Estimated tax payments are an important aspect of financial planning and tax management for individuals and businesses. They serve as a way for taxpayers to pay their income tax and self-employment tax obligations throughout the year, rather than in a lump sum at the end of the year. Estimated tax payments are typically required by the IRS for taxpayers who receive income that is not subject to withholding, such as self-employment income, rental income, and investment income. By making these payments throughout the year, taxpayers can avoid penalties for underpayment of taxes and ensure that they have enough money set aside to pay their tax bill when it is due. For businesses, estimated tax payments may also be required to cover obligations such as corporate income tax, payroll tax, and other taxes. Making these payments on time and in the correct amount can help businesses to avoid costly penalties and interest charges, and maintain good standing with the IRS. It is important for taxpayers to carefully calculate their estimated tax payments to ensure that they are paying the correct amount and avoiding underpayment penalties. This may require working with a tax professional or using online tax calculators to estimate tax liabilities. Self-employed individuals, such as freelancers and independent contractors, are often required to make estimated tax payments since they typically do not have taxes withheld from their income. Business owners, including partners in partnerships and members of multi-member LLCs, may be responsible for making estimated tax payments on their share of business income. Investors who receive significant income from interest, dividends, or capital gains may need to make estimated tax payments to cover their tax liability. Retirees receiving income from pensions, annuities, or other sources not subject to withholding may be required to make estimated tax payments. Individuals who receive substantial income not subject to withholding, such as alimony or rental income, may need to make estimated tax payments. In cases where an individual's tax withholding is not sufficient to cover their tax liability, estimated tax payments may be necessary to avoid penalties. To calculate estimated tax payments, taxpayers must first determine their total annual income from various sources: Business Income: Income earned from self-employment or business operations Interest and Dividends: Income generated from investments, such as interest-bearing accounts and stock dividends Capital Gains: Income resulting from the sale of investments or other assets Rental Income: Income generated from rental properties Retirement Income: Income received from pensions, annuities, or other retirement plans Once the total annual income has been determined, taxpayers must calculate their taxable income by considering deductions, exemptions, and credits: Deductions: Expenses that can be subtracted from total income to reduce taxable income. Exemptions: Amounts that can be deducted from income for each taxpayer and dependent, reducing taxable income. Credits: Amounts that can be subtracted directly from the taxpayer's tax liability. After calculating taxable income, taxpayers must determine their tax liability based on the progressive tax brackets, self-employment tax, and alternative minimum tax (AMT). Once a taxpayer has calculated their taxable income, they must determine their tax liability by applying the appropriate tax rates based on the progressive tax brackets. The tax rates increase as income increases, with taxpayers in higher income brackets paying a higher percentage of their income in taxes. In addition to federal income tax, self-employed individuals may also be subject to self-employment tax, which is a Social Security and Medicare tax that is typically paid by both employers and employees. This tax is calculated based on self-employment income and is separate from federal income tax. Furthermore, some taxpayers may be subject to the alternative minimum tax (AMT), which is a parallel tax system designed to ensure that high-income taxpayers pay a minimum amount of tax regardless of deductions and credits. Taxpayers who are subject to the AMT must calculate their tax liability under both the regular tax system and the AMT system, and pay the higher amount. It is important for taxpayers to carefully calculate their tax liability to ensure that they are paying the correct amount and avoiding penalties for underpayment. This may require working with a tax professional or using tax software to calculate tax liabilities and identify potential deductions and credits. Taxpayers should consider any adjustments for refundable and non-refundable credits and tax-saving deductions to arrive at their final estimated tax payment. After calculating their taxable income and determining their tax liability, taxpayers should consider adjustments for refundable and non-refundable credits and tax-saving deductions to arrive at their final estimated tax payment. Refundable credits are credits that can be used to reduce tax liability to zero and receive a refund for any excess credit amount. Examples of refundable credits include the Earned Income Tax Credit and the Child Tax Credit. Non-refundable credits, on the other hand, can only be used to reduce tax liability to zero and cannot result in a refund. Examples of non-refundable credits include the Lifetime Learning Credit and the Foreign Tax Credit. Tax-saving deductions, such as those for charitable contributions, medical expenses, and retirement account contributions, can also reduce tax liability and help taxpayers to lower their estimated tax payments. By taking advantage of these deductions, taxpayers can lower their tax bill and keep more money in their pocket. It is important for taxpayers to carefully consider any adjustments for credits and deductions when calculating their estimated tax payments to ensure that they are paying the correct amount and maximizing their tax savings. This may require working with a tax professional or using tax software to identify potential deductions and credits and accurately calculate tax liabilities. Estimated tax payments are typically due on a quarterly basis, with specific deadlines falling in April, June, September, and January. Taxpayers with fluctuating or seasonal income can use the annualized income installment method to calculate their estimated tax payments based on their actual income for each quarter. Taxpayers should adjust their estimated tax payments if their income changes significantly during the year to avoid underpayment or overpayment. Taxpayers who underpay or pay their estimated taxes late may be subject to penalties. The Electronic Federal Tax Payment System (EFTPS) is a free, secure method for submitting estimated tax payments online. Taxpayers can schedule payments in advance and track their payment history. Direct Pay is another online payment option available through the IRS website, which allows taxpayers to make estimated tax payments directly from their checking or savings accounts. Taxpayers can also submit their estimated tax payments by phone using the Electronic Federal Tax Payment System (EFTPS) voice response system or other designated payment services. Estimated tax payments can be submitted through the mail by sending a check or money order, along with the appropriate payment voucher, to the IRS. Taxpayers living outside the United States have several options for submitting estimated tax payments, including EFTPS, Direct Pay, and international wire transfers. Taxpayers should regularly review their financial records to ensure accurate reporting and to make necessary adjustments to their estimated tax payments. Taxpayers can adjust their withholding from other income sources, such as wages or pensions, to help cover their estimated tax payment obligations. It is important for taxpayers to set aside funds throughout the year to cover their quarterly estimated tax payments. Working with a tax professional can help taxpayers navigate the complexities of estimated tax payments and ensure accurate calculations. Tax planning software can help taxpayers calculate their estimated tax payments and manage their financial records. Farmers and fishermen have unique rules and deadlines for estimated tax payments, which differ from those of other taxpayers. Individuals with fluctuating income, such as seasonal workers or freelancers, may need to adjust their estimated tax payments throughout the year based on their actual income. High-income taxpayers may be subject to additional taxes and have different thresholds for calculating their estimated tax payments. Nonresident aliens may be required to make estimated tax payments if they have U.S. source income not subject to withholding. Making accurate and timely estimated tax payments is crucial for avoiding penalties and managing tax liabilities. Taxpayers should be aware of their eligibility, payment schedules, and submission options to ensure compliance. By understanding the calculation methods, staying organized, and seeking professional assistance when needed, taxpayers can effectively manage their estimated tax payments and stay on track with their financial obligations.Estimated Tax Payments: Definition

Eligibility for Estimated Tax Payments

Self-Employed Individuals

Business Owners

Investors

Retirees

Individuals With Substantial Income Not Subject to Withholding

Situations Where Withholding Is Insufficient to Cover Tax Liabilities

Calculation of Estimated Tax Payments

Determining Total Annual Income

Calculating Taxable Income

Determining Tax Liability

Adjustments for Credits and Deductions

Payment Schedule and Due Dates

Quarterly Payment Deadlines

Annualized Income Installment Method

Adjusting Estimated Tax Payments for Changes in Income

Penalties for Underpayment or Late Payment

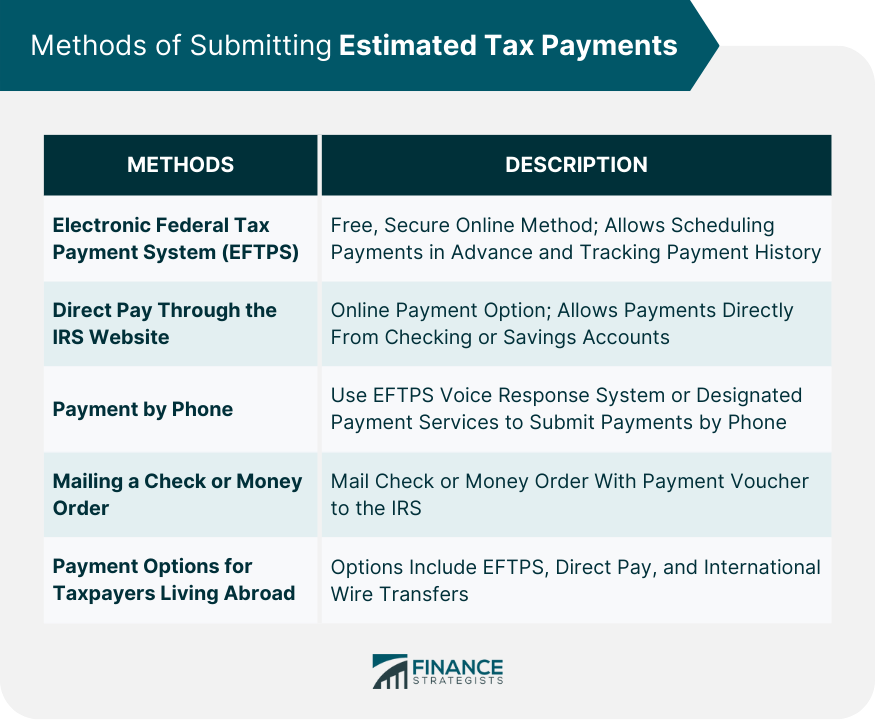

Methods of Submitting Estimated Tax Payments

Electronic Federal Tax Payment System

Direct Pay Through the IRS Website

Payment by Phone

Mailing a Check or Money Order

Payment Options for Taxpayers Living Abroad

Tips for Managing Estimated Tax Payments

Regularly Reviewing Financial Records

Adjusting Withholding From Other Income Sources

Saving for Quarterly Payments

Working With a Tax Professional

Utilizing Tax Planning Software

Special Circumstances

Estimated Tax Payments for Farmers and Fishermen

Estimated Tax Payments for Individuals With Fluctuating Income

Estimated Tax Payments for High-Income Taxpayers

Estimated Tax Payments for Nonresident Aliens

Conclusion

Estimated Tax Payments FAQs

Estimated tax payments are payments made by individuals, businesses, and other entities to the IRS on a quarterly basis to cover their tax liability for the year.

Individuals, sole proprietors, partners, and S corporation shareholders are required to make estimated tax payments if they expect to owe at least $1,000 in taxes for the year.

Estimated tax payments are due four times a year, on April 15th, June 15th, September 15th, and January 15th of the following year.

To calculate your estimated tax payments, you will need to estimate your income and tax liability for the year and use the IRS's Form 1040-ES worksheet or online calculator.

If you don't make estimated tax payments or underpay your estimated taxes, you may be subject to penalties and interest on the underpayment when you file your tax return.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.