Pooled funds are an investment strategy where multiple investors pool their money together. This pooled capital is then managed by professional fund managers who invest it into a diversified portfolio of assets such as stocks, bonds, or other securities. This collective investment structure allows investors to access a wider range of investments and professional management that they might not have been able to afford individually. Pooled funds have become a crucial part of many investors' strategies due to their several advantages. For starters, they provide an affordable means for small investors to gain exposure to professionally managed, diversified portfolios. They also provide liquidity, as shares in a pooled fund can usually be bought or sold on any business day. Moreover, pooled funds can offer a level of risk management through diversification, as the impact of any single security's poor performance is lessened by the presence of many other securities in the fund's portfolio. Mutual funds are perhaps the most well-known type of pooled funds. In a mutual fund, the money from many investors is pooled together and managed by a professional fund manager. The manager uses this money to create a diversified portfolio of stocks, bonds, or other assets. Each investor owns shares, which represent a portion of the holdings of the fund. Exchange-Traded Funds are a type of pooled funds that are traded on an exchange like individual stocks. ETFs can track an index, sector, commodity, or a basket of assets. They offer the same diversification benefits as mutual funds but can be bought and sold throughout the trading day at market prices. Hedge funds are pooled investment vehicles that are typically available only to certain accredited or qualified investors due to their potential for high risk. They use a range of strategies, including leverage, short selling, and derivatives, to generate high returns. Hedge funds are less regulated than other pooled funds, such as mutual funds or ETFs. Unit Investment Trusts are a type of U.S. investment company offering a fixed (unmanaged) portfolio of securities having a definite life. Unlike mutual funds, UITs provide a set list of stocks or bonds which are not changed over the life of the investment. Closed-end funds are a type of investment company which raises a fixed amount of capital through an initial public offering (IPO). The fund is then structured, listed and traded like a stock on a stock exchange. Unlike regular mutual funds, closed-end funds do not stand ready to issue and redeem shares on a continuous basis. In a pooled fund, the role of the fund manager is crucial. These are the individuals or teams responsible for making the investment decisions for the fund. They determine what assets to buy, hold, or sell, and when to do so. Their decisions are guided by the fund's investment objective, which is outlined in the fund's prospectus. The proficiency of the fund manager can have a substantial impact on the fund's performance. Investors buy units or shares in a pooled fund from the fund itself or through a broker. The price of each unit or share is determined by the net asset value (NAV) of the fund, which is the total value of the fund's assets minus its liabilities, divided by the number of outstanding shares. In open-end funds like mutual funds, new shares are issued whenever investors invest in the fund, and shares are redeemed when investors withdraw their money. In contrast, for closed-end funds and ETFs, a fixed number of shares are issued which are then traded on the stock exchange. The NAV of a pooled fund represents the per-share/unit price of the fund. It's calculated at the end of each trading day based on the total value of the fund's assets, minus any liabilities, divided by the number of outstanding shares or units. The NAV provides an accurate measure of the value of a single share or unit in a fund and fluctuates daily with the changing market value of the fund's assets. One of the primary benefits of investing in pooled funds is diversification. Because pooled funds invest in a wide range of assets, they help spread investment risk. This means that if one or a few investments perform poorly, the impact on the overall portfolio is mitigated by the performance of the rest of the investments. Pooled funds are managed by professional fund managers who have deep knowledge and expertise in selecting and managing investments. This means investors can benefit from professional investment management, which can be particularly beneficial for those who lack the time or expertise to manage their own investments. Most pooled funds, particularly mutual funds and ETFs, offer high liquidity. This means that investors can buy or sell shares in the fund on any business day. This makes pooled funds a flexible investment option that can be suitable for a wide range of investment needs. Pooled funds operate under economies of scale. This means that as more assets are added to the fund, the cost of managing the fund is spread across a larger asset base, which can lower the cost per investor. This makes pooled funds a cost-effective investment option for many investors. Just like any other investment, pooled funds are exposed to market risk, which is the risk of investments losing value due to macroeconomic or market-wide events. Since pooled funds usually invest in a variety of securities, they are susceptible to movements in the overall market or sector. Management risk refers to the possibility that the fund's managers may make poor investment decisions or fail to execute the fund's investment strategy effectively. This can result in subpar performance and potential losses for the fund's investors. While pooled funds generally offer daily liquidity, certain situations could impede this. For example, if a significant number of investors simultaneously decide to sell their shares in a mutual fund, the fund might have to quickly sell assets to meet these redemptions, potentially at unfavorable prices. In extreme cases, a fund might even temporarily suspend redemptions. Operational risk involves the risk of loss from inadequate or failed internal processes, people, and systems, or from external events. This can include issues such as errors in trade execution, record keeping, or other administrative tasks, or outright fraud. Generally, investing in pooled funds carries lower risk than investing in individual securities. This is primarily due to diversification. Because pooled funds spread their investments across a variety of securities, the poor performance of a single security has a smaller impact on the overall portfolio. The potential for higher returns is often greater with individual investments, especially if the investor has a high degree of skill or knowledge. However, the potential for loss is also greater. Pooled funds, on the other hand, aim for consistent, positive returns over the long term. In terms of cost, pooled funds typically charge a management fee and other operational expenses, which are proportionally shared among all investors. Individual investments, on the other hand, may involve broker commissions or transaction fees. However, they do not have ongoing management fees. Different pooled funds have different objectives and risk levels, so it's crucial to select a fund that aligns with your own investment goals and risk tolerance. For instance, if you're saving for retirement and have a long time horizon, you may be comfortable with a fund that takes on more risk in pursuit of higher returns. On the other hand, if you're saving for a short-term goal, a lower-risk fund may be more suitable. While past performance isn't a guarantee of future results, reviewing a fund's track record can provide insight into how it has managed different market conditions and how it compares to similar funds or its benchmark index. Fees and expenses can significantly impact your returns over time, so it's important to understand a fund's cost structure. This includes management fees, administrative costs, and any sales charges or redemption fees. The expertise and experience of the fund manager or management team can significantly impact a fund's performance. It's worth researching their background, their investment strategy, and how long they've been managing the fund. Pooled funds can play a crucial role in asset allocation, allowing investors to easily diversify their portfolios across different asset classes, such as equities, bonds, commodities, or real estate. Investing in pooled funds can be an efficient way to achieve a diversified portfolio. Because each fund holds a variety of securities, investors can achieve diversification with fewer transactions than if they were to buy each security individually. Pooled funds can also be an effective risk management tool. Different funds have different risk profiles, so investors can choose a combination of funds that aligns with their overall risk tolerance. Pooled funds in the United States are regulated by the Securities and Exchange Commission (SEC) under the Investment Company Act of 1940. They must register with the SEC and provide disclosures to investors about the fund's investments, operations, and expenses. The Financial Industry Regulatory Authority (FINRA) also oversees broker-dealers who sell fund shares, ensuring they comply with fair practice rules. Pooled funds are required to comply with a range of regulatory requirements. These include maintaining sufficient liquidity, keeping accurate records, conducting regular audits, and providing regular reports to investors. They must also have policies in place to manage conflicts of interest and prevent fraudulent activity. Regulation also provides protections for investors. For example, pooled funds must value their assets daily, allowing for accurate calculation of the net asset value per share. This ensures investors receive a fair price when they buy or sell shares. Funds must also have a custodian to hold their assets, providing an additional layer of oversight and protection. Pooled funds are investment vehicles where multiple investors pool their resources together to gain exposure to a professionally managed portfolio. They provide an affordable and efficient way for investors to access a wide range of securities. Investing in pooled funds can offer several advantages, including diversification, professional management, and high liquidity. However, like all investments, they come with risks and costs. Therefore, it's important to thoroughly research any fund before investing and to consider how it fits within your overall investment strategy and risk tolerance. It is crucial to consult with a financial advisor before making investment decisions. An advisor can provide personalized advice based on your individual circumstances, goals, and risk tolerance.What Are Pooled Funds?

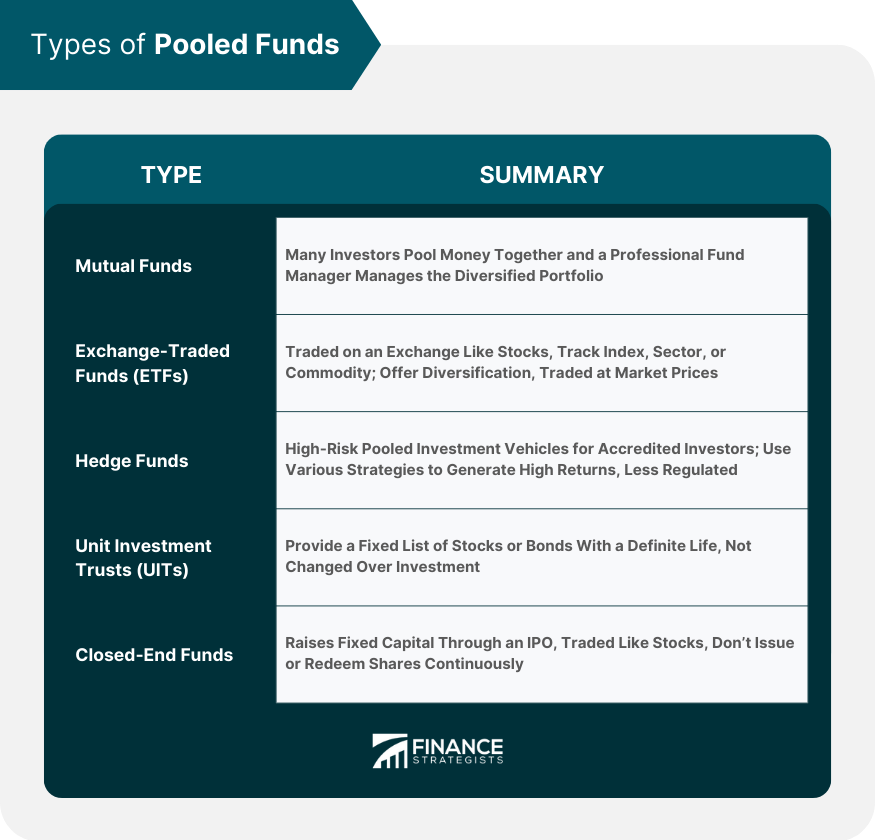

Types of Pooled Funds

Mutual Funds

Exchange-Traded Funds (ETFs)

Hedge Funds

Unit Investment Trusts (UITs)

Closed-End Funds

Working Mechanism of Pooled Funds

Role of Fund Managers

Process of Buying and Selling Units or Shares

Fund Valuation

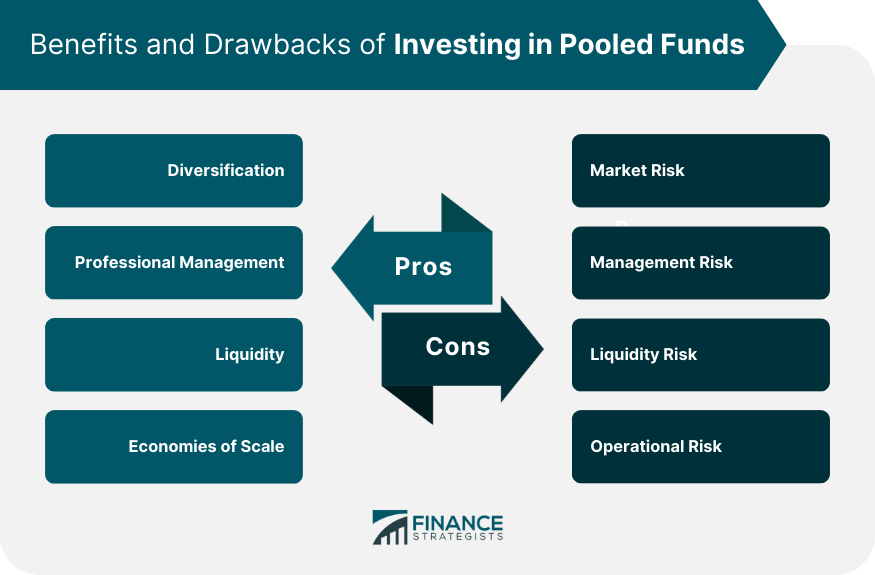

Benefits of Investing in Pooled Funds

Diversification

Professional Management

Liquidity

Economies of Scale

Drawbacks of Investing in Pooled Funds

Market Risk

Management Risk

Liquidity Risk

Operational Risk

Pooled Funds vs Individual Investments

Comparison Based on Risk

Comparison Based on Return

Comparison Based on Cost

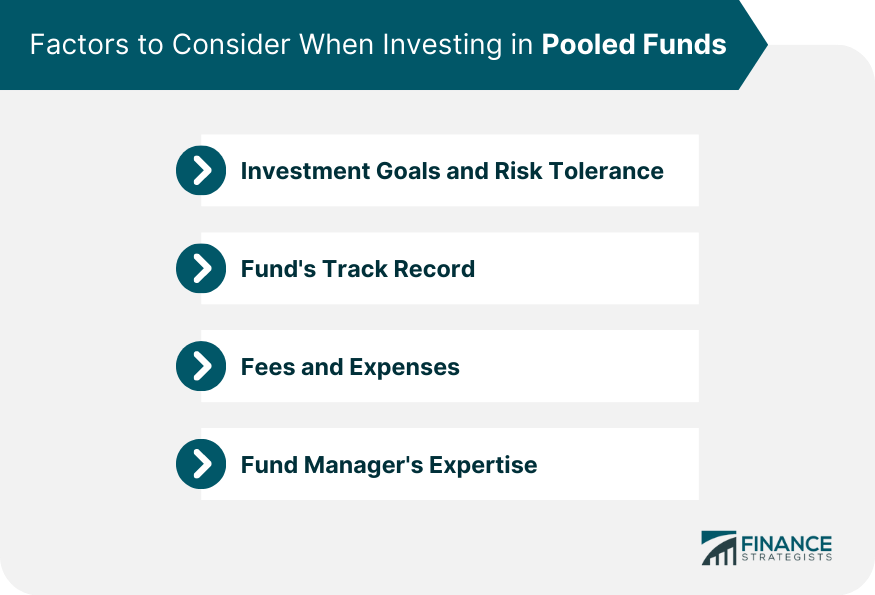

Factors to Consider When Investing in Pooled Funds

Investment Goals and Risk Tolerance

Fund's Track Record

Fees and Expenses

Fund Manager's Expertise

Role of Pooled Funds in Portfolio Construction

Asset Allocation

Diversification Strategy

Risk Management

Regulation of Pooled Funds

Regulatory Bodies

Compliance Requirements

Investor Protection Measures

Final Thoughts

Pooled Funds FAQs

Pooled funds, also known as collective investment schemes, are investment vehicles that pool money from many investors and use it to invest in a diversified portfolio of stocks, bonds, and other assets. This allows individual investors to gain access to a broader range of investments than they might otherwise be able to afford.

Pooled funds work by pooling the money of many investors into a single investment vehicle, such as a mutual fund, exchange-traded fund (ETF), or hedge fund. The fund's manager then uses the pooled money to invest in a diversified portfolio of assets on behalf of the investors. Investors own shares in the fund and receive a portion of the fund's returns in proportion to the number of shares they own.

Investing in pooled funds offers several benefits, including diversification, professional management, liquidity, and access to a wider range of investment opportunities. By pooling their money with other investors, individuals can gain access to a broader range of investments than they might be able to afford on their own. Additionally, pooled funds are typically managed by professional investment managers who have the expertise and resources to manage the fund's portfolio effectively.

Like any investment, pooled funds come with risks. These risks include market risk, liquidity risk, credit risk, and manager risk. Market risk refers to the risk of losing money due to fluctuations in the value of the underlying assets. Liquidity risk refers to the risk of not being able to sell your shares in the fund when you want to. Credit risk refers to the risk of the fund's investments defaulting on their debt obligations. Manager risk refers to the risk of the fund's manager making poor investment decisions.

Investing in pooled funds is relatively easy. Investors can buy shares in mutual funds, ETFs, or hedge funds through a broker or directly from the fund company. To invest in a mutual fund or ETF, investors typically need to meet a minimum investment requirement, which can range from a few hundred dollars to several thousand dollars. Hedge funds are typically only open to accredited investors who meet certain income and net worth requirements.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.