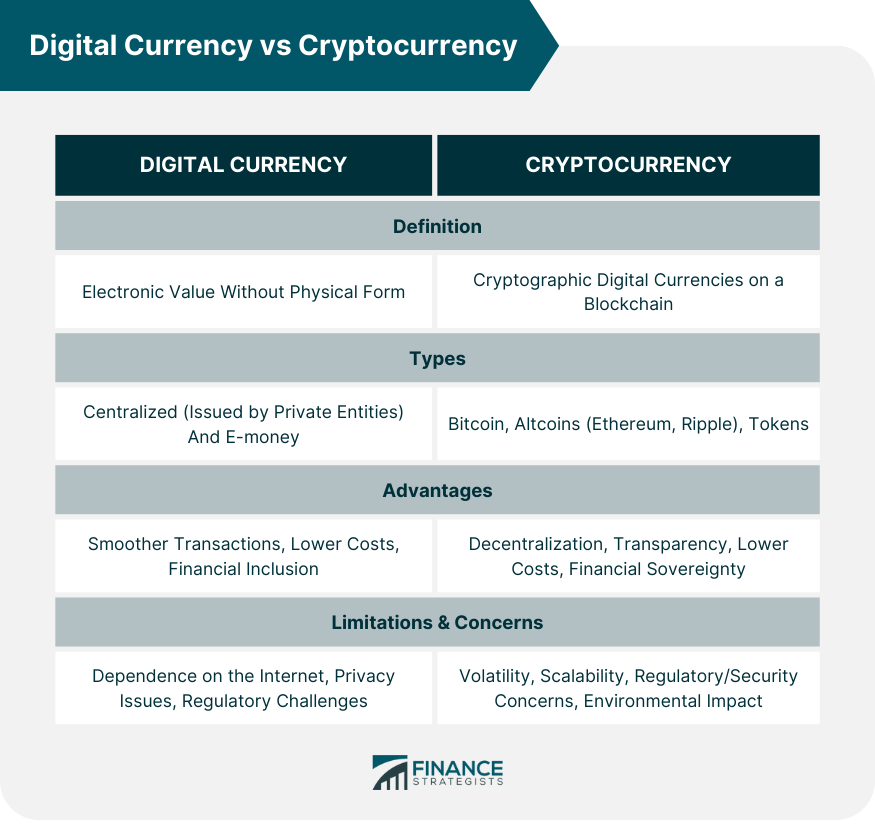

Digital currency is a broad term that encompasses all forms of money in digital format. It simplifies online transactions by eliminating the need for physical cash and can be either centralized (like e-money issued by banks) or decentralized. Cryptocurrency, a subset of digital currency, introduces a revolutionary framework, utilizing cryptographic principles for transaction security and typically operating on a decentralized system called a blockchain. While all cryptocurrencies are digital currencies, not all digital currencies are cryptocurrencies. The primary distinction lies in their structure and management: digital currencies are often overseen by centralized institutions, whereas cryptocurrencies operate on distributed networks, removing the need for intermediaries. As the world shifts towards a more digital financial landscape, understanding the nuances between digital currency and cryptocurrency becomes pivotal for users, investors, and regulators alike. Most digital currencies operate under a centralized system governed by a specific entity or organization. This centralization often leads to streamlined processes and controlled monetary policies. In contrast, cryptocurrencies function on a decentralized model, relying on distributed networks. This ensures that no single institution or authority holds power, promoting a democratized control of resources and transactions. Decentralization can also result in diverse validation processes, contributing to the robustness of the network. Digital currencies typically operate within the boundaries of existing regulatory frameworks since they often mirror traditional financial models. Governments and financial institutions can exert control over them. On the other hand, cryptocurrencies, with their revolutionary approaches, push boundaries, leading to debates and new regulatory challenges. Given their decentralized nature, regulating cryptocurrencies becomes a complex task, with many nations still exploring appropriate legislative measures. Centralized digital currencies may entail the collection and storage of user data, making transactions traceable. This could be advantageous for authorities monitoring financial activities but raises privacy concerns for users. In contrast, cryptocurrencies, particularly Bitcoin, prioritize user anonymity. While transactions are recorded on the blockchain, personal identities are often concealed. However, it's essential to note that complete anonymity isn't always guaranteed, especially with advanced tracing tools becoming available. The backbone of digital currencies usually lies in centralized databases maintained by the issuing authority or organization. These databases manage balances, transactions, and other vital data. Cryptocurrencies, conversely, operate on blockchain technology—a decentralized ledger that records transactions across numerous nodes. This distributed nature ensures redundancy, preventing data loss and bolstering security against centralized system failures. Both digital currencies and cryptocurrencies face security threats, but the nature of these threats can differ significantly. For digital currencies, concerns might revolve around centralized system breaches, database vulnerabilities, or authority malfeasance. Cryptocurrencies, with their reliance on complex cryptographic principles and decentralized architectures, encounter challenges like potential vulnerabilities in smart contracts, risks associated with wallet security, and the ever-evolving landscape of cyber threats targeting decentralized networks. Digital currency can be best described as a monetary value that's exclusively in electronic form. It doesn't possess a physical counterpart like coins or banknotes, making it distinct from conventional tangible currencies. Instead of relying on tangible elements, digital currencies hinge on electronic representations of value. This electronic nature stems from advanced technologies and cryptographic principles to ensure that these representations are secure, valid, and unique, preventing duplication or counterfeiting. Centralized Digital Currencies: Unlike traditional currencies issued by governments, centralized digital currencies are often issued by private entities or organizations. Electronic Money (E-money): E-money, or electronic money, signifies electronic storage of monetary value on a technical device. Ease of Transactions: Digital currencies facilitate smoother transactions. There’s no need for physical exchanges; a simple click ensures the transfer of value, making it ideal for online commerce. Lower Transaction Costs: Bypassing traditional banking systems or intermediaries often means lower fees. Digital currency transactions can be more cost-effective than their conventional counterparts. Increased Accessibility: For those without access to traditional banking systems, digital currencies offer an alternative. It paves the way for financial inclusion in underbanked regions. Dependence on Internet Infrastructure: A significant drawback is the reliance on Internet connectivity. Without it, the functionality of digital currencies becomes moot." Privacy Concerns: In centralized digital currencies, there's potential for user data to be stored and possibly misused. This central repository becomes a concern for privacy advocates. Regulatory Issues: The rise of digital currencies has caught the attention of regulators worldwide. Their decentralized nature poses challenges in terms of taxation, monetary policy, and potential misuse. Cryptocurrencies are a subset of digital currencies that use cryptographic techniques for secure transactions. They operate on decentralized platforms, typically on a technology called the blockchain. Blockchain technology underpins most cryptocurrencies. It’s a distributed ledger that records all transactions across numerous computers. Its design ensures data integrity, security, and decentralization. Bitcoin: Introduced in 2009, Bitcoin is the pioneer and remains the most well-known cryptocurrency. Its decentralized nature, capped supply, and robust security make it a digital gold counterpart. Altcoins: These are alternatives to Bitcoin. Notable examples include Ethereum, which offers smart contract functionality, and Ripple, known for its digital payment protocol more than its cryptocurrency. Tokens: Represent assets or utility and reside on existing blockchains. ERC-20 tokens, for instance, are built on the Ethereum platform and have become increasingly popular for crowdfunding projects. Decentralization: Cryptocurrencies operate without a central authority, ensuring no single entity has control, thereby reducing risks of censorship or central point of failure. Transparency and Immutability: Transactions on the blockchain are transparent and immutable. Once recorded, they can't be altered, ensuring transparency in transactions. Potentially Lower Transaction Costs: Much like digital currencies, cryptocurrencies can bypass traditional financial intermediaries, often leading to reduced costs. Financial Sovereignty: Cryptocurrencies offer individuals full control over their money without interference or oversight from banks or governments. Volatility: Cryptocurrency prices can be highly volatile, driven by factors ranging from regulatory news to market speculations. Scalability Issues: Popular cryptocurrencies face challenges in scaling up and processing large numbers of transactions quickly. Regulatory and Security Concerns: As decentralized entities, cryptocurrencies face scrutiny from regulators. Additionally, the ecosystem has seen its share of security breaches. Environmental Concerns: Some cryptocurrencies, like Bitcoin, require significant computational work, leading to concerns about energy consumption and environmental impact. Digital and cryptocurrencies are poised to reshape the landscape of global remittances. They promise faster transaction times, often bypassing the lengthy processes associated with conventional banking systems. This speed is crucial for migrant workers and families dependent on timely funds. With the escalating popularity of digital and cryptocurrencies, traditional banking institutions face an imperative to evolve. This could mean integrating blockchain technologies into their systems or exploring the creation of their own digital currencies to remain relevant and competitive. A significant portion of the global population remains unbanked or underbanked, lacking access to essential financial services. Digital and cryptocurrencies can address this gap, providing these individuals with platforms to save, invest, and transact, all without the need for traditional banking infrastructure. • How Different Countries Approach Digital Currency and Cryptocurrency: Nations vary in their approach. Some embrace the technology, while others impose bans or strict regulations, reflecting diverse economic, political, and cultural contexts. • Regulatory Challenges and Solutions: Balancing innovation with consumer protection, fraud prevention, and financial stability is a global challenge. Collaborative international approaches may pave the way forward. • Concerns for Anti-Money Laundering (AML) and Combating the Financing of Terrorism (CFT): Both digital and cryptocurrencies face concerns over the potential misuse of illicit activities. Rigorous AML and CFT procedures can mitigate these risks. The evolving financial landscape is being significantly influenced by the rise of digital currencies and cryptocurrencies. While both offer electronic versions of money, digital currencies can be centralized and overseen by institutions, whereas cryptocurrencies operate on decentralized systems, often using blockchain technology. This decentralization offers heightened security, transparency, and democratized control of transactions. As these innovations gain momentum, they present opportunities for faster global remittances, challenge conventional banking paradigms, and promise broader financial inclusion. However, with these advancements come challenges, especially in the realm of regulation. Different nations grapple with integrating these technologies into their financial and regulatory infrastructures, balancing innovation with concerns about stability, fraud, and illicit activities. Moreover, the environmental implications of some cryptocurrencies necessitate a broader debate on sustainable practices. As the line between traditional and digital finance continues to blur, understanding the intricacies of these innovations becomes essential for all stakeholdersOverview of Digital Currency vs Cryptocurrency

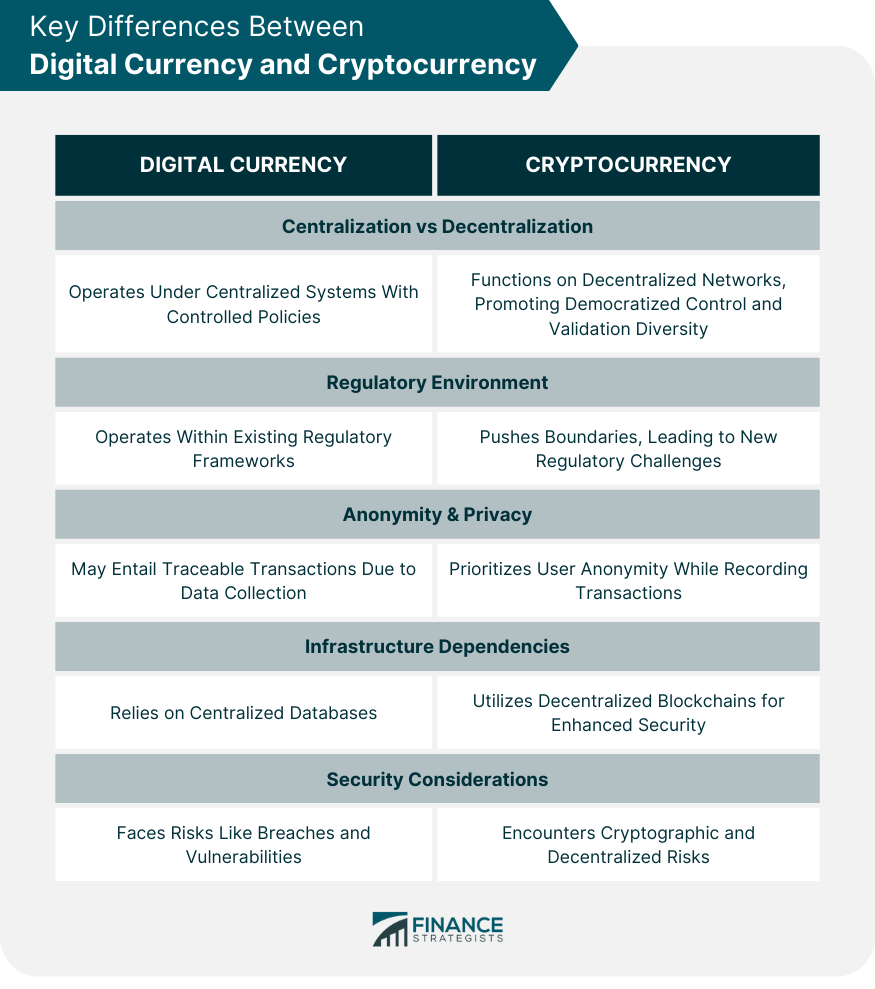

Key Differences Between Digital Currency and Cryptocurrency

Centralization vs Decentralization

Regulatory Environment

Anonymity & Privacy

Infrastructure Dependencies

Security Considerations

What Is Digital Currency?

Types of Digital Currencies

They operate within an internal system, with a central authority overseeing and regulating the transactions.

This can be widely used for transactions, both online and offline, with accepting parties. Popular examples include prepaid cards or mobile money.Advantages of Digital Currencies

Limitations & Concerns

What Is Cryptocurrency?

Types of Cryptocurrencies

Advantages of Cryptocurrencies

Limitations & Concerns

Economic Implications of Digital Currency and Cryptocurrency

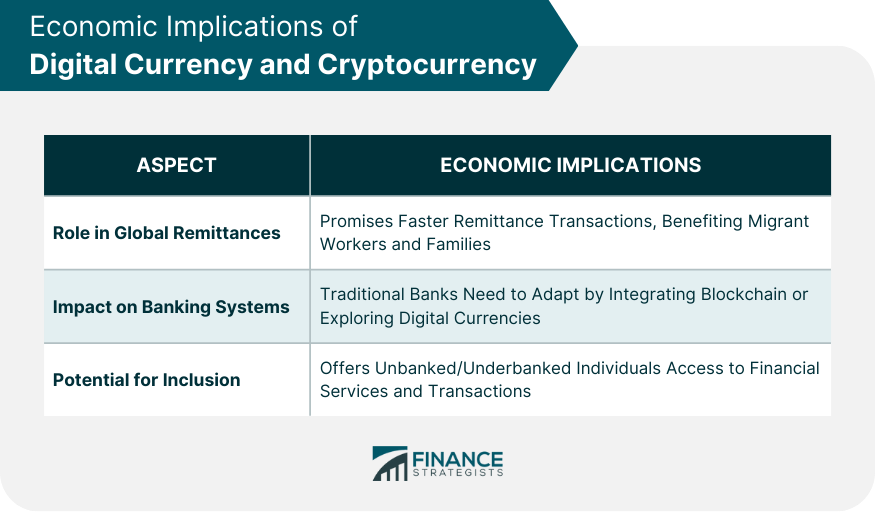

Role in Global Remittances

Impact on Traditional Banking Systems

Potential for Financial Inclusion

Regulatory and Legal Perspectives of Digital Currency and Cryptocurrency

Conclusion

Digital Currency vs Cryptocurrency FAQs

Digital currencies are electronic versions of traditional money, which can be centralized and regulated by institutions. Cryptocurrencies, on the other hand, are a subset of digital currencies that operate on decentralized platforms, often using blockchain technology and cryptographic principles for added security.

Cryptocurrencies primarily use blockchain technology, which is a decentralized and distributed ledger system. It ensures transparent, secure, and immutable transactions, which are key characteristics that set cryptocurrencies apart from many other forms of digital currency.

They offer potential solutions for quicker, more affordable global remittances, challenge traditional banking systems, and provide opportunities for financial inclusion, especially in areas underserved by conventional financial services.

Approaches vary widely. Some countries embrace these technologies by establishing clear frameworks or even launching their own digital currencies. Others take a cautious approach by imposing strict regulations or outright bans, often due to concerns about economic stability, fraud, or illicit activities.

Certain cryptocurrencies, like Bitcoin, require energy-intensive computational work known as proof-of-work for their operation. This leads to significant energy consumption and, consequently, environmental concerns, especially when non-renewable energy sources are used.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.