Every tax season, a myriad of Americans face the critical decision of how to file their taxes. The IRS presents a buffet of filing statuses, such as single, head of household, and for married couples—joint or separate filing. The dynamics of each status come with a unique set of rules, tax rates, and associated benefits. While married individuals always have the option to file separately, most choose the path of filing jointly due to its perceived benefits. Yet, understanding the nuances of each choice, along with its pros and cons, can greatly impact a couple's financial landscape. Selecting the right tax filing status impacts your financial obligations, affecting tax amounts, credits, and required forms. It's crucial to understand each status's pros and cons. A well-informed choice optimizes financial benefits, while a poor one can result in added financial strain. Opting for a "married filing jointly" status implies a married couple is choosing to combine their incomes, credits, and deductions when filing taxes. To be eligible, couples need to be legally recognized as married by the final day of the tax year. It's a combined approach, often simplifying the tax process. Yet, as with most financial strategies, it's essential to recognize when this approach is advantageous. Several factors play into its efficacy, including the income disparity between partners, potential credits, and the unique financial situations each partner brings to the table. Larger Standard Deduction: Filing jointly often allows couples to benefit from a higher standard deduction, reducing taxable income. Access to Tax Credits: Joint filers can be eligible for several tax credits such as the Earned Income Tax Credit and the Child and Dependent Care Credit. Favorable Tax Rate: For couples with significant income differences, joint filing might result in a more advantageous tax rate. Spousal IRA Contributions: This status enables the higher-earning spouse to contribute to the other's IRA, boosting retirement savings. Joint Liability: Both partners are held accountable for the accuracy of their tax return and any resulting tax debts. Higher Tax Brackets for High Earners: Couples with combined high incomes might find themselves in a steeper tax bracket. Loss of Specific Tax Benefits: Some tax benefits might phase out based on combined income levels. Risk of Alternative Minimum Tax: High-earning joint filers might be more susceptible to the AMT, ensuring they pay a minimum amount of tax. Contrary to joint filing, "married filing separately" allows each spouse to stand their financial ground. Each partner's income, deductions, and credits are reported independently. While this method might seem counterintuitive to the spirit of marriage, it caters to specific scenarios where financial independence and clarity are sought. In essence, filing separately ensures that each spouse's tax responsibility is independent of the other's. It becomes a pivotal strategy when looking to protect oneself from potential financial missteps of the partner or when navigating intricate financial terrains. Protection From Shared Financial Liabilities: Each spouse is accountable only for their tax duties, ideal when one faces financial issues like large debts. Potential for Certain Deductions: With separate filing, certain deductions like significant medical expenses might be more attainable. Favorable Tax Scenarios for High Earners: High-income earners might avoid the topmost tax brackets when filing separately. Reduced AMT Risk: Separate incomes might lessen the risk of the Alternative Minimum Tax. Loss of Specific Tax Credits: Separate filers may miss out on certain tax credits available to joint filers. Possible Higher Tax Rates: The tax rate for separate filers might sometimes be less advantageous. Limited Itemized Deductions: Many itemized deductions are not accessible for separate filers. Inability for Spousal IRA Contributions: Separate filing precludes one spouse from contributing to the other's IRA, which can affect retirement planning. The interplay of incomes under the two filing statuses drastically influences tax brackets. While pooling incomes under joint filing can potentially place the couple in a lower or higher bracket, filing separately keeps each income confined to its bracket. Especially when both spouses rake in significant incomes, separate filing can prevent bracket escalation. In contrast, couples with vastly different earnings might find the scales tipping in favor of joint filing. The combined income, in such cases, could result in a more benevolent tax rate. Navigating the labyrinth of deductions and credits becomes easier with a compass pointing towards the most beneficial filing status. Joint filers, with their combined resources, often access a broader spectrum of tax breaks. In stark contrast, separate filers might find certain doors closed—like the Earned Income Tax Credit and student loan interest deductions. Therefore, when chartering the tax seas, it's paramount for couples to evaluate which tax reliefs are more germane to their situation and how their chosen status steers their course. Beyond numbers, the emotional and financial security of a couple plays a starring role in the tax filing drama. Joint filers, while reaping the benefits of combined resources, also shoulder each other's financial liabilities. Conversely, a separate filing approach carves out distinct financial territories, potentially shielding one partner from the other's financial storms. Deciphering where one's comfort lies—in shared responsibilities or individual accountability—can significantly impact the couple's financial harmony. The ripple effects of a tax filing decision extend into the future, influencing subsequent financial planning. Joint filing, with its amalgamation of resources, might offer a better foothold when securing loans or mortgages. Contrarily, maintaining individual financial identities, as seen with separate filers, can be a strategic move in more complex financial scenarios. The dance of numbers—where combined incomes land on the tax bracket spectrum—plays a pivotal role in the decision-making process. Couples with similar high incomes might gravitate towards separate filing to avoid catapulting into steeper brackets. Conversely, couples with differing earnings could lean into joint filing to harness its benefits. The allure of credits and deductions, both in their range and magnitude, often steers the filing decision. A thorough assessment of which tax reliefs resonate most with a couple's circumstances, and the access provided by their chosen status, is vital. Personal financial terrains—marked by debts, assets, and liabilities—often dictate the filing approach. Especially when one partner's financial landscape is marred by debts or obligations, the allure of separate filing gains momentum. It's an intricate balance between maximizing benefits and minimizing risks. Projecting into the future, couples need to appraise how their filing choice today shapes tomorrow's dreams and strategies. Whether it's a dream home, significant investments, or other financial milestones, the choice between joint or separate filing can chart the course. In summation, whether to file jointly or separately isn't a black and white decision. The hues of individual circumstances, current benefits, and future aspirations paint a unique picture for every couple. Delving deep, consulting experts, and evaluating both present and future scenarios can illuminate the best path forward. Choosing between filing taxes jointly or separately is a multifaceted decision that greatly impacts a couple's financial scenario. The IRS offers a range of filing statuses, each with distinct rules, rates, and benefits. While jointly filing often presents attractive perks such as a higher standard deduction and access to certain tax credits, it also comes with the weight of joint liabilities. On the other hand, filing separately offers financial independence, which can be pivotal for those wanting to protect themselves from a partner's financial liabilities. However, this might limit certain deductions and tax credits. The decision largely hinges on combined income levels, potential deductions, individual financial situations, and future financial plans. Every couple's circumstances are unique, and it's vital to evaluate both the immediate and long-term implications. Expert consultation can provide clarity, ensuring a choice that optimizes financial benefits and aligns with future aspirations.Overview of Tax Filing Status Options

Overview of Filing Taxes Jointly

Definition and Eligibility

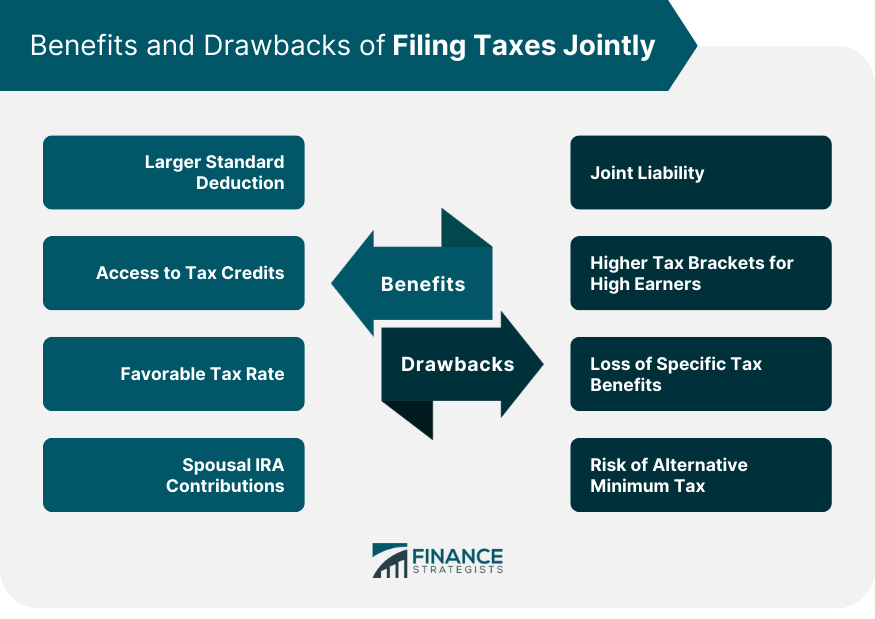

Key Benefits of Filing Jointly

Potential Drawbacks of Filing Jointly

Overview of Filing Taxes Separately

Definition and Eligibility

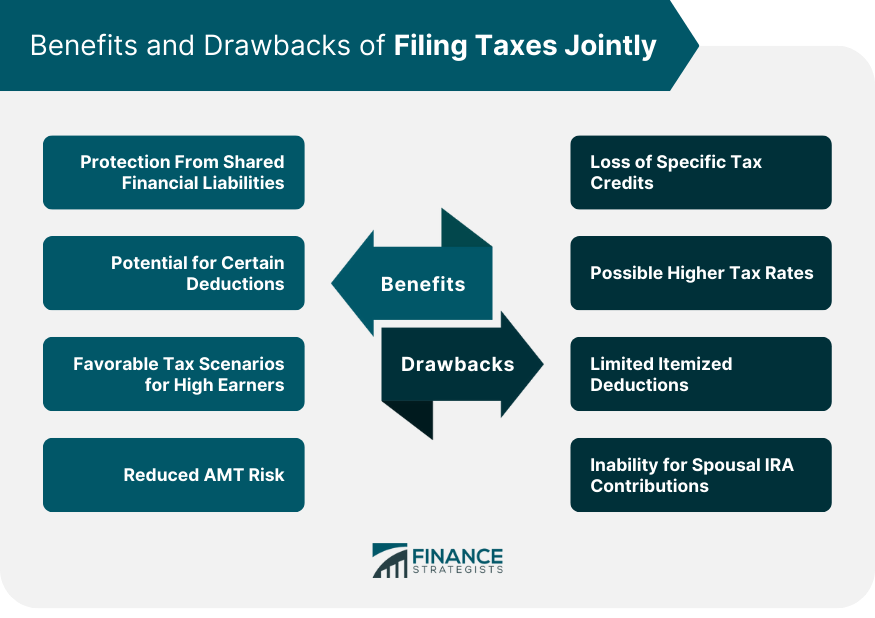

Key Benefits of Filing Separately

Potential Drawbacks of Filing Jointly

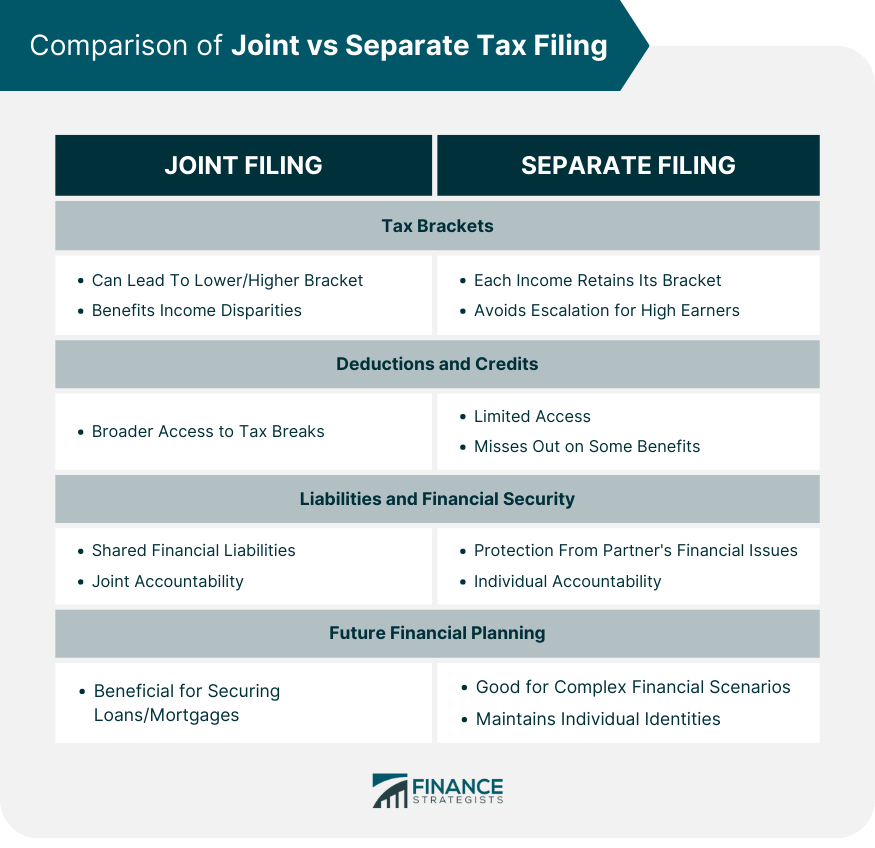

Comparison of Joint vs Separate Tax Filing

Comparative Financial Outcomes Based on Tax Brackets

Impact on Deductions and Credits

Considerations Regarding Liabilities and Financial Security

Implications for Future Financial Planning

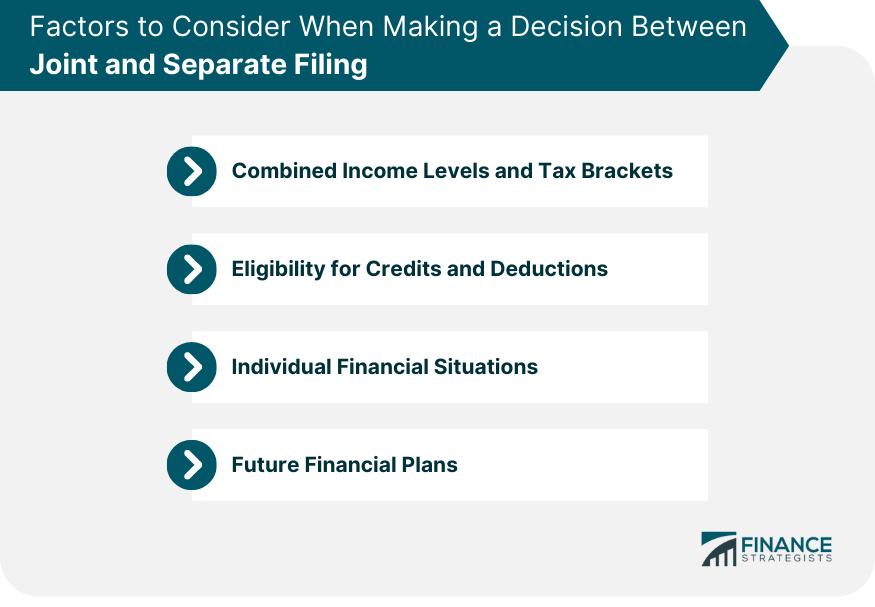

Factors to Consider When Making a Decision Between Joint and Separate Filing

Combined Income Levels and Tax Brackets

Eligibility for Credits and Deductions

Individual Financial Situations

Future Financial Plans

Bottom Line

Is It Better to File Taxes Jointly or Separately? FAQs

Joint filing often offers larger standard deductions, access to specific tax credits, favorable tax rates for varied incomes, and eligibility for spousal IRA contributions.

Yes, joint filing can lead to joint liability issues, potentially higher tax rates for high earners, phase-outs of some tax benefits, and exposure to the Alternative Minimum Tax.

Filing separately provides distinct financial liabilities, potential deductions, benefits for high earners in particular scenarios, and a reduced AMT risk based on individual incomes.

Separate filers may miss out on certain tax credits, face a potential higher tax rate, have limitations on itemized deductions, and can't contribute to a spousal IRA.

Your tax filing choice can influence future loan approvals, investment strategies, and other financial milestones, based on combined resources or individual financial standing.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.