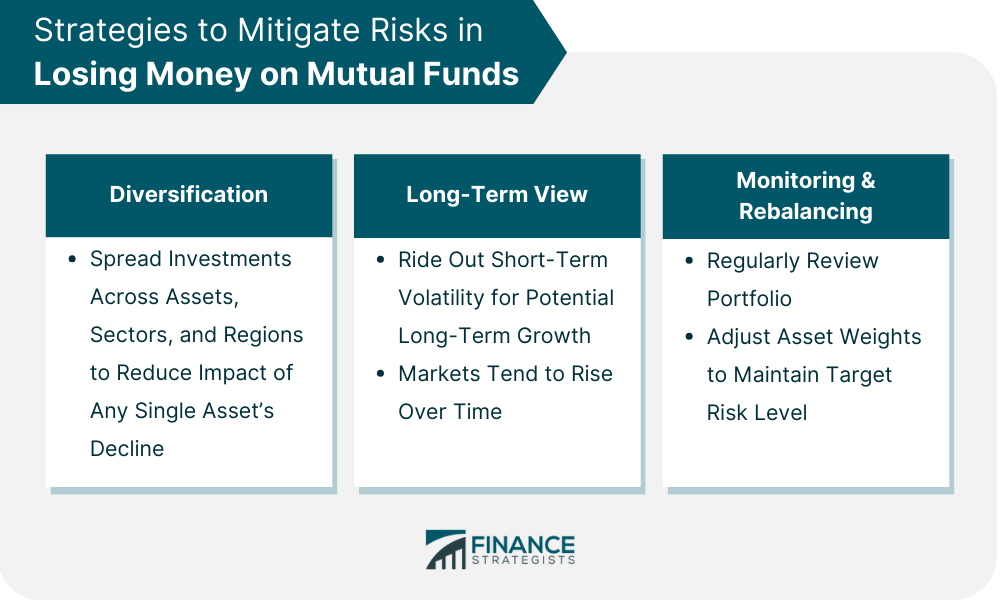

Investing in mutual funds can sometimes result in losses due to market ups and downs, poor management, or economic conditions. Mutual funds gather money from many investors to buy various stocks, bonds, or other securities. Even with this diversification, the value of these investments can fall if the assets do not perform well. High management fees and expenses can also reduce returns, especially in actively managed funds. Economic downturns, interest rate changes, and global events can negatively affect fund performance. Investors might also lose money if they sell their shares during a market drop instead of waiting for a potential recovery. Choosing mutual funds without thorough research, not aligning investments with financial goals, and ignoring the importance of a long-term perspective can increase the risk of losses. Understanding these risks and having a strategic approach is key to reducing potential losses in mutual funds. Market volatility is a primary risk in mutual funds. If a mutual fund is heavily invested in stocks and the market drops, the fund's value decreases, as seen during the 2008 financial crisis and the early COVID-19 pandemic. Mutual fund performance depends on fund managers' decisions about buying and selling securities. Poor decisions, whether due to error or unforeseen market changes, can lead to losses. For example, a manager who fails to predict a sector downturn may cause the fund to suffer. The broader economic environment significantly affects mutual fund performance. Economic recessions, geopolitical tensions, or sector-specific issues can negatively impact markets. For instance, a tech-focused mutual fund might decline during a tech industry slump. Interest rate changes impact bond funds. Existing bonds lose value when rates rise as new bonds offer higher returns. For example, a bond fund holding 3% interest bonds will drop in value if new bonds offer 4%. Credit risk involves the chance that a bond issuer defaults on payments. Government bonds are low risk, while high-yield corporate bonds carry higher risk. Funds investing in "junk" bonds are more exposed to credit risk. Liquidity risk occurs when a fund must sell assets quickly to meet redemptions. Illiquid assets, like certain bonds or real estate, might need to be sold at a loss. This risk is heightened during market stress when many investors withdraw funds. Inflation risk is the possibility that returns will not keep up with inflation, reducing real earnings. Fixed-income investments, like bonds, are particularly vulnerable. For instance, a bond fund returning 3% annually would result in a negative real return if inflation is 4%. Individual investment goals vary greatly, but they often include saving for retirement, accumulating wealth, funding education, or preserving capital. The choice of mutual fund should align with these objectives. For example, growth-oriented funds might be suitable for long-term wealth accumulation, while income-oriented funds could be better for those nearing retirement. Risk appetite refers to an investor's willingness and ability to endure market volatility and potential losses. It is influenced by investment time horizon, financial situation, and emotional comfort with risk. Younger investors often have a higher risk tolerance due to their longer investment horizons, which allow them to recover from market downturns. Conversely, those closer to retirement may prefer more conservative investments. The cost of investing in mutual funds, typically reflected in the expense ratio, can substantially impact net returns. The expense ratio is a key metric that reflects the annual cost of investing in a mutual fund. This percentage, calculated as a portion of the fund's average assets, encompasses management fees, administrative expenses, and other operational costs. To generate the same net returns for investors, funds with high expense ratios need to perform significantly better than lower-cost funds. Index and passively managed funds usually have lower expense ratios than actively managed funds. Investors should compare costs among similar funds and consider how these expenses will affect their investment returns over time. Investors can conduct research using various resources, such as financial websites, mutual fund reports, and investment analysis platforms. Key factors to research include the fund’s performance history, the manager's track record, the fund's investment strategy, and how it has performed under different market conditions. Consulting with a financial advisor can also be beneficial, especially for investors who are new to mutual funds or those with complex financial situations. Financial advisors can provide personalized advice based on an individual’s financial goals, risk tolerance, and investment timeline. The world of mutual funds presents growth opportunities but is equally fraught with potential pitfalls. It is crucial to understand that mutual funds are not a one-size-fits-all solution. They offer a range of options, from conservative income funds to aggressive growth funds, each with its own set of risks and rewards. An informed approach is key. This means understanding the specific mutual fund in which one is investing and recognizing how it fits into the broader context of an individual's overall financial plan. It is about knowing the expected returns, underlying assets, the fund manager's strategy, and how these align with personal financial goals. Understanding the risks involved cannot be overstated. Market volatility, interest rate changes, and economic shifts are just a few of the elements that can impact the performance of a mutual fund. Awareness of these factors and how they might affect investments is critical to, successful mutual fund investing.Losing Money in Mutual Funds Overview

Risks in Mutual Funds

Market Fluctuations

Management Decisions

Economic Downturns

Interest Rate Risk

Credit Risk

Liquidity Risk

Inflation Risk

Choosing the Right Mutual Fund

Investment Goals and Risk Appetite

Expense Ratios and Fees

Research

Conclusion

Can You Lose Money on a Mutual Fund? FAQs

Mutual funds can lose value due to market fluctuations. If the market experiences a downturn, the value of the securities within the fund may decrease, reducing the overall value of the mutual fund.

A mutual fund manager's decisions can impact the fund's performance. Poor investment choices or failure to anticipate market changes can result in losses for the mutual fund.

Interest rate changes can lead to losses in a mutual fund, especially bond funds. When interest rates rise, the value of existing bonds with lower rates tends to fall, decreasing the value of bond-focused mutual funds.

Mutual funds can lose money during economic downturns. Funds invested in sectors or industries hit hard by an economic slump can see a significant decrease in value, affecting the fund's overall performance.

Inflation risk can lead to losses in a mutual fund. If the fund's rate of return does not keep up with inflation, it can erode the real value of the returns, effectively resulting in a loss of purchasing power for the investor.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.