A unit investment trust (UIT) enables investors to buy into a fixed portfolio of stocks, bonds, and other securities in one transaction. Generally, the trust has a set maturity date or termination date at which the fund will be liquidated, distributing any proceeds to the investors. UITs are just one of three investment companies that pool investor money to make it easier for people to build diversified portfolios at a lower cost. The other two types are mutual funds and closed-end funds. Unlike mutual funds, unit investment trusts are not actively traded in the markets. Instead, their underlying securities are held for extended periods and only bought or sold whenever there is a significant change in their underlying investments, such as a corporate merger or bankruptcy. UITs tend to be associated with more low-risk strategies and are often chosen as long-term investments rather than short-term trading instruments. UITs are investment options for those seeking capital growth and income. They enable investors to gain ownership of trust by purchasing units, typically in a one-time public offering. Each unit is equal to an ownership slice of the trust, giving the investor their rightful share of any income or profits generated by the fund's investments. Since the performance of UITs is primarily determined by the success of their underlying investments, investors must wisely choose when deciding which type of UIT they want to invest in. UITs generally have fixed investments with a predetermined lifespan, ranging from 15 months to more than ten years; investors can redeem their shares early if they change their objectives. A UIT can offer investors an attractive, low-cost way to achieve a certain level of investment performance. Here are some key features of UITs: A UIT is established to invest in a professionally selected and diversified portfolio of securities designed to meet a particular stated objective, such as growth, income, or capital appreciation. A key attribute of a UIT is its “buy-and-hold” strategy which remains in place until the end of the UIT’s term – thereby allowing investors to potentially reduce volatility by limiting trading activity. The potential risks associated with each security within the trust are also clearly outlined in the prospectus. Allowing investors to understand exactly what they own and take advantage of fast-changing markets over time makes UITs an attractive long-term option. A UIT investment is hugely beneficial to the average investor, as it allows them to access a diversified portfolio of securities, such as stocks and bonds, without having to construct it themselves. Additionally, this portfolio typically has been designed by an experienced team of financial advisors. These advisors understand the complexities of their asset classes and can craft strategies that mitigate risk while optimizing gains. As these professionals have thoroughly evaluated their holdings, investors can benefit from an aggregated portfolio that spreads and offsets potentially unprofitable investments with those with a better chance of earning a return. UITs offer various products to meet every investor's varying and specific needs. They can be categorized into two main types based on their underlying securities - fixed-income and equity - with various UITs available within each. The array of securities open for investment is quite broad, allowing investors to choose from a range, including municipal and corporate bonds, US government securities, domestic or foreign common stocks, preferred stocks, mortgage-backed securities, and international bonds. Thus, it is easy to tailor an investment to fit any investor's objectives and risk tolerance level. An often attractive feature that makes UITs desirable for many investors is the regularity of their interest payments. Fixed-income UITs, for instance, often distribute payments monthly, adding a constant income stream to an investor's portfolio. In comparison, investors who purchase bonds separately and directly experience more sporadic interest payment intervals - such as semiannually or annually. On the other hand, equity UITs may provide investors with monthly, quarterly, or semiannual dividend payments. Regardless of the chosen UIT type, there is always the possibility of experiencing losses amid market volatility, which should be considered when making any investing decisions. Fixed-income and equity UITs allow investors to benefit from automatic reinvestment of their distributions. With a fixed-income investment, this reinvestment typically occurs in a mutual fund with securities of a similar value and nature. The distributions are put back into the same trust for an equity UIT via extra units. Regardless of the strategy, reinvestment is advantageous as it allows yield compounding to occur, resulting in a higher potential return over time. Investors can also exchange units of one UIT for another to suit their changed investment objectives and market outlook. This is often accompanied by a reduced sales charge when purchasing new units through an exchange. Fixed-income UITs offer an "estimated current return," which is calculated by taking the estimated net annual interest income per unit divided by the offering price. This provides a measure of the trust's current cash flow. Meanwhile, the total return of an equity UIT is determined by the price changes of the securities held in it, plus the reinvestment of any income received from said securities. This figure is calculated by dividing all realized and unrealized gains by the original public offering price. It should be noted that returns for fixed-income UITs are more predictable because the bonds contained within them are often held until maturity. In contrast, the returns for equity UITs tend to fluctuate according to stock valuations and market conditions at home or abroad. Investors looking to obtain price quotes for UITs have plenty of options to choose from. But before investing, it is important to know where to find UIT price quotes. Many reputable brokerages offer quotes, as do some other sources such as Nasdaq's Mutual Fund Quotation Service or weekly publications like Barron’s. Broker-dealers may also sponsor their own trusts or sell those offered by independent sponsors, allowing investors to purchase units from their registered representatives. Smaller investment firms sponsored by third-party bond or brokerage firms also sell UITs. It is worth noting that although only a limited number of units are available in an initial public offering (IPO), many trust sponsors provide secondary markets for these investments, which helps increase liquidity. Although many investors purchase units to hold them until the trust terminates, UIT investors may sell their units at any time in the secondary market. In addition, for UITs without a secondary market, these trusts are required by law to redeem (buy back) outstanding units at their net asset value (NAV). This is based on the current market value of the underlying securities. The NAV may be more or less than the price the investor paid initially. If an investor’s objectives change, some UIT sponsors allow them to exchange units for another UIT at a reduced sales charge. Unit trusts can be purchased, sold, or exchanged on any business day at the current net asset value—including the deduction of applicable sales charges. Unit investment trusts are one of the most secure investments available due to their strict regulation by federal government laws and oversight from the U.S. Securities and Exchange Commission (SEC). Because of this, they must utilize the same federal securities rules when offering publicly available investments as mutual funds and closed-end funds provided in the Securities Act Of 1933. To ensure its structure and operations stay legally compliant, the Investment Company Act of 1940 lays out even more detailed rules that UITs must abide by. Those regulations include a requirement to supply investors with a prospectus document upon purchase which outlines information such as investment objectives, portfolio inclusions, and sales/expenses fees associated with buying and selling units. UITs offer an affordable option to investors looking to diversify their investments. With a one-time purchase, investors can access a portfolio of several stocks and bonds. The minimum investment for UITs is usually $1,000 but can be lowered even further if bought through an IRA. A sales charge or load is typically due when making the initial purchase, and there may also be deferred charges if applicable. The offering price for such trusts comprises the NAV and the sales charge; large purchases may qualify for discounts on the sales charge. A UIT's annual fee covers the sponsor's supervision, organization costs, and a creation and development fee. Unlike other investment options, UITs do not charge investment management fees. Transaction costs are significantly reduced due to the limited buying and selling of portfolio securities. Plus, there are no ongoing marketing fees associated with the trust since most UITs do not market themselves directly to potential investors. Some UITs provide income that is free from federal or state taxes. However, unitholders must generally pay income taxes on the dividends, interest, and capital gains they gain from investing in UITs. Individuals who invest in UITs through retirement accounts, such as a traditional 401(k), may be able to defer these taxes until withdrawals are made from these accounts. UITs provide Form 1099 annually to unitholders to summarize distributions. For example, when an investor sells units, any resulting gain or loss must be reported on this tax return form. There are various types of UITs available that can address the need of any investor. Below are some of them: These UITs hold bonds issued by corporations. Investing in a corporate bond UIT can be an ideal way to add a low-risk but high-return income into one’s portfolio. Several UITs avail of private insurance to guarantee timely interest and principal payments on the bonds within the trust. Investing in investment-grade bonds is another way other UITFs secure returns for investors who choose an uninsured UIT. Equity UITs allow investors to diversify their portfolios by choosing from various stocks. Popular specialty trusts offer portfolios mirroring popular indices, while other UITs focus on specific market trends such as telecom and healthcare. With equity UITs, more sophisticated investors can choose among various investment approaches and strategies, including contrarian, growth and value, and emerging market investments. International Bond UITs offer investors a great way to access foreign, fixed-income markets that might be outside their usual scope. Investing in these trusts provides an investor with exposure to debt issued by foreign companies and governments, allowing them to capitalize on the potentially high returns offered in these markets. While participating in international markets subjects an investor to extra volatility due to fluctuating currency rates, the potential payoffs often outweigh the risks. A middle-income investor can become an international player with the right mindset and the proper UITs. Mortgage-Backed Securities UITs are another way to achieve higher income levels without taking extra risks. Government-sponsored entities, like Ginnie Mae and Freddie Mac, back these investments. These securities offer the investor a steady income stream and open them up to the potential of capital gains when interest rates go up. Investing in Mortgage-Backed Securities UITs requires researching and understanding the security's complexities and associated risks. Still, it can be an excellent investment for those willing to take the time to learn about them. Investing in municipal bonds can be an attractive option for higher-income taxpayers looking to make a safe, tax-advantaged investment. States and municipalities issue these bonds to fund public projects like schools, highways, hospitals, and airports. The income earned on these securities is often exempt from federal income taxes. It is important to remember that some taxpayers may still be subject to the alternative minimum tax for municipal bond investments. State Municipal Bond UITs offer a unique benefit to residents of the state in which they are issued. If these residents receive income from investing in a UIT containing this state’s municipal bonds, this income is exempt from both federal and state income taxes. This tax-exempt income opportunity can even include further exemption from local and other kinds of taxes. However, in some cases, portions of income may be subject to the federal alternative minimum tax, so individuals should check the specific details before investing. U.S. Government Securities UITs can provide investors with a reliable source of income while mitigating risk. These trusts invest in various fixed-income securities issued directly by the United States government, such as Treasury bonds and other government notes. Such investments are highly sought after because of their guaranteed low-risk nature, making them an attractive option for many. As a result, these types of trusts can offer investors consistent returns through the safety provided by government-issued securities. Unlike mutual or closed-end funds, a UIT always has an end date determined by the investments in its portfolio. For example, if its portfolio holds bonds with five-, 10- and 20-year maturities, its expiration date will be set when the last 20-year bonds mature. At this time, investors receive their fair share of UIT's remaining net assets. Because it is not actively traded, securities are purchased or sold only when specific changes within the underlying investments occur, such as corporate mergers or bankruptcies. This ensures that investors still get their expected returns from their holding periods. While UITs offer the convenience and simplicity of 'buy and hold’ until maturity, investors can sell their holdings back to the issuing investment company at any time. This redemption may come with several considerations since investors should be aware that the amount paid for their holdings may be less than if they kept it until maturity, as bond prices rise and fall with changing market conditions. Some UITs provide the additional flexibility of allowing investors to exchange their holdings for a different one for a reduced sales charge. This can be helpful in case an investor's needs or objectives change over time. Unit Investment Trusts and mutual funds have a good deal in common – both invest large sums of money composed of multiple securities, such as stocks and bonds, intending to spread out risk. However, there are some differences between the two that investors should be aware of. Unlike mutual funds, UITs do not actively engage in trading. This means the fund stays fixed a certain way, regardless of market winners and losers. On the other hand, mutual funds can sell or buy stocks in their portfolio at any time without notice to investors. This means that investors must keep a close watch on these open-ended funds if they wish for their financial goals to be realized. Mutual funds and UITs provide investors with the opportunity to diversify their portfolios. By pooling together capital rather than investing individually in every security, these tools significantly reduce the risk for investors and make it easier for them to invest in various securities. The SEC adds an extra layer of protection by regulating mutual funds and UITs to ensure that the financial interests of all involved are looked after. Overall, these two instruments make it easier for investors to build a more resilient portfolio and protect their long-term wealth goals. A Unit Investment Trust, or UIT, is a type of investment vehicle that offers investors diversified portfolios managed by professionals. It is considered a passive investment because it is pre-packaged and follows the market's movements. With a UIT, an investor buys units through initial public offerings, and those units remain fixed throughout the trust's lifespan. They can be redeemed before maturity, with the redemption value based on the underlying value of the portfolio at that time. There are various UITs available to investors, including corporate bond UITs, equity UITs, international bond UITs, mortgage-backed securities UITs, national municipal bond UITs, state municipal bond UITs, and U.S. Government Securities UITs. While UITs can be profitable investments for certain types of investors, it is essential to do careful research before making any decisions. Consult with a financial advisor to see if unit investment trusts best suit your individual needs and situation.What Is a Unit Investment Trust (UIT)?

How UITs Work

Key Features of UITs

Professional Selection

Diversification

Variety

Distribution Frequency

Reinvestment and Exchange

Investment Return

Buying and Selling Units

Liquidity

Regulation and Disclosure

Fees and Expenses

Taxes

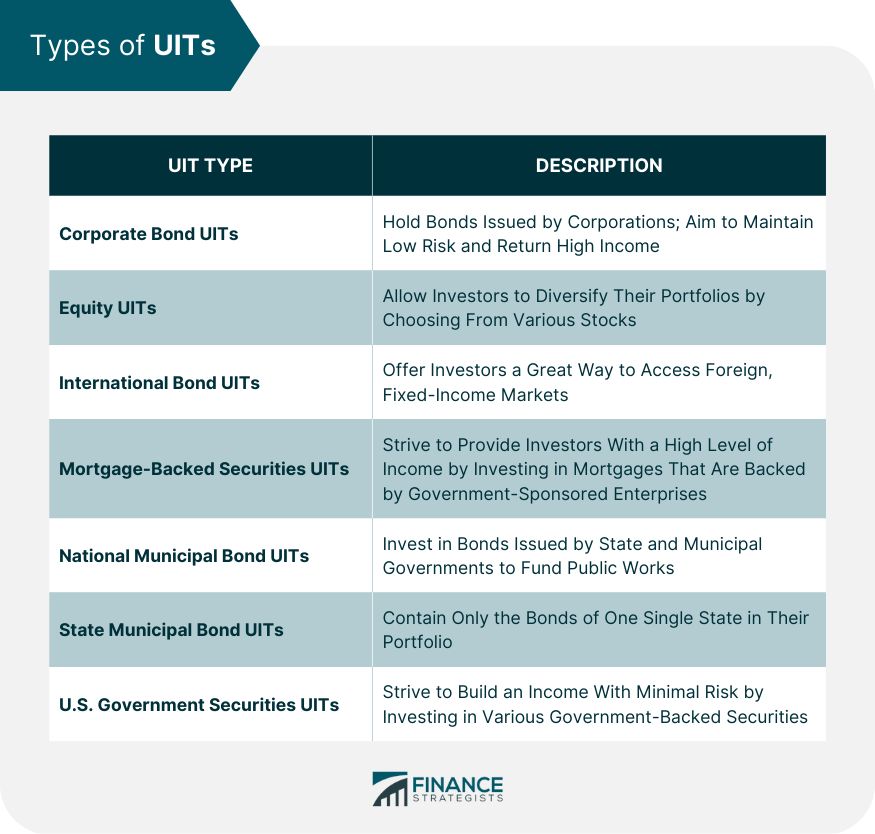

Types of UITs

Corporate Bond UITs

Equity UITs

International Bond UITs

Mortgage-Backed Securities UITs

National Municipal Bond UITs

State Municipal Bond UITs

U.S. Government Securities UITs

Termination Date of UITs

Early Redemption/Exchange of UITs

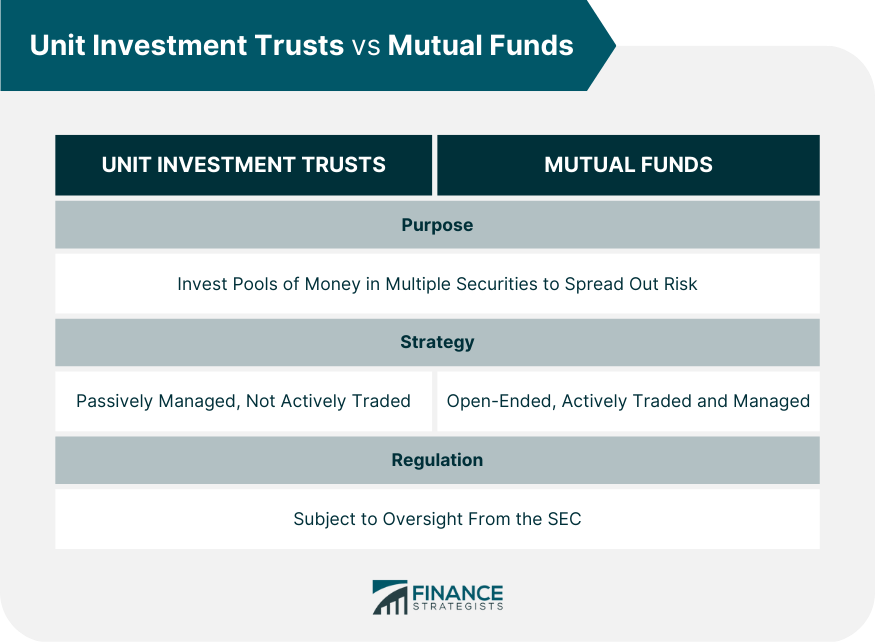

UITs vs Mutual Funds

Final Thoughts

UITs are assembled by an investment company. They have a fixed portfolio, and managers do not have the discretion to modify their investments. On the other hand, mutual funds allow managers to actively choose and trade different securities to meet their investment objectives.

Unit Investment Trust (UIT) FAQs

Upon maturity of a UIT, investors receive the proceeds of the underlying securities held within the trust. Investors may also have their original principal returned to them if applicable.

Yes, it is possible to lose money investing in a UIT due to market fluctuations and other risks associated with the investment. UITs are often considered a low-risk investment option. However, like any further investment, there is the potential for loss.

Unlike mutual funds, UITs are not actively traded, which means the securities they contain remain unchanged unless a corporate merger or bankruptcy occurs. To get around this, investors can choose to sell their UIT on the secondary market, redeem the UIT with the fund, or transfer investments to another UIT.

UITs are typically valued based on the net asset value of the underlying securities held within the trust and may fluctuate with changes in market conditions. Prices for UITs can be found through online brokerage services or by contacting your broker’s office for more information.

UITs can be a good investment, depending on an individual’s financial goals and risk tolerance. They offer low-risk options with stable returns. However, investing in UITs also come with certain drawbacks, such as the relative lack of liquidity and the risk that the securities contained in the UIT may bring lower returns when the markets shift since they remain unchanged for extended periods.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.