Tax-efficient charitable giving refers to the practice of making charitable donations in a manner that optimizes the tax benefits associated with the contributions. This involves strategically planning and structuring charitable gifts to take advantage of available tax deductions, credits, and other incentives, with the goal of reducing the donor's overall tax burden. Tax-efficient charitable giving allows donors to make the most of their generosity by maximizing the amount of money that goes to the intended charitable organizations while minimizing the amount paid in taxes. When donors adopt tax-efficient giving strategies, they can increase the amount of their contributions without incurring additional out-of-pocket expenses. This allows the donor to provide more substantial support to their chosen causes. Tax-efficient giving enables donors to reduce their taxable income, resulting in lower tax liabilities. This can be especially beneficial for individuals in higher tax brackets. Incorporating tax-efficient charitable giving into personal financial planning can help individuals achieve their philanthropic goals while optimizing their financial health and estate plans. Cash donations are the most common form of charitable giving. They are straightforward, and donors can claim tax deductions for the amount given, subject to certain limitations. Donating appreciated securities, such as stocks, bonds, or mutual funds, can provide significant tax benefits. Donors can avoid capital gains taxes and claim a tax deduction for the fair market value of the donated asset. Donating real estate, like appreciated securities, can help donors avoid capital gains taxes and claim a tax deduction for the fair market value of the property. Donors can also contribute tangible personal property, such as art or collectibles, to a charitable organization. The tax deduction depends on the nature of the property and its relation to the charity's mission. A charitable bequest involves including a donation to a charity in the donor's will or estate plan. This type of donation can reduce estate taxes and ensure that the donor's philanthropic legacy lives on. DAFs are charitable investment accounts that provide an immediate tax deduction for contributions. Donors can make grant recommendations to eligible charities over time, and the funds can be invested for tax-free growth. DAFs may come with administrative fees and can lack the flexibility of other giving vehicles, such as private foundations. CRTs are irrevocable trusts that provide a stream of income to the donor or their beneficiaries for a specified period. At the end of the term, the remaining assets are transferred to the designated charity. CRTs offer tax deductions, capital gains tax avoidance, and potential income tax savings. CRTs can be complex to set up and administer, and they typically require significant upfront contributions. CLTs provide income to a charity for a specified period, after which the remaining assets are transferred back to the donor or their beneficiaries. CLTs can reduce estate and gift taxes and provide a stream of income to the chosen charity. Similar to CRTs, CLTs can be complex to set up and administer and typically require significant upfront contributions. Establishing a private foundation allows donors to create a lasting philanthropic legacy, exercise significant control over grant-making decisions, and provide family members with involvement in the foundation's management. Private foundations come with strict regulatory requirements, administrative costs, and a lower limit on tax deductions compared to other giving vehicles. The IRS provides guidelines for claiming charitable deductions on income tax returns. Donors must itemize deductions on their tax returns and ensure that the recipient organization qualifies for tax-deductible donations. There are limits on the amount of charitable deductions that can be claimed based on the donor's adjusted gross income (AGI). These limits can range from 20% to 60% of the AGI, depending on the type of donation and the recipient organization. Donors must maintain proper records of their charitable contributions to claim deductions. For cash donations, a bank record or a written acknowledgement from the charity is required. For non-cash donations, additional documentation, such as appraisals, may be needed, depending on the value of the contribution. For non-cash donations, donors must consider additional factors, such as the holding period for appreciated assets and the need for a qualified appraisal to determine the fair market value of the donated property. Before donating to a charity, donors should research the organization's mission, goals, and impact to ensure their donations align with their philanthropic objectives. Donors should review a charity's financial statements to assess its financial health and efficiency. This helps determine how effectively the organization uses its resources to achieve its mission. To claim tax deductions for charitable contributions, donors must confirm that the recipient organization is a qualified tax-exempt entity. This can be done by checking the IRS's Tax Exempt Organization Search tool. There are several charity rating agencies, such as Charity Navigator, GuideStar, and BBB Wise Giving Alliance, that provide comprehensive evaluations of non-profit organizations to help donors make informed decisions. Including charitable bequests in estate planning enables donors to leave a lasting legacy by donating a portion of their estate to charity. Incorporating charitable giving into estate planning can provide significant tax benefits by reducing estate taxes and ensuring that assets are utilized according to the donor's philanthropic goals. To maximize the benefits of tax-efficient charitable giving, it is essential to work closely with financial advisors and estate planners. They can help design and implement strategies tailored to the donor's specific financial and philanthropic objectives. Tax-efficient charitable giving is a strategy that helps donors maximize the impact of their donations while minimizing their tax liabilities. Cash donations, appreciated securities, real estate, tangible personal property, and charitable bequests are common types of charitable contributions. Donor-advised funds, charitable remainder trusts, charitable lead trusts, and private foundations are some tax-efficient giving strategies. The IRS provides guidelines on charitable deductions, and donors must maintain proper records of their charitable contributions to claim deductions. Donors should research the recipient organization's mission, impact, financial statements, and tax-exempt status to make informed decisions. Charitable bequests can also be included in estate planning to leave a lasting philanthropic legacy. In conclusion, tax-efficient charitable giving can provide significant benefits for both donors and non-profit organizations. By incorporating tax-efficient giving strategies into personal financial planning, individuals can maximize the impact of their donations while optimizing their financial health and estate plans. It is important to research and evaluate non-profit organizations to ensure that donations align with philanthropic goals and have a meaningful impact. With tax rules and regulations constantly evolving, it is crucial to stay up-to-date and seek professional advice when necessary.Tax-Efficient Charitable Giving: Definition

Benefits of Tax-Efficient Charitable Giving

Maximizing the Impact of Donations

Reducing Tax Liability

Enhancing Personal Financial Planning

Types of Charitable Contributions

Cash Donations

Appreciated Securities

Real Estate

Tangible Personal Property

Charitable Bequests

Tax-Efficient Giving Strategies

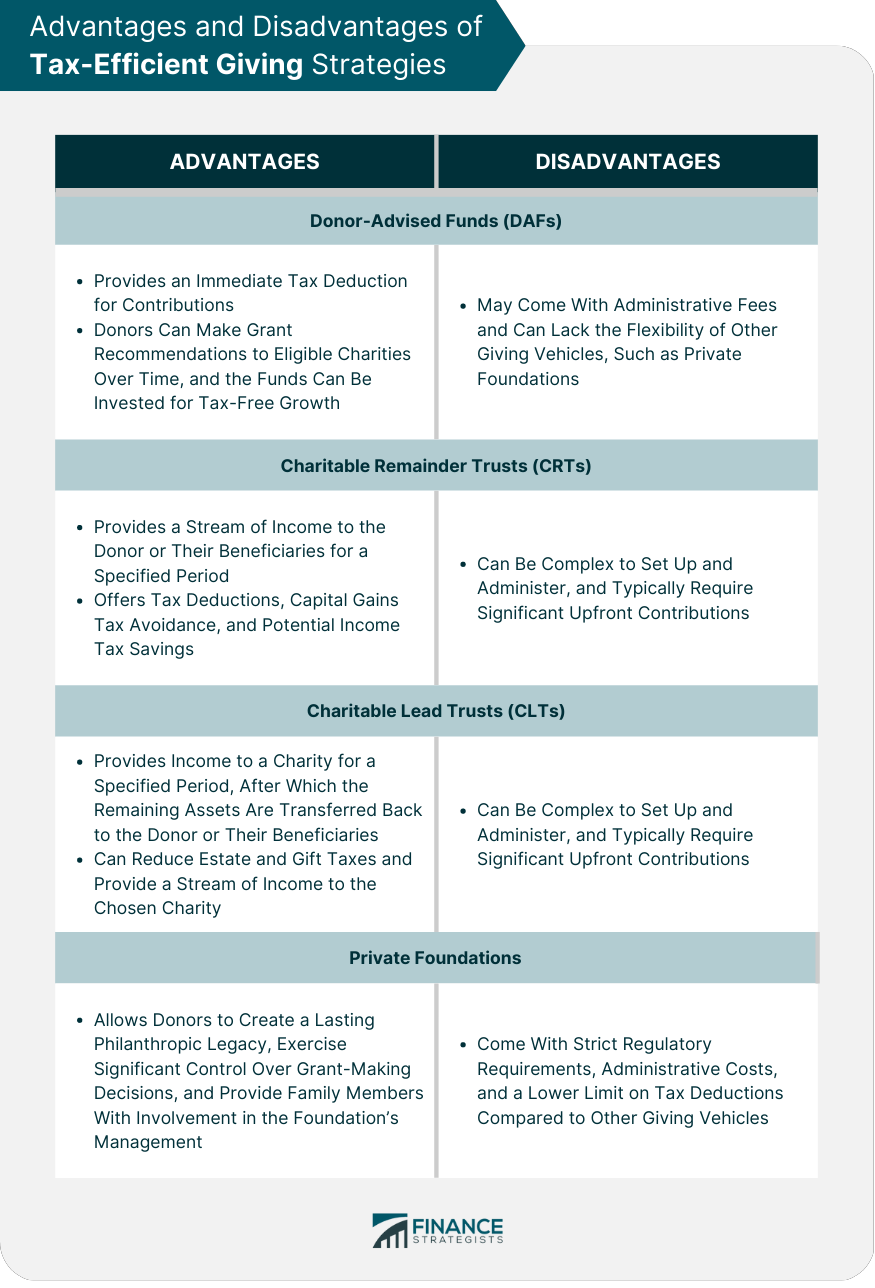

Donor-Advised Funds (DAFs)

Advantages

Disadvantages

Charitable Remainder Trusts (CRTs)

Advantages

Disadvantages

Charitable Lead Trusts (CLTs)

Advantages

Disadvantages

Private Foundations

Advantages

Disadvantages

Tax Rules and Regulations

IRS Guidelines on Charitable Deductions

Deduction Limits Based on Income

Recordkeeping Requirements

Special Considerations for Non-cash Donations

Evaluating and Selecting Charities

Researching the Organization's Mission and Impact

Reviewing Financial Statements and Efficiency

Confirming Tax-Exempt Status

Utilizing Charity Rating Agencies

Incorporating Tax-Efficient Giving Into Estate Planning

Charitable Bequests

Benefits of Including Charitable Giving in Estate Planning

Coordinating With Financial Advisors and Estate Planners

Conclusion

Tax-Efficient Charitable Giving FAQs

Tax-efficient charitable giving refers to donating to a charitable cause in a way that minimizes your tax liability. It involves using tax deductions and credits to maximize the impact of your charitable donations.

There are several tax-efficient ways to donate to charity, including donating appreciated assets, setting up a donor-advised fund, and making qualified charitable distributions from your IRA. These methods can help you reduce your taxes while still supporting a cause you care about.

Donating appreciated assets, such as stocks or mutual funds, can be a tax-efficient way to give to charity. By donating these assets directly to a charitable organization, you can avoid capital gains taxes and receive a tax deduction for the full market value of the asset.

A donor-advised fund is a charitable giving account that allows you to make a charitable contribution and receive an immediate tax deduction, while retaining the ability to recommend grants to your favorite charities over time. By contributing appreciated assets to a donor-advised fund, you can maximize your tax benefits while supporting charitable causes.

Yes, tax-efficient charitable giving can benefit both you and the charity you support. By using tax-efficient strategies to donate to charity, you can reduce your tax liability and potentially increase the size of your donation, while the charity receives much-needed support for their mission. It's a win-win situation for everyone involved.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.