Investment risk refers to the possibility that an investment's actual return will be different from its expected return. It is the potential for losses or lower returns on an investment due to various factors, such as changes in market conditions, economic downturns, or other unforeseen events. Investment risk can be divided into two categories, systematic and unsystematic, and investors should consider both types of risk when making investment decisions and assess their risk tolerance accordingly. Higher-risk investments have the potential for higher returns, but they also carry a greater risk of loss. Conversely, lower-risk investments may offer lower returns but are less likely to result in significant losses. Systematic Risk: Systematic risk refers to the risk inherent in the entire market or market segment. This type of risk cannot be eliminated through diversification as it affects all investments in the market. Examples include interest rate risk, inflation risk, and economic risk. Unsystematic Risk: Unsystematic risk is specific to a particular company, industry, or security. This type of risk can be reduced or eliminated through diversification. Examples include business risk, credit risk, and liquidity risk. The risk-return trade-off is the principle that higher risk investments generally have the potential for higher returns, while lower risk investments have lower potential returns. Investors need to balance their risk tolerance with their desired investment returns. Diversification is the process of spreading investments across various asset classes, industries, and geographies to reduce overall portfolio risk. By investing in a diverse set of assets, investors can limit the impact of any single investment on their overall portfolio performance. Active and passive risks are two distinct approaches to investment management. Understanding the differences and implications for investors is vital for successful portfolio management. Active Risk: Active risk is the risk associated with an investment manager's decisions to deviate from a benchmark index. Active management aims to outperform the benchmark through active security selection and market timing. Passive Risk: Passive risk, on the other hand, is the risk associated with mirroring the performance of a benchmark index. Passive management seeks to replicate the index's performance by holding the same securities in the same proportions as the index. Active risk management involves taking on additional risk in pursuit of outperformance, while passive risk management focuses on minimizing tracking error and achieving benchmark-like returns. Investors must choose the approach that best aligns with their investment objectives and risk tolerance. Active risk can result in higher potential returns compared to passive risk but may also lead to higher management fees, more significant tracking errors, and potentially greater losses if the active manager underperforms. Measuring active risk is essential for evaluating investment managers and understanding the risk associated with their investment decisions. Definition and Calculation: Tracking error measures the difference between a portfolio's returns and its benchmark index's returns. It is calculated as the standard deviation of the difference between the portfolio and benchmark returns. Interpretation and Significance: A higher tracking error indicates greater deviation from the benchmark index, signaling higher active risk. Conversely, a lower tracking error reflects a closer alignment with the benchmark and lower active risk. Definition and Calculation: Active share measures the degree to which a portfolio's holdings differ from those of its benchmark index. It is calculated as the sum of the absolute differences between the portfolio and benchmark weights divided by two. Interpretation and Significance: A higher active share indicates a more significant deviation from the benchmark index and greater active risk. Conversely, a lower active share reflects a closer alignment with the benchmark and lower active risk. Definition and Calculation: The information ratio measures the risk-adjusted return of a portfolio relative to its benchmark index. It is calculated as the portfolio's excess return (the difference between the portfolio and benchmark returns) divided by the tracking error. Interpretation and Significance: A higher information ratio indicates a portfolio has generated better risk-adjusted returns relative to its benchmark. Conversely, a lower information ratio reflects poorer risk-adjusted performance compared to the benchmark. Various factors can influence the level of active risk in a portfolio, including investment strategy, market conditions, and portfolio characteristics. Active Management Styles: Different active management styles, such as value, growth, or momentum investing, can result in varying levels of active risk. Each style has its unique approach to security selection and market timing, which can lead to different deviations from the benchmark index. Passive Management Styles: Passive management styles, such as index funds or exchange-traded funds (ETFs), typically have lower active risk due to their aim to replicate benchmark index performance. Market Volatility: In volatile market conditions, active managers may take more significant deviations from the benchmark to capitalize on opportunities, potentially leading to higher active risk. Market Cycles: Different market cycles may favor different investment styles, leading to varying levels of active risk depending on the active manager's approach. Asset Allocation: The allocation of assets in a portfolio can significantly impact active risk levels, as different asset classes have different risk-return profiles. Security Selection: The specific securities chosen by the investment manager can also influence active risk, as individual securities may have unique risk-return characteristics. Investment Time Horizon: The investment time horizon can impact active risk, as short-term market fluctuations may have a more significant effect on portfolios with shorter time horizons. Active risk management is crucial for achieving investment objectives while maintaining a portfolio's risk within an acceptable range. Definition and Purpose: Active risk budgeting is the process of allocating a specific level of active risk to various investment strategies or managers within a portfolio. This approach helps investors maintain control over their portfolio's overall active risk while seeking excess returns. Techniques and Tools: Investors can use quantitative tools, such as risk models, scenario analysis, and optimization techniques, to determine the optimal allocation of active risk to various strategies or managers. Sharpe Ratio: The Sharpe ratio measures a portfolio's risk-adjusted return by dividing its excess return by its standard deviation (a measure of volatility). A higher Sharpe ratio indicates better risk-adjusted performance. Sortino Ratio: The Sortino ratio is similar to the Sharpe ratio but focuses on downside risk by considering only the negative deviations in returns. A higher Sortino ratio indicates better downside risk-adjusted performance. Risk Tolerance Assessment: Investors must assess their risk tolerance to determine the appropriate level of active risk in their portfolios. Diversification Strategies: Implementing diversification strategies, such as allocating assets across various investment styles, managers, or asset classes, can help manage active risk and enhance portfolio performance. Investment risk refers to the potential for financial losses associated with an investment, and it is crucial to understand the different types of investment risk and how they can affect a portfolio. Systematic risk is inherent in the entire market or market segment, while unsystematic risk is specific to a particular company, industry, or security. The risk-return trade-off principle suggests that higher risk investments have the potential for higher returns, while lower risk investments have lower potential returns. Investors can manage their risk through diversification, which involves spreading investments across various asset classes, industries, and geographies. Active and passive risks are two distinct approaches to investment management, and investors must choose the approach that best aligns with their investment objectives and risk tolerance. Measuring active risk is essential for evaluating investment managers and understanding the risk associated with their investment decisions, and various factors can influence the level of active risk in a portfolio, including investment strategy, market conditions, and portfolio characteristics. Active risk management is crucial for achieving investment objectives while maintaining a portfolio's risk within an acceptable range, and techniques and tools such as active risk budgeting and risk-adjusted performance measures can help investors manage their risk effectively.What Is Investment Risk?

Understanding Investment Risk

Types of Risk

Risk-Return Trade-Off

Diversification and Risk Management

Active Risk vs Passive Risk

Definition and Differences

Role in Portfolio Management

Implications for Investors

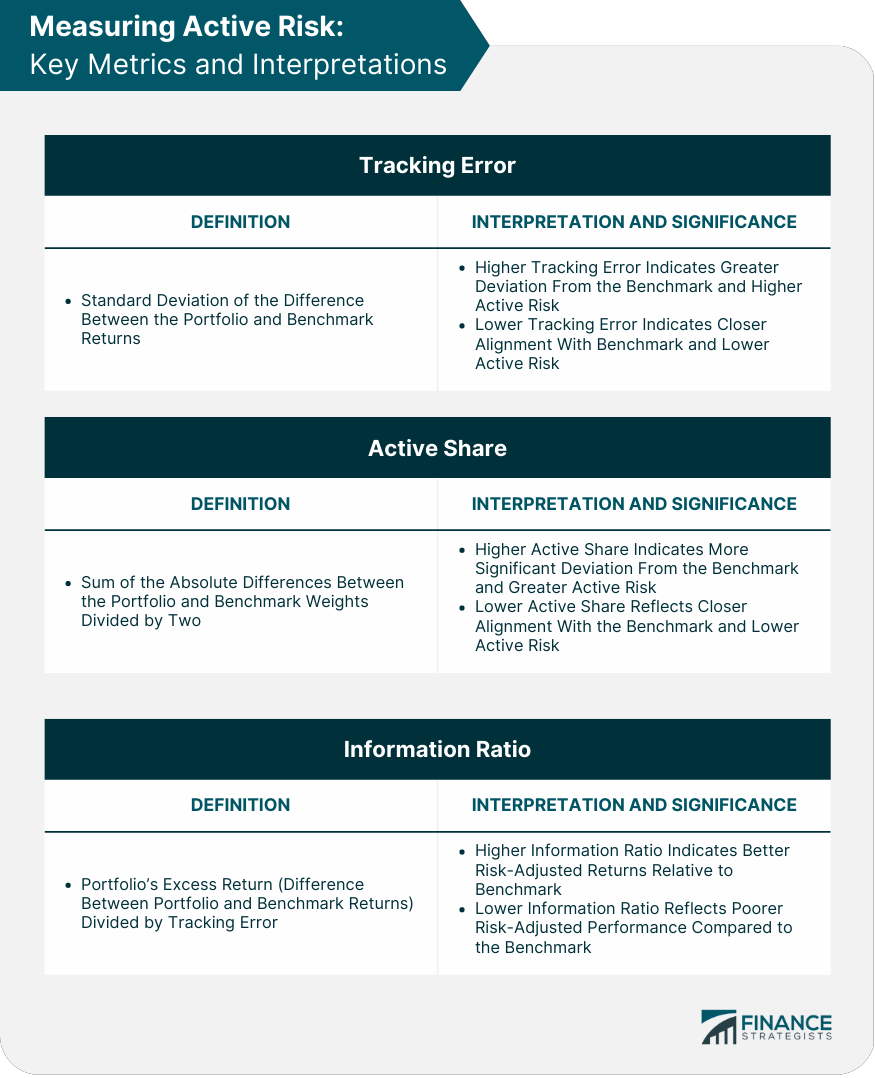

Measuring Active Risk

Tracking Error

Active Share

Information Ratio

Factors Affecting Active Risk

Investment Strategy

Market Conditions

Portfolio Characteristics

Managing Active Risk

Active Risk Budgeting

Risk-Adjusted Performance Measures

Role of Risk Management in Portfolio Construction

Conclusion

Active Risk FAQs

Active risk is the measure of how much the returns of a portfolio deviate from its benchmark. It is also known as tracking error and represents the risk associated with actively managing a portfolio.

Passive risk, also known as systematic risk, is the risk that affects the overall market and cannot be diversified away. Active risk, on the other hand, is the risk specific to a portfolio's active management strategy.

Active risk is important for portfolio managers because it measures the effectiveness of their active management strategy. A higher active risk indicates that the portfolio is deviating significantly from its benchmark, which can either result in higher returns or losses.

Active risk can be reduced by increasing the correlation of a portfolio with its benchmark, reducing the number of active positions, or by selecting less volatile stocks. However, reducing active risk may also lower potential returns.

Active risk is calculated by subtracting the benchmark return from the portfolio return and then calculating the standard deviation of the difference. The formula is: Active Risk = Standard Deviation (Portfolio Return - Benchmark Return).

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.