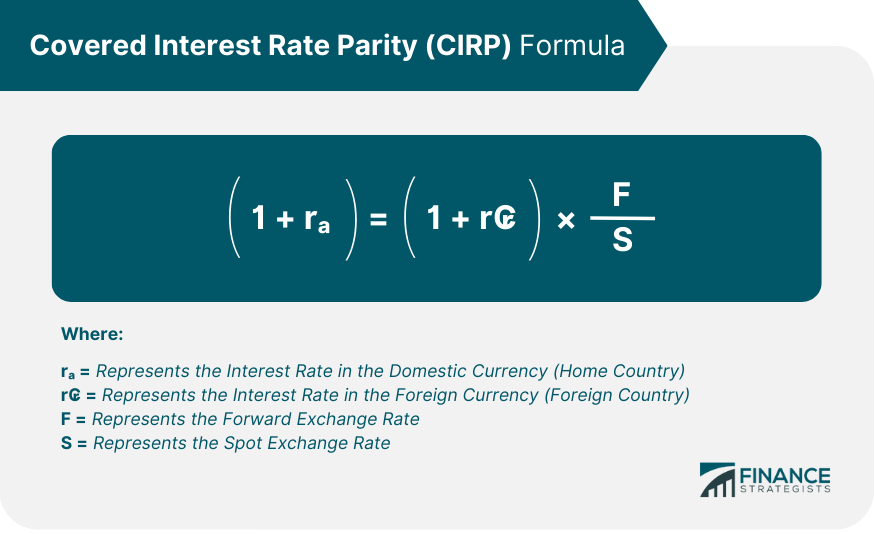

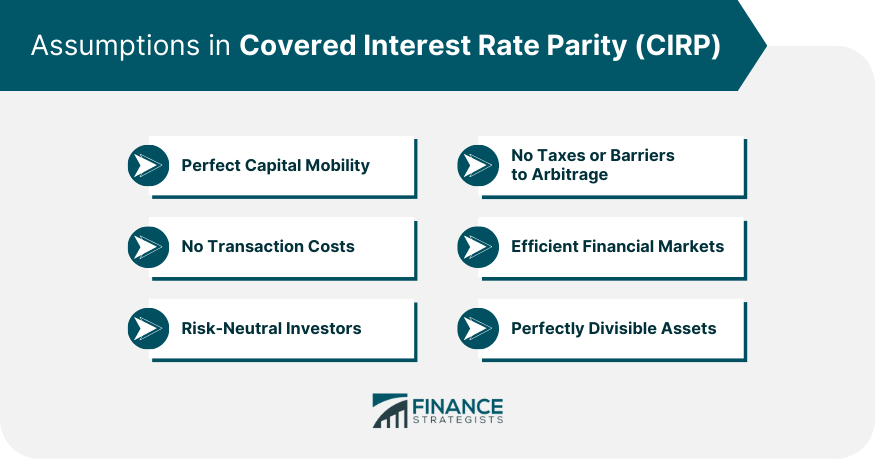

Covered Interest Rate Parity (CIRP) is a fundamental concept in international finance that asserts a direct relationship between forward exchange rates and spot exchange rates, given the interest rates of two countries. It's premised on the notion of no-arbitrage, implying that investors cannot achieve risk-free profits by capitalizing on the discrepancies between the interest rates and exchange rates of two countries. The significance of CIRP is multifaceted. It plays a crucial role in shaping the dynamics of the foreign exchange market, influencing spot and forward exchange rates. Furthermore, it serves as a theoretical benchmark for currency hedging and predicting future exchange rates. The formula for Covered Interest Rate Parity (CIRP) is as follows: Assumptions of Covered Interest Rate Parity (CIRP) include: Perfect Capital Mobility: It assumes that there are no restrictions on capital flows between countries, allowing investors to freely borrow or lend in different currencies. No Transaction Costs: CIRP assumes that there are no transaction costs involved in exchanging currencies or entering into forward contracts. Risk-Neutral Investors: It assumes that investors are risk-neutral, meaning they don't prefer one currency over another based on risk considerations. No Taxes or Barriers to Arbitrage: CIRP assumes the absence of taxes or other barriers that would hinder arbitrage opportunities. Efficient Financial Markets: It assumes that financial markets are efficient, meaning all relevant information is reflected in the exchange rates and interest rates. Perfectly Divisible Assets: CIRP assumes that investors can borrow or lend any amount of money at the prevailing interest rates without limitations on the size of investments. It's important to note that while CIRP is a widely used concept, these assumptions may not hold in the real world, leading to deviations from the parity relationship. Exchange rates, both spot and forward, have a direct bearing on CIRP. The relationship between the spot and forward exchange rates should align with the interest rate differential between the two countries for CIRP to hold. Interest rates are integral to CIRP. The parity condition is based on the comparison of interest rates in two different countries. Any changes in these rates can disrupt parity. CIRP assumes efficient markets, meaning all relevant information is readily available to all market participants, and prices adjust quickly to new information. Inefficient markets can lead to deviations from CIRP. The forward exchange rate, according to CIRP, should reflect the interest rate differential between the two countries. If it doesn't, arbitrage opportunities arise, pushing the rates back into alignment. To calculate the forward rate rates using parity, simply multiply the spot rate by the ratio of interest rates and adjust for the time until expiration. Arbitrage refers to the practice of taking advantage of price discrepancies in different markets to make risk-free profits. CIRP prevents arbitrage by maintaining a balance between interest rates and exchange rates. If there's a deviation from CIRP, arbitrageurs would exploit this discrepancy until the no-arbitrage condition is restored. There have been instances when CIRP didn't hold, leading to arbitrage opportunities. These usually occur during times of financial crises, market inefficiencies, or when there are restrictions on capital mobility. CIRP exerts a significant influence on both spot and forward exchange rates. It ensures that these rates align with the interest rate differential between the two countries. CIRP is fundamental to currency hedging strategies. It helps in determining the forward exchange rate, which is used to hedge against future exchange rate fluctuations. CIRP is also used to predict future exchange rates. By using current spot rates, interest rates, and the CIRP equation, one can calculate forward rates that serve as predictions of future spot rates. While CIRP assumes a frictionless market with no transaction costs, the reality is different. Transaction costs and market frictions can lead to deviations from CIRP, as these costs can inhibit arbitrage activities that would otherwise bring the market back into parity. CIRP also assumes no credit risk and unrestricted capital mobility, which is not always the case. Credit risks and capital controls imposed by countries can disrupt CIRP, providing room for potential arbitrage opportunities. The theory of CIRP is based on the assumption of perfect capital mobility, meaning investors are free to move their capital across borders without restrictions. However, in practice, many countries impose controls on capital movements, which can lead to deviations from CIRP. Covered Interest Rate Parity (CIRP) is a fundamental concept in international finance that establishes a relationship between forward and spot exchange rates based on interest rate differentials. However, CIRP is subject to certain limitations. Transaction costs, market frictions, and credit risk can hinder the effectiveness of arbitrage opportunities, leading to deviations from CIRP. Capital controls imposed by countries can also disrupt the parity relationship. Furthermore, CIRP assumes perfect capital mobility, which may not always hold in the real world. Despite these limitations, CIRP plays a significant role in shaping the dynamics of the foreign exchange market, influencing spot and forward rates. It is crucial for currency hedging strategies and can be used to predict future exchange rates. Understanding the limitations of CIRP is essential for comprehending its practical implications in the complex global financial landscape.Definition of Covered Interest Rate Parity

Formula and Assumptions in Covered Interest Rate Parity (CIRP)

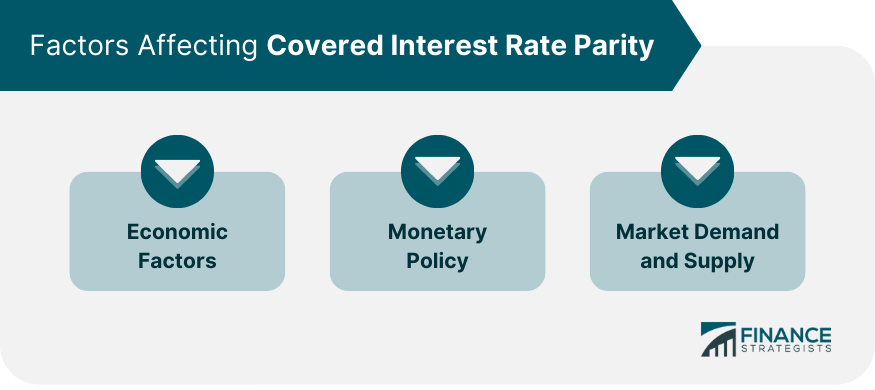

Factors Affecting Covered Interest Rate Parity

Exchange Rates

Interest Rates

Market Efficiency

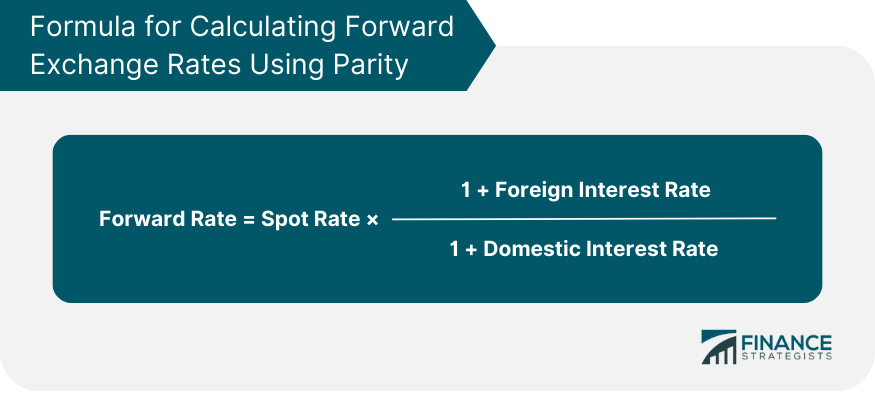

Covered Interest Rate Parity and Forward Exchange Rates

Relationship Between Parity and Forward Rates

Calculating Forward Exchange Rates Using Parity

Covered Interest Rate Parity and Arbitrage Opportunities

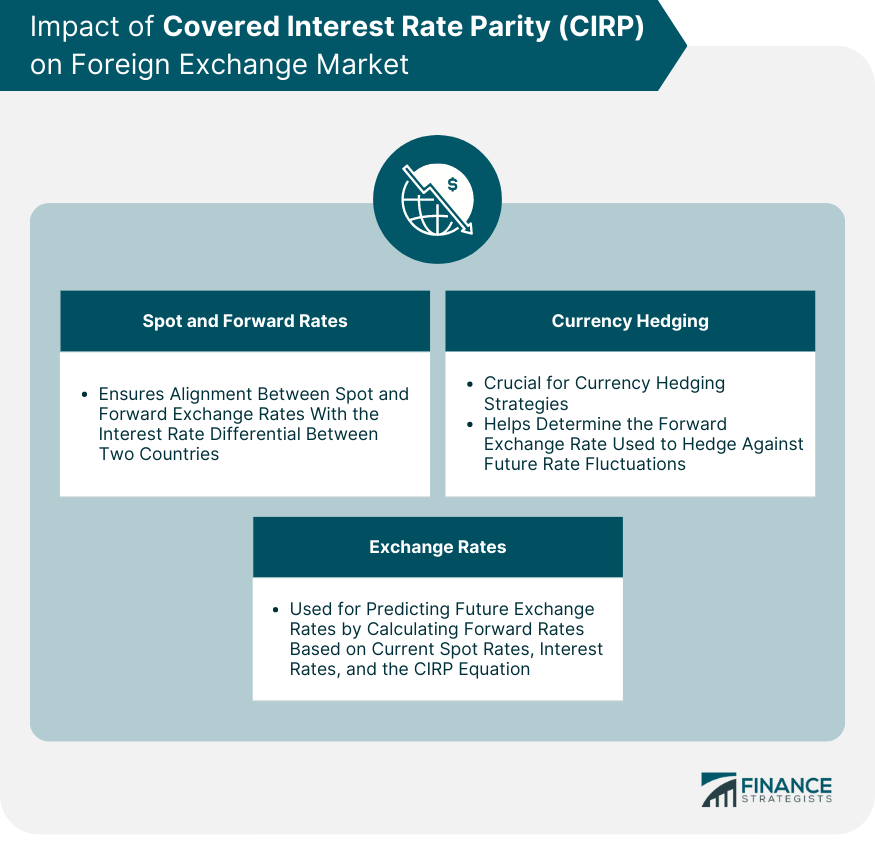

Impact of Covered Interest Rate Parity on Foreign Exchange Market

Influence on Spot and Forward Rates

Effects on Currency Hedging

Role in Predicting Future Exchange Rates

Limitations of Covered Interest Rate Parity

Market Frictions and Transaction Costs

Credit Risk and Capital Controls

Perfect Capital Mobility

Conclusion

Covered Interest Rate Parity (CIRP) FAQs

Covered Interest Rate Parity (CIRP) is a financial concept that states the relationship between forward and spot exchange rates should align with the interest rate differential between two countries to prevent risk-free arbitrage opportunities.

CIRP influences the foreign exchange market by determining the relationship between spot and forward exchange rates. It also plays a significant role in currency hedging strategies and predicting future exchange rates.

Key factors affecting CIRP include exchange rates, interest rates, and market efficiency. Changes in any of these can lead to deviations from CIRP, potentially creating arbitrage opportunities.

While CIRP assumes a frictionless market with no transaction costs or credit risk and perfect capital mobility, the reality is often different. Factors like transaction costs, credit risk, capital controls, and market frictions can lead to deviations from CIRP.

CIRP maintains a balance between interest rates and exchange rates, preventing risk-free arbitrage opportunities. If there's a deviation from CIRP, arbitrageurs would exploit this discrepancy until the no-arbitrage condition is restored.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.