Immediate Steps to File Back Taxes

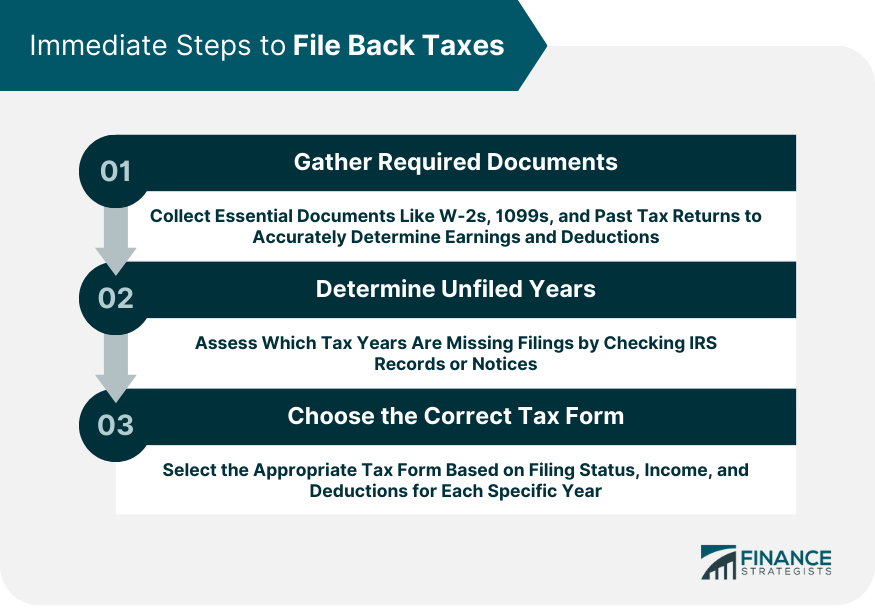

Gathering Required Documents

Before diving into the mechanics of filing back taxes, one must first understand the integral role of documents.

Just as constructing a building requires the right materials, filing back taxes mandates precise and accurate documentation.

W-2s, 1099s, or Other Income Statements

W-2s and 1099s act as evidence of your yearly earnings. These forms are typically sent by employers, clients, or other income sources.

Without them, it’s challenging to determine how much tax is owed accurately. If you've misplaced them, consider reaching out to the issuer or checking if they're available online.

Previous Tax Returns for Reference

A reference point is vital. Previous tax returns can offer insights into deductions, credits, or other factors you might have overlooked. They act as templates, reminding taxpayers of categories or details specific to their financial situation.

Receipts for Deductions and Credits

Tax deductions and credits can significantly reduce the amount of money owed. Keep a meticulous record of receipts, especially if you’re itemizing deductions.

This not only helps in reducing taxable income but also serves as proof should the IRS question any claims.

Records of Tax Payments or Withholdings

Ensure you're not paying twice! Past records of tax payments or withholdings can be subtracted from the total amount owed. This step is paramount in avoiding potential overpayments.

Determining Which Years Are Unfiled

An essential step in the back tax filing process is understanding the scope of the task ahead.

Checking With the IRS or Relevant Tax Authority

For those unsure about which years remain unfiled, the IRS or the local tax authority can provide this information. Often, they will have records or notices sent about any discrepancies.

Reviewing Personal Records and Financial Statements

Complementing the official channels, personal records are a goldmine. By sifting through old bank statements, pay stubs, or financial documents, one can gauge which tax years might be missing crucial filings.

Choosing the Right Tax Form

Not all tax years are the same, and neither are their respective forms.

Depending on Filing Status, Income, and Available Deductions

The specifics of your tax situation will dictate which form to use. Factors such as marital status, income level, and the nature of deductions can influence this choice.

Ensuring the Use of Forms Specific to Each Year in Question

Tax laws evolve. Consequently, tax forms get updated to reflect these changes. Ensure that for each year of back taxes you’re addressing, you're using the specific form for that year.

Understanding Penalties and Interest in Filing Back Taxes

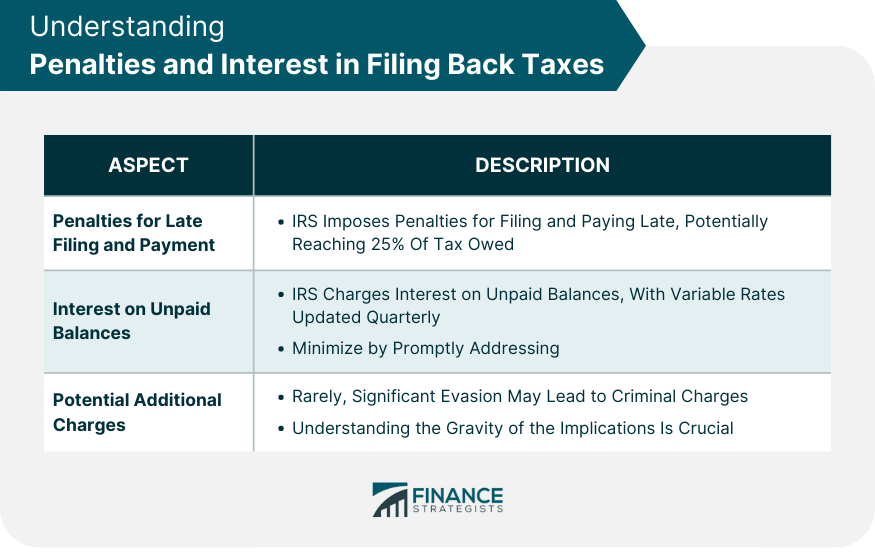

The consequences of late tax filings aren’t merely bureaucratic—they're financial.

Calculation of Penalties for Late Filing and Late Payment

The IRS levies two main penalties: one for filing late and another for paying late. These can quickly add up, sometimes reaching up to 25% of the tax owed.

Interest Rates Applied to Unpaid Balances

Beyond penalties, the IRS charges interest on unpaid balances. This rate can change quarterly, making it essential to stay updated and address back taxes promptly to minimize accruing interest.

Potential for Additional Charges or Criminal Penalties

In extreme cases, especially with significant amounts or deliberate evasion, criminal charges can be filed. While rare, understanding the gravity of these implications is vital.

Consulting a Tax Professional in Filing Back Taxes

Benefits of Hiring a CPA, Tax Attorney, or Enrolled Agent

These professionals can offer guidance, navigate the labyrinth of tax laws, and even negotiate on your behalf. Their expertise can often save taxpayers more money in the long run than the upfront cost of hiring them.

How Professionals Can Negotiate With the IRS or Relevant Authority

Tax professionals have tools and knowledge that the average taxpayer doesn’t. They can set up payment plans, reduce penalties or interest, and in some cases, lower the overall debt through mechanisms like Offers in Compromise.

Evaluating Costs vs Potential Savings

Though hiring help comes at a price, the potential for savings, both in money and stress, often outweighs the initial investment.

Filing Back Taxes

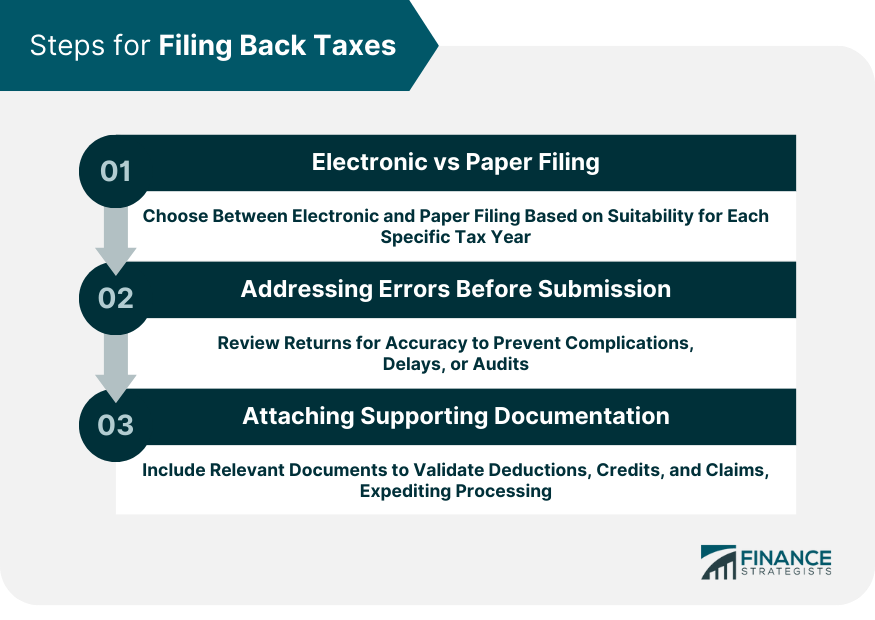

Electronic vs Paper Filing

While electronic filing offers convenience and quicker processing, certain back taxes might require paper filing. It's essential to determine which method is suitable for each tax year in question.

Addressing Errors or Discrepancies Before Submission

Accuracy is paramount. Before submitting, review returns meticulously. Any errors can lead to further complications, delays, or potential audits.

Ensuring to Attach Any Supporting Documentation

Always back your claims. Attach relevant documents that support your deductions, credits, or other declarations, as they will provide validity to your claims and speed up the processing time.

Setting up Payment Plans or Negotiating Settlements

Exploring IRS Options Like Installment Agreements

If paying the total amount is overwhelming, the IRS offers installment plans. These allow taxpayers to pay their debt in manageable chunks over time.

Understanding the Offer in Compromise (OIC) Process

For those facing significant financial hardship, the IRS's Offer of Compromise might be an option. It allows taxpayers to settle their debt for less than the full amount owed.

Considering Other Alternatives Like Temporarily Delaying Collection

In situations where immediate payment might cause significant hardship, the IRS might allow for a temporary delay. Though interest and penalties will continue to accrue, it offers a short reprieve.

Staying in Compliance Moving Forward

Organizing Records for Future Tax Years

Develop a system. Store receipts, statements, and other pertinent documents systematically, ensuring easy access when tax season rolls around.

Setting Reminders for Annual Tax Deadlines

Avoid past mistakes by marking tax deadlines prominently on calendars. Modern tools and apps can send reminders, ensuring punctuality.

Making Estimated Tax Payments if Required

For freelancers or those with irregular income, quarterly estimated tax payments can help avoid end-of-year tax surprises.

Conclusion

Filing back taxes, while daunting, is a navigable process when approached methodically. At the heart of this endeavor lies the criticality of documentation, from income statements like W-2s to previous tax returns.

Recognizing unfiled tax years through both official channels and personal records establishes the foundation for corrective action. With the dynamic nature of tax forms and regulations, ensuring accuracy and year-specific compliance is paramount.

Penalties, interest, and the potential for more severe consequences underline the importance of timely resolution. Yet, there's solace in the fact that expert guidance, from CPAs to tax attorneys, can provide valuable insights and negotiation power.

Once the back taxes are filed, options like installment plans or the Offer in Compromise provide avenues for manageable settlements.

Ultimately, the lesson is clear: with proactive organization and awareness, future tax compliance becomes a more straightforward endeavor.

How to File Back Taxes FAQs

Back taxes refer to taxes that were not paid when due, typically from previous years. These can accumulate interest and penalties over time, increasing the amount owed.

You can check with the IRS or your local tax authority for a record of your filed returns. Additionally, reviewing your personal financial records and previous tax documents can help identify any missing years.

Yes. By consulting with a tax professional, you can explore options like negotiating with the IRS, setting up payment plans, or potentially qualifying for programs like the Offer in Compromise that can reduce the amount owed.

The IRS and many local tax authorities offer payment plans, such as Installment Agreements, which allow taxpayers to pay their owed amounts in manageable installments over time. Additionally, in certain cases of financial hardship, you might be able to settle for less than the total owed through mechanisms like the Offer in Compromise.

Staying organized is key. Keep all pertinent tax documents, set reminders for tax deadlines, and, if required, make estimated tax payments throughout the year. If unsure, consulting with a tax professional can provide guidance tailored to your specific situation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.