An abnormal return is the excess return that an investment or a portfolio generates over a predicted rate of return. This predicted rate, or expected return, could be based on a benchmark index like the S&P 500 or an asset pricing model such as the Capital Asset Pricing Model (CAPM). Abnormal return is crucial as it provides insights into how an investment performs relative to overall market conditions or its expected performance. Abnormal return plays a pivotal role in financial analysis as it allows investors, financial analysts, and portfolio managers to evaluate the performance of an investment or a portfolio beyond what was anticipated. It helps to identify investments that have outperformed or underperformed their expected returns, thus serving as a key tool in investment decision-making and risk management. The formula for calculating abnormal return is quite straightforward: The actual return is the return that the investment or portfolio has actually generated, while the expected return is the return that was anticipated based on the market performance or an asset pricing model. In calculating the abnormal return, several variables can influence the expected return. These may include the risk-free rate (often based on government bond yields), the beta of the investment (which measures its volatility relative to the market), and the expected market return. Adjustments can also be made to account for factors such as risk, size, and value. A positive abnormal return, as in the example above, suggests that the investment or portfolio has outperformed its expected return. This could be due to a variety of factors, such as strong company performance, positive market sentiment, or successful investment strategies. A negative abnormal return, on the other hand, indicates underperformance. This means the investment or portfolio has returned less than what was anticipated. Reasons for a negative abnormal return can include poor company performance, adverse market conditions, or failed investment strategies. A zero abnormal return suggests that the investment or portfolio performed exactly as expected, with the actual return matching the expected return. This scenario, while possible, is relatively rare given the volatility and unpredictability of financial markets. Abnormal returns can be influenced by a variety of market factors. These can include overall market performance, economic indicators, interest rates, and investor sentiment. For example, during a bull market, many securities may generate positive abnormal returns due to the generally favorable market conditions. Conversely, during a bear market, negative abnormal returns may be more common. Company-specific factors can also significantly impact abnormal returns. These can include earnings reports, product launches, management changes, mergers and acquisitions, and other company news. For instance, a company that reports better-than-expected earnings might see positive abnormal returns as investors react to the news. In today's interconnected global economy, international events and economic conditions can also influence abnormal returns. For example, geopolitical tensions, changes in foreign policy, or economic crises in other countries can affect global financial markets and, consequently, the abnormal returns of investments. In active trading, traders often seek to generate positive abnormal returns by exploiting market inefficiencies. This could involve using complex algorithms to identify mispriced securities, timing the market based on economic indicators, or trading based on news events. However, achieving consistent abnormal returns through active trading can be challenging and risky due to market volatility and the potential for losses. In portfolio management, abnormal return is a key metric for evaluating the performance of portfolio managers. A manager who consistently generates positive abnormal returns is seen as adding value beyond what could be achieved by passively investing in the market. Nonetheless, it's important to consider risk-adjusted returns, as higher returns may be accompanied by higher risk. Abnormal return is based on the assumption that markets are efficient and that all available information is already incorporated into stock prices. However, markets may not always be perfectly efficient, and investors could face challenges in accurately identifying mispriced securities. The presence of market anomalies and behavioral biases can impact abnormal returns and introduce uncertainties into investment strategies. Calculating abnormal return relies heavily on historical price and return data. The accuracy and quality of this data are crucial for deriving meaningful insights. Data errors or inconsistencies can distort abnormal return calculations and lead to incorrect investment decisions. Investors should exercise caution and ensure they have access to reliable and accurate data sources. The choice of benchmark index or market proxy is an important consideration when calculating abnormal return. Selecting an inappropriate benchmark can result in misleading conclusions about the performance of an investment strategy. It is essential to choose a benchmark that closely aligns with the investment strategy and accurately represents the relevant market segment. Abnormal return calculations are often based on short-term price movements, which can be influenced by market noise and volatility. Short-term fluctuations may not necessarily reflect the underlying value or long-term prospects of an investment. Relying solely on abnormal return without considering longer-term performance and fundamentals can lead to misguided investment decisions. There is a risk of overfitting and data mining bias when using abnormal return in investment strategies. Overfitting occurs when investment strategies are tailored too closely to historical data, resulting in poor performance in new market conditions. Data mining bias refers to the selective use of historical data to support a particular investment strategy, which may not hold up in the future. Investors should be cautious about relying solely on past abnormal returns without considering the robustness and generalizability of the strategy. Abnormal return represents a significant metric within financial analysis and investment decision-making. It is defined as the difference between the actual return of an investment or portfolio and its expected return. This measure enables investors to discern whether an investment has exceeded or fallen short of its anticipated performance. The calculation of abnormal returns involves understanding numerous factors, including market conditions, company-specific elements, and global economic influences. However, it's crucial to remember that past abnormal returns do not guarantee future performance, and the calculation of expected returns is an estimate that can vary based on the model used. As technological advancements continue to refine the precision of abnormal return analysis, these tools should serve as aids, not substitutes, for sound investment decision-making. The principles of comparing actual returns to expected returns as a means to evaluate investment performance remain at the core of financial analysis.What Is an Abnormal Return?

Calculating Abnormal Returns

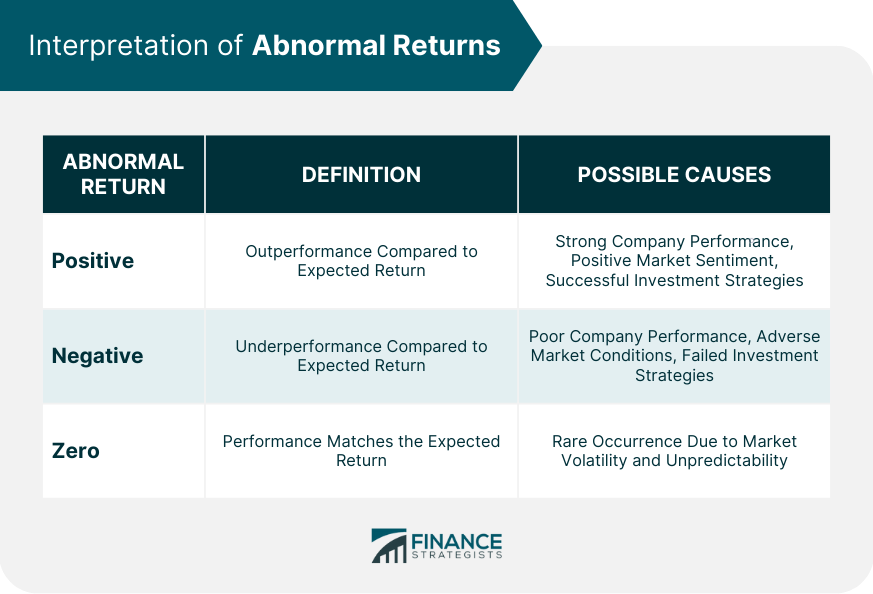

Interpretation of Abnormal Returns

Positive Abnormal Return

Negative Abnormal Return

Zero Abnormal Return

Factors Influencing Abnormal Returns

Market Factors

Company-Specific Factors

Global Economic Factors

Abnormal Return and Investment Strategies

Use of Abnormal Returns in Active Trading

Use of Abnormal Returns in Portfolio Management

Limitations and Risks of Using Abnormal Returns in Investment Strategies

Market Efficiency Assumptions

Data Reliance and Accuracy

Benchmark Selection

Short-Term Volatility and Noise

Overfitting and Data Mining Bias

Final Thoughts

Abnormal Return FAQs

Abnormal return is the difference between the actual return earned on an investment and the expected return on that investment based on the market trends.

To calculate abnormal return, the expected return is estimated using various methods, such as market trends or a specific benchmark. The actual return is then subtracted from the expected return to get the abnormal return.

A positive abnormal return means that the actual return on an investment is higher than the expected return. This can be an indicator that the investment performed better than the market trends or benchmark.

A negative abnormal return means that the actual return on an investment is lower than the expected return. This can be an indicator that the investment performed worse than the market trends or benchmark.

Abnormal returns can be caused by a variety of factors, such as changes in the market, changes in the industry, unexpected news or events, or even company-specific factors like management changes or financial performance.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.