When you sell your home for more than you paid for it, the IRS typically considers that profit as a capital gain. But the government also acknowledges that a home is more than an investment. It's the roof over your head, the nest where you raise your kids and the hub of your life. To reflect this reality, the tax code offers a home sale exclusion from capital gains tax. This means that, up to a certain limit, the profit from the sale of your primary residence may be tax-free. Specifically, the home sale exclusion allows you to exclude up to $250,000 (or $500,000 for a married couple filing jointly) of capital gains on the sale of your home from your income.

Not every home sale qualifies for this favorable tax treatment. There are specific conditions you must meet to be eligible for the home sale exclusion. The key criteria revolve around the nature of the property, your ownership, and your use of it. Firstly, you must meet the 'ownership test' and the 'use test.' The ownership test requires you to have owned the home for at least two years during the five years leading up to the sale. Meanwhile, the use test requires you to have lived in the home as your primary residence for at least two years during the same five-year period. These two years of residency do not have to be continuous. You could live in the home for a year, rent it out for three years, then move back in for a year, and still qualify for the exclusion. Another essential condition to be aware of is that you generally can't use the home sale exclusion if you've claimed it on the sale of another home within two years of the current sale. However, exceptions apply if you had to change your residence due to health, employment, or certain unforeseen circumstances. The two-year rule is one of the key pillars of the home sale exclusion. However, it's not just about meeting the ownership and use tests. There are additional considerations and exceptions to this rule that can affect your eligibility for the home sale exclusion. The two-year rule is basically what we've already outlined in the 'ownership' and 'use' tests. But it's important to delve a little deeper into its implications. For instance, the two-year rule means you don't have to be living in the home at the time of sale to qualify for the exclusion. There are also exceptions to the two-year rule. If you have to sell your home before you've lived in it for two years due to health reasons, changes in employment, or other unforeseen circumstances, you may still qualify for a partial exclusion. This is determined on a case-by-case basis, and the amount of the exclusion is usually proportional to the time of residency. The home sale exclusion isn't an all-or-nothing deal. There are several exceptions to the general rules that can either qualify you for the exclusion when you otherwise wouldn't be or disqualify you when you'd generally be eligible. Understanding these exceptions can help you navigate the tax implications of your home sale effectively. One of the most noteworthy exceptions is the unforeseen circumstances exception. This applies when you must sell your home due to situations you could not have anticipated before buying and occupying the house. Such unforeseen circumstances can include a divorce or legal separation, natural or man-made disasters resulting in a casualty to your home, or the death of a qualified individual. Another exception comes into play if you have to move because of a job-related issue. If your new workplace is at least 50 miles farther from your home than your old workplace was, you're considered as having moved due to work. The job-related exception can be particularly useful for people whose work requires frequent relocations. Health-related exceptions allow you to claim the home sale exclusion if you've had to move due to health reasons. This could be because a doctor recommended a change in residence for the sake of your health or to obtain or provide necessary medical care for a family member. When you sell your home, one factor that can affect the exclusion amount is depreciation recapture. If you've ever used part or all of your home for business or rental purposes, you've probably claimed depreciation deductions on your tax returns. When you sell the property, you'll need to recapture that depreciation. Depreciation recapture is essentially a tax on the gain resulting from the depreciation deductions you've taken on your property. It's designed to prevent you from double-dipping on tax benefits, as depreciation deductions reduce your taxable income while the home sale exclusion potentially exempts your profit from tax. The part of the profit of your home sale that's attributed to depreciation deductions taken after May 6, 1997, can't be excluded from your taxable income. This portion of the gain is subject to a maximum tax rate of 25%, which is higher than the maximum long-term capital gains tax rate of 20%. While you can't completely avoid depreciation recapture when you've used your home for business or rental purposes, there are a few strategies to minimize its impact: Accurate Record-Keeping: Keep accurate records of your home's use. It's easier to claim the home sale exclusion for the parts of your home and the periods when it was used as your primary residence. 1031 Exchange: If you're selling a rental property, consider a 1031 exchange to defer capital gains and depreciation recapture taxes. Understanding your home's tax basis is crucial for determining the amount of capital gain that's potentially subject to tax upon sale. It can affect the home sale exclusion, especially if you've made significant improvements to your home or had other adjustments to the original cost. The tax basis of your home is typically its cost when you bought it, plus purchase expenses like transfer taxes and fees. You can also add to the tax basis the cost of significant home improvements you've made over the years. However, repairs and maintenance costs don't increase your tax basis. Several factors can adjust your tax basis, affecting your capital gain calculation: Home Improvements: As mentioned, substantial home improvements increase your tax basis. Depreciation: If you've used your home for business or rental purposes and claimed depreciation deductions, these deductions decrease your tax basis. Casualty Losses: If you suffered a casualty loss for which you took a tax deduction, it reduces your tax basis. Exclusion of Gain on a Previous Home Sale: If you used a previous tax rule to exclude gain on the sale of a previous home before May 7, 1997, this exclusion reduces your tax basis. The home sale exclusion from capital gains tax is a significant provision in U.S. tax law that allows homeowners to potentially save a considerable amount of money when selling their primary residence. It allows the exclusion of up to $250,000 ($500,000 for joint filers) of capital gains from one's income. Eligibility is based on the ownership and use tests, requiring a minimum of two years of ownership and residence over the last five years. Exceptions exist for less than two years of residence due to unforeseen circumstances, including health or job-related moves. Homeowners must also be aware of depreciation recapture if the property was used for business or as a rental. Finally, understanding one's home tax basis is crucial for calculating potential taxable capital gain. By understanding and navigating these aspects, homeowners can optimize their financial outcomes when selling their primary residence.Home Sale Exclusion From Capital Gains Tax: Overview

Eligibility for Home Sale Exclusion From Capital Gains Tax

Ownership and Use Tests

Frequency of Claiming the Exclusion

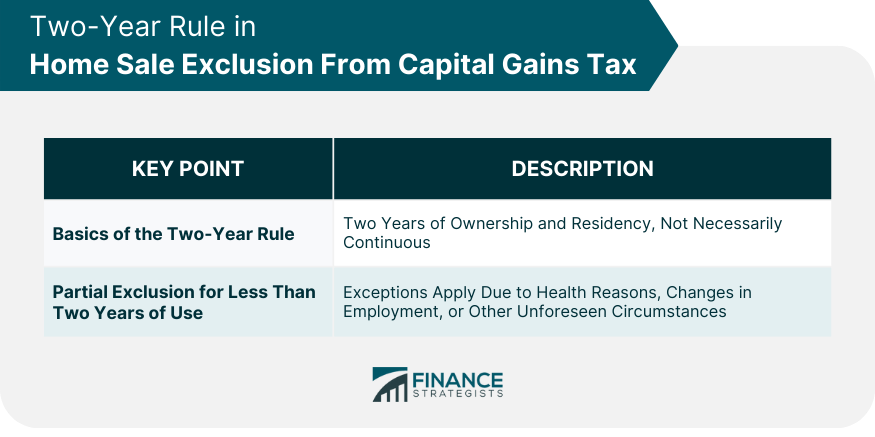

Two-Year Rule in Home Sale Exclusion From Capital Gains Tax

Basics of the Two-Year Rule

Partial Exclusion for Less Than Two Years of Use

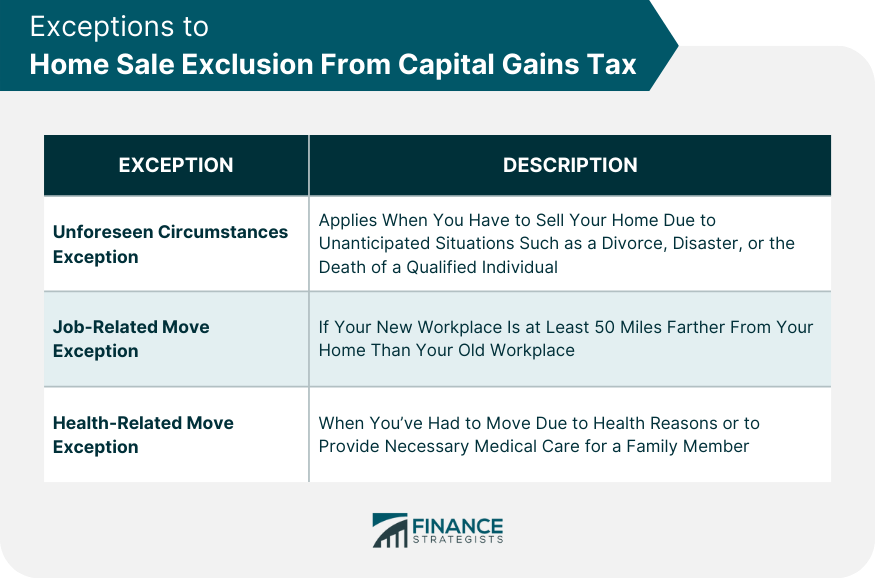

Exceptions to Home Sale Exclusion From Capital Gains Tax

Unforeseen Circumstances Exception

Job-Related Move Exception

Health-Related Move Exception

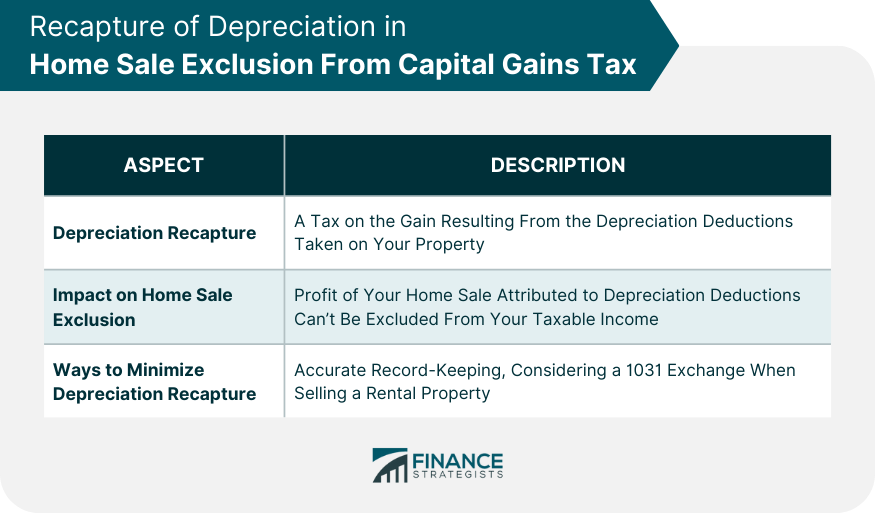

Recapture of Depreciation in Home Sale Exclusion From Capital Gains Tax

Depreciation Recapture

Impact on Home Sale Exclusion

Ways to Minimize Depreciation Recapture

Role of Tax Basis in Home Sale Exclusion From Capital Gains Tax

Understanding Tax Basis

Adjustments to Tax Basis

Conclusion

Home Sale Exclusion From Capital Gains Tax FAQs

The home sale exclusion is a provision in the U.S. tax code that allows homeowners to exclude up to $250,000 of capital gains on the sale of their primary residence from their income ($500,000 for married couples filing jointly).

To be eligible for the home sale exclusion, you must pass two tests: the ownership and use tests. These require you to have owned and lived in the home as your main home for at least two years during the five-year period ending on the date of the sale.

Yes, you can use the home sale exclusion multiple times over your lifetime, but you cannot use it more than once every two years.

The home sale exclusion typically does not apply to rental or investment properties. It primarily applies to your primary residence. However, partial exclusions may apply in some cases where the property was used as both a rental and a primary residence.

The home sale exclusion only applies to gains from the sale of your home. If you sell your home at a loss, you generally cannot deduct the loss from your income.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.