Off-The-Run Treasuries are U.S. government bonds that are not part of the most recent issuance of a given maturity. They include all previously issued bonds, which tend to be less liquid and traded less frequently than the newest, or "on-the-run," treasuries. These bonds offer a slightly higher yield as compensation for their reduced liquidity. Off-The-Run Treasuries serve a crucial purpose in the financial market as they provide an additional investment opportunity and play a role in setting the overall yield curve. The impact of Off-The-Run Treasuries lies in their potential as investment vehicles. These can offer a higher yield, potentially leading to greater returns compared to on-the-run treasuries. Understanding these bonds helps investors make informed decisions about risk, liquidity, and potential returns. These are short-term securities with maturities ranging from a few days to 52 weeks. They are sold at a discount from their face value, and upon maturity, the government pays the full face value. Treasury notes have a longer maturity than bills, typically 2, 3, 5, 7, or 10 years. They pay interest every six months until maturity, at which point the face value is also paid to the investor. These are long-term investments with maturities ranging from 20 to 30 years. Like notes, bonds pay interest semi-annually, and the face value is returned at maturity. TIPS are securities that offer protection against inflation. Their principal is adjusted based on changes in the Consumer Price Index, ensuring that investors' purchasing power remains constant over time. FRNs are a relatively new addition to the U.S. Treasury’s roster, first issued in 2014. They have a maturity of two years and a variable interest rate that is reset daily. When the U.S. Treasury issues a new Treasury bill, note, or bond of a particular maturity, this security becomes an on-the-run issue. Once a newer issue for the same maturity is released, the former on-the-run security becomes off-the-run security. Off-the-run Treasuries are traded Over-The-Counter (OTC), primarily through dealers and brokers. Major players include banks, hedge funds, pension funds, insurance companies, and individual investors. The liquidity of off-the-run Treasuries is less than their on-the-run counterparts, resulting in a wider bid-ask spread. This spread is the difference between what a dealer is willing to pay for a security (bid) and the price they are willing to sell it (ask). Off-the-run Treasuries are often used in portfolio management to provide diversification and a degree of safety due to their lower volatility. They offer a stable, albeit smaller, return compared to riskier assets like equities. Yield curve is constructed using both on-the-run and off-the-run Treasuries. Because off-the-run Treasuries typically offer a higher yield due to their lower liquidity, they contribute to the overall shape of the yield curve. For institutional investors, such as pension funds and insurance companies, off-the-run Treasuries can provide a stable source of income. Their long maturities match well with these institutions' long-term liabilities. Interest rate risk is inherent in all fixed-income securities. When interest rates rise, bond prices fall, and vice versa. This risk is particularly relevant for off-the-run Treasuries due to their longer maturities. Off-the-run Treasuries also carry market liquidity risk. Since they are less frequently traded than on-the-run Treasuries, they may be more difficult to sell without impacting their price. While generally considered risk-free, Treasuries do carry a slight credit risk. This is the risk that the U.S. government will default on its debt, an event considered highly unlikely. The yield on off-the-run Treasuries is calculated in the same way as other fixed-income securities by dividing the annual interest payment by the current market price. However, because these securities are older and less liquid, their yield is typically higher than on-the-run Treasuries. The yield curve, which plots the yield of Treasuries against their maturity, typically shows higher yields for off-the-run Treasuries. This is due to the liquidity premium that investors demand for holding these less liquid securities. The yield spread between off-the-run and on-the-run Treasuries is often used as a measure of market liquidity. A larger spread indicates lower liquidity and higher perceived risk. The Federal Reserve’s monetary policy directly influences Treasury yields through its open market operations. When the Fed buys Treasuries, it increases their price and lowers their yield, and vice versa. Quantitative Easing (QE), an unconventional monetary policy where the central bank purchases long-term securities from the open market, has been used to lower long-term interest rates. This can increase the price and decrease the yield of off-the-run Treasuries. Changes in the Federal Funds rate, the short-term interest rate targeted by the Fed, can impact the yield of off-the-run Treasuries. When the Fed raises rates, yields on these Treasuries may increase. Over the past several decades, the market for off-the-run Treasuries has grown significantly, reflecting the overall expansion of the U.S. government's debt. Technological advancements have transformed the trading of off-the-run Treasuries. Electronic trading platforms have increased market transparency and reduced transaction costs, making these securities more accessible to individual investors. The future of off-the-run Treasuries depends on various factors, including fiscal policy, monetary policy, and global economic conditions. One potential challenge is the increasing supply of U.S. government debt, which could pressure yields higher. Off-The-Run Treasuries, encompassing a variety of securities such as Treasury Bills, Notes, Bonds, TIPS, and FRNs, present a valuable facet of investment strategies and yield curve formation. Created when newer Treasury issues of the same maturity emerge, they typically offer higher yields due to reduced liquidity. Traded over-the-counter, these bonds play a crucial role in portfolio management and serve as a stable income source for institutional investors. However, they carry associated risks, including interest rates, market liquidity, and minimal credit risk. Their yield is a crucial aspect, playing a part in yield curve implications and indicating market liquidity. Monetary policy also influences these securities, with actions like Quantitative Easing impacting their yield. Technological advancements have broadened access to these securities, transforming their trading landscape. The future of Off-The-Run Treasuries will depend on various factors, with the expanding U.S. debt supply posing potential challenges.What Are Off-The-Run Treasuries?

Types of Off-The-Run Treasuries

Treasury Bills

Treasury Notes

Treasury Bonds

Treasury Inflation-Protected Securities (TIPS)

Floating Rate Notes (FRNs)

Creation and Trading of Off-The-Run Treasuries

How Treasuries Become Off-The-Run

Trading Platforms and Players in the Market

The Bid-Ask Spread and Liquidity of Off-The-Run Treasuries

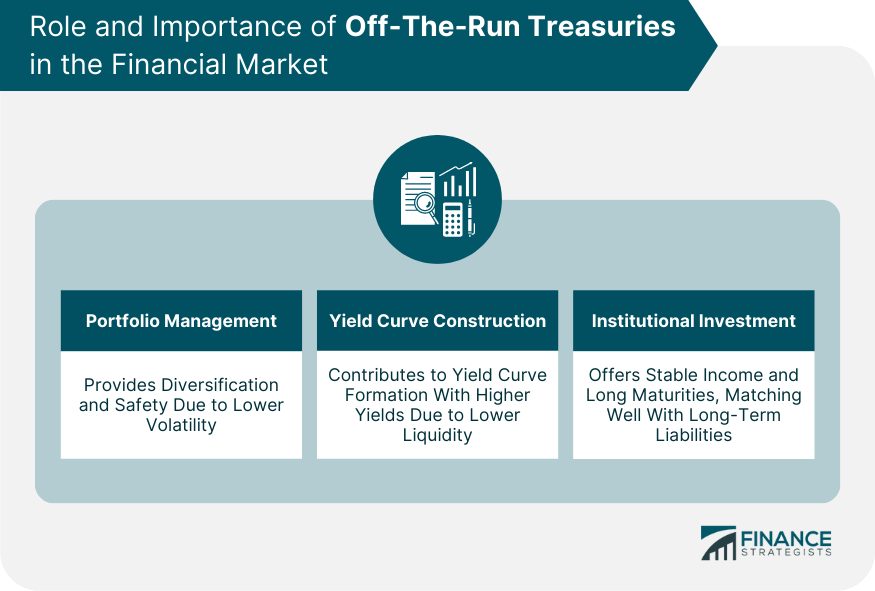

Role and Importance of Off-The-Run Treasuries in the Financial Market

Function in Portfolio Management

Role in Yield Curve Construction

Importance for Institutional Investors

Risks Associated With Off-The-Run Treasuries

Interest Rate Risk

Market Liquidity Risk

Credit Risk

Yield of Off-The-Run Treasuries

Yield Calculation

Yield Curve Implications

Yield Spread Between Off-The-Run and On-The-Run Treasuries

Impact of Monetary Policy on Off-The-Run Treasuries

Influence of Federal Reserve Operations

Effects of Quantitative Easing

Reaction to Changes in Interest Rates

Recent Trends and Future of Off-The-Run Treasuries

Evolution of the Market Over Time

Technological Advancements and Their Impacts

Future Prospects and Challenges for Off-The-Run Treasuries

Bottom Line

Off-The-Run Treasuries FAQs

Off-The-Run Treasuries are U.S. government bonds that are not part of the most recent issuance of a given maturity. They are all previously issued bonds, which tend to be less liquid and traded less frequently than the newest, or "on-the-run," Treasuries. These bonds offer a slightly higher yield due to their reduced liquidity.

When the U.S. Treasury issues a new Treasury bill, note, or bond of a particular maturity, it becomes an on-the-run issue. Once a newer issue for the same maturity is released, the former on-the-run security becomes off-the-run. These Treasuries are primarily traded over-the-counter, through dealers and brokers.

Off-The-Run Treasuries play a crucial role in providing an additional investment opportunity and contribute to the overall yield curve. They are often used in portfolio management to provide diversification and safety due to their lower volatility. Institutional investors, like pension funds and insurance companies, provide a stable source of income and match well with their long-term liabilities.

Off-The-Run Treasuries are associated with interest rate risk, market liquidity risk, and credit risk. Interest rate risk is due to fluctuations in rates affecting bond prices, while liquidity risk relates to the difficulty of selling these less frequently traded securities without impacting their price. Credit risk, although minimal, is the risk that the U.S. government will default on its debt.

Monetary policy, particularly the operations of the Federal Reserve, directly influences the yield of Off-The-Run Treasuries. For instance, when the Fed buys Treasuries, it increases their price and lowers their yield. Conversely, when it sells, the price drops, and the yield rises. Additionally, unconventional monetary policies like Quantitative Easing can decrease the yield of these Treasuries.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.