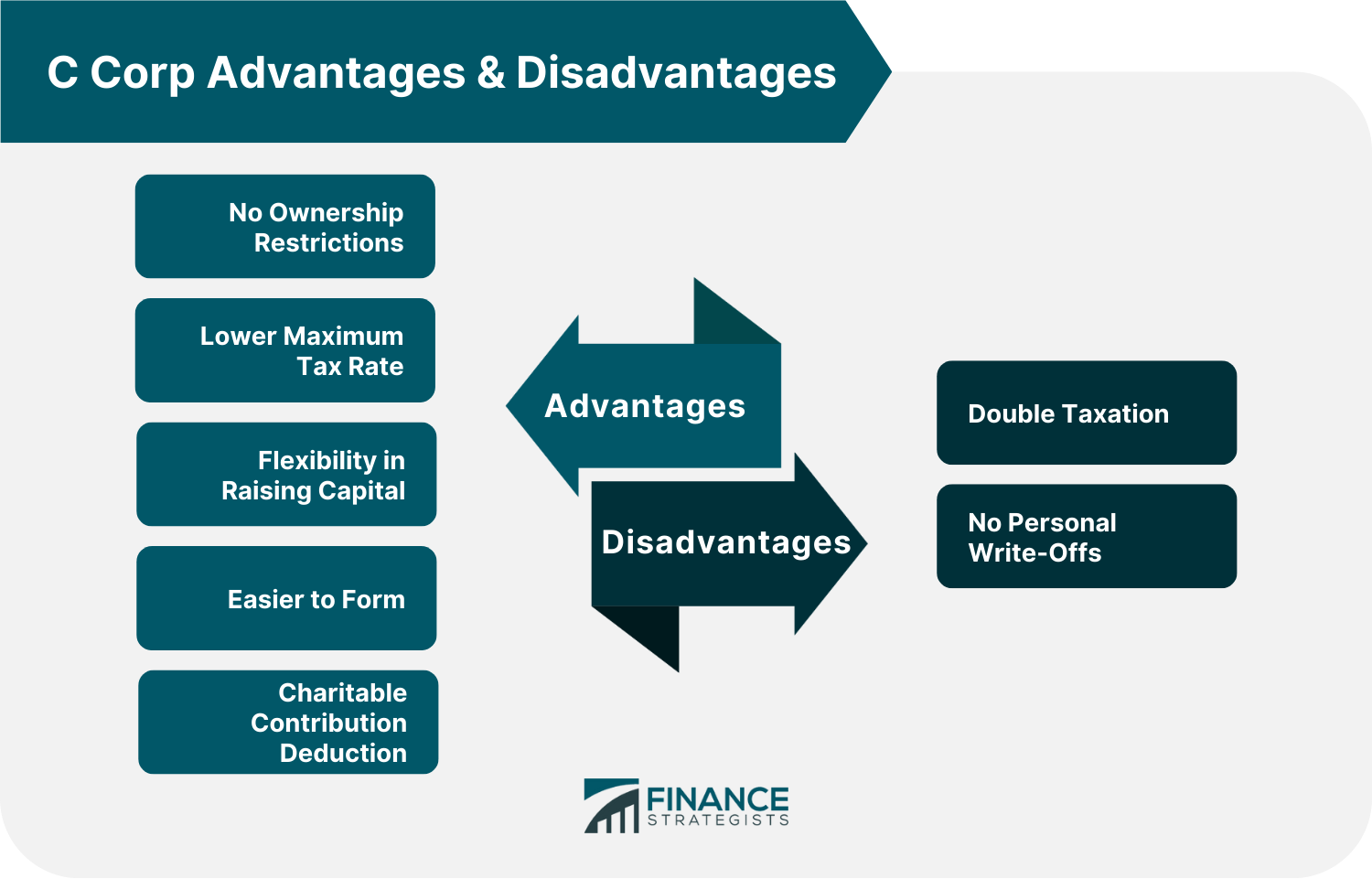

C Corp Advantages

C Corp Disadvantages

S Corp vs C Corp: Which Should You Choose?

Alternatives to S Corp and C Corp

The Bottom Line

S Corp vs C Corp FAQs

The corporation's classification can be found on the business returns form, which is annually filed. C Corporations submit IRS Form 1120, whereas S Corporations submit Form 1120-S. Another way of knowing is to call the IRS Business Helpline. The IRS can evaluate the business file to determine if the firm is a C Corporation or an S Corporation.

In general, C Corps pay more taxes because of double taxation. S Corps may pay fewer taxes because of their tax benefits and deductions.

An S Corp is the appropriate option for new firms that anticipate some losses. S corporations allow owners to pass-through losses and deduct them on their personal tax returns. Also, S Corp should be chosen by owners who want to avoid double taxation and benefit from tax advantages and deductions.

The key differences between S Corp and C Corp are based on how they are established, taxed, the number of owners, the type of stocks and shareholders, and the difficulty in financing.

There is no clear-cut and definitive answer to this question, as the best corporation for a business will vary depending on factors like size, shareholders' preferences and ownership, and the company's profits.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.