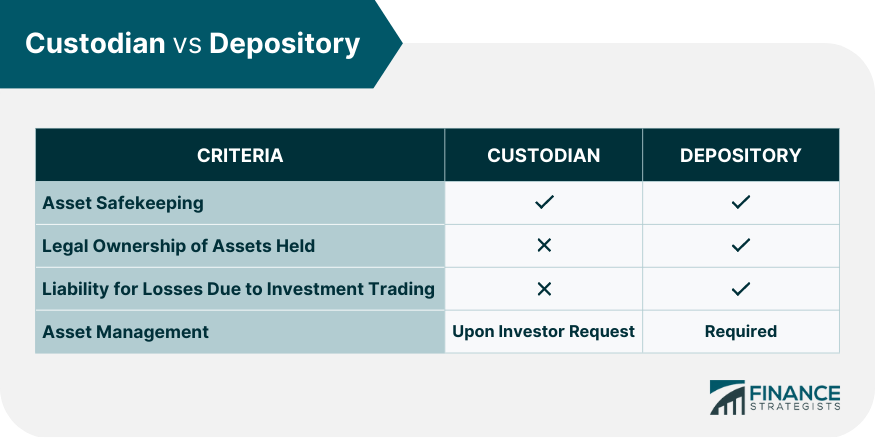

A custodian is a financial institution or professional firm that holds financial assets for individuals, families, or institutional investors. They have physical possession of securities and other assets, such as stocks, bonds, certificates of deposit (CDs), commodities, jewelry, and art. Custodians are also responsible for record-keeping, managing cash flows, and collecting dividends. They may also be asked to buy and sell securities. By performing such services, custodians protect the interests of investors. They are also critical to the successful operation of many large-scale investment funds, mutual funds, pension plans, individual retirement accounts (IRAs), 401(k) plans, and other managed portfolios. Custodial services generally involve four key elements: safekeeping the assets, accounting for asset activity, providing regulatory compliance support, and offering additional value-added services such as foreign currency exchange or cash management. They are responsible for the safekeeping and administration of the custody of securities such as stocks or bonds. It includes recording ownership, collecting dividends and interest payments, and providing monthly or quarterly account statements. Sometimes, investors ask custodians to trade securities on their behalf. Thus, custodians may act as brokers, ensuring that the asset traded goes to the right owner and the investor is paid accordingly. Custodians have a fiduciary responsibility to their clients, meaning they must put a client’s interests first and ensure all transactions comply with applicable laws and regulations. Lastly, custodians may be responsible for value appraisal regarding other assets, such as jewelry or art. At the same time, they insure against loss or damage and provide periodic reports to document its value over time. Fees vary depending on the custodian. Generally, these fees include either a flat rate or an account balance fee, such as a percentage of total assets under management (AUM). Depending on the account size and fee structure, this fee usually ranges from 0.2% to 1%. When brokerage firms act as custodians, they typically waive safekeeping fees and earn commission or transaction fees for the execution of investment trades instead. Some custodians also charge transaction fees for opening, transferring funds, or making deposits or withdrawals from an individual’s account. Custodians may also charge maintenance fees for other services, such as online banking, bill payments, tax forms, or account statements. Custodial services help ensure the safety and security of your assets. Consider the following before hiring a custodian: A custodian should be easy to work with and offer multiple communication methods, including phone calls, text, email, and live chat. Look for a custodian who is available when you need help or answers to questions. Also, consider the accessibility of the office location of the custodian. It is important to consider fees, as they can add up quickly. Some custodians may charge a flat fee, while others may charge fees based on the number of transactions or trades you make in a given period. Additional charges for wire transfers or check deposits may also be added. Different custodians offer different services and products. For example, if you are investing in stocks, exchange-traded funds (ETFs), or mutual funds, look for a custodian who provides trading and research tools. In addition, a helpful customer support service is always preferable. The specific technology platform they use can mean flexibility and ease of access, especially for online transactions. It also gives you an idea of how the custodian adapts to innovation — a good sign that adds to your confidence and peace of mind. Finally, make sure to get the help of a qualified financial advisor. They can provide further insight into different custodians and their services and help you make an informed decision based on your specific financial needs and goals. Custodians and depositories both provide asset-holding services. A key difference lies in their responsibility over such assets. A depository typically has legal ownership and controlling power over the assets. Custodians do not. Depositories must perform asset management and maintain, issue, buy, and sell assets and securities in their care according to legal and regulatory guidelines. Custodians only do so when told by investors. Depositories are responsible for any losses incurred from investment activities. On the other hand, custodians are only expected to ensure that trades push through and are only liable for general losses, damage, or negligence. While custodians maintain custody of assets and financial securities, depositories extend the scope of a custodian's services. A securities depository that stores financial securities allows for book-entry transfers of those assets and clearing and settlements. For instance, the Depository Trust and Clearing Corporation (DTCC) offers clearing and settlement services and acts as a custodian for the maintained securities. Custodians provide safekeeping for an investor's assets. They keep records, manage cash flows, and report account statements. They may also manage investments and act as brokers on behalf of their clients. Like depositories, they play a crucial role in protecting your assets. However, they have less liability and control over the assets held in their care. In choosing a custodian, consider how accessible they are, the fees they charge, their service offerings, and the technology platform they use. It is also essential to seek the advice of a qualified financial advisor to guide and advise you in decision-making.What Is a Custodian?

How Custodians Work

How Much Do Custodial Fees Cost?

Factors to Consider When Choosing a Custodian

Accessibility

Custodial Fees

Product Offerings

Technology Platform

Custodian vs Depository

Final Thoughts

Custodian FAQs

A custodian provides safekeeping, asset management, record-keeping, and financial transaction processing for investors. They may also act as brokers in securities trading. The custodian also records any changes to the account and can provide timely information to clients about their investments.

Custodians are vital because they offer protection and oversight to prevent mismanagement or fraud. They ensure that financial assets are kept secure and that the asset owner's interests are protected.

Custodians typically make money by charging a fee for their services. These fees are usually based on the assets under management, although some custodians may also charge an annual or transaction-based fee or earn commissions.

A key difference is in the responsibility and control of assets held. Depositories have legal ownership, power, and liability for the different assets in their safekeeping. While both are responsible for safeguarding assets, custodians are only liable for general losses, damage, or negligence and not for losses incurred through trading.

It depends on your assets, the type of investments you want to make, and how much risk you take. A custodian will likely be required if you invest in stocks, bonds, mutual funds, exchange-traded funds (ETFs), or other registered securities.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.