A listing agreement is a legal document between a property owner (seller) and a licensed real estate broker. The agreement authorizes the broker to represent the seller and transact the property sale on the owner's behalf. The primary purpose of a listing agreement is to define the terms and conditions under which the broker will operate. It sets out both parties' rights and obligations, the agreement's length, the property's listing price, and the broker's commission. The listing agreement is vital because it provides legal protection to both parties and outlines the framework for the property sale. Understanding listing agreements enables informed decisions, ensuring fair property sale transactions. In an exclusive right-to-sell agreement, the seller grants their broker exclusive rights to sell the property. The broker is entitled to the commission regardless of who brings in the buyer. An exclusive agency agreement allows the broker to sell the property, but the seller retains the right to sell it themselves. The broker does not receive a commission if the seller finds the buyer. An open listing is a non-exclusive agreement allowing multiple brokers to try to sell the property. The seller also retains the right to sell the property themselves. A net listing agreement involves the broker selling the property for a price above a minimum set by the seller. The broker's commission is the difference between the selling price and the net price set by the seller. In any listing agreement, it's crucial to identify all parties involved accurately. This typically includes the full legal names of the seller and the broker and, in some cases, may also include the brokerage firm's name. The parties' contact information should also be included, such as addresses, phone numbers, and email addresses. This precise identification helps avoid confusion and potential legal complications. The listing agreement should provide a comprehensive description of the property being listed. This includes the property's address and a legal description based on the property deed. It should also detail the property's key characteristics, such as the number of rooms, property type (e.g., single-family, condominium), square footage, and any noteworthy features (e.g., pool, garage). Any included personal property or fixtures, such as appliances or custom-built furniture, should also be detailed. The listing price—the amount for which the property will be initially offered on the market—should be clearly stated in the listing agreement. Determining this price is usually a collaborative effort between the seller and the broker, considering various factors like the property's condition, the local market conditions, and recent sales of similar properties in the area. The agreement must specify its effective date and when it will terminate. This term can vary but typically ranges from six months to a year. The agreement term should provide sufficient time for the broker to market the property effectively and allow the seller to reevaluate if the property doesn't sell within the agreed period. The agreement should clearly outline the duties and obligations of the seller. This may include maintaining the property in good condition, providing all necessary disclosures (e.g., known property defects, property's legal status), cooperating with the broker in showing the property and providing all necessary documentation related to the property. The broker's responsibilities, too, need to be explicitly laid out in the agreement. Duties typically include marketing the property, presenting all written offers to the seller, negotiating terms on behalf of the seller, and coordinating the closing process. In fulfilling these duties, the broker must adhere to professional standards and legal requirements, including the duty to put the seller's interest ahead of their own. The listing agreement should detail the broker's compensation for their services. This is usually a commission—a percentage of the property's selling price—paid by the seller at closing. The agreement should specify the commission amount when it is earned (usually upon the sale of the property) and any conditions under which the commission might be shared with other brokers involved in the transaction. This clear arrangement helps avoid commission disputes later. Before a listing agreement can be made, a seller must choose a suitable brokerage to represent their interests best. The seller should consider the broker's reputation, experience in the market, and the broker's marketing strategy. After choosing a brokerage, the seller and broker will negotiate the terms of the listing agreement. This includes the listing price, the duration of the agreement, and the commission to be paid to the broker. Both parties must agree on these terms to avoid conflicts down the line. The seller must prepare the property for sale, which may involve home repairs, staging, and professional photography. The broker might also suggest making the property more appealing to potential buyers. Once all the terms have been finalized and the property is ready for sale, the seller and the broker sign the listing agreement. This legally binds both parties to their respective roles and duties. After signing the agreement, the broker markets the property to potential buyers. This could involve open houses, online listings, and direct mailings. When a buyer shows interest, the broker will handle negotiations on the seller's behalf. If a satisfactory offer is made, the broker will coordinate with the buyer's agent to finalize the sale. This includes handling paperwork, facilitating inspections, and ensuring that all conditions of the sale are met. After the sale is completed and the property changes hands, the seller pays the agreed-upon commission to the broker. Remember, it's important to read and understand all the terms of a listing agreement before signing. Sellers should feel free to ask their broker any questions they may have about the process. One of the most straightforward ways a listing agreement can terminate is through expiration. At the outset, the agreement stipulates a certain duration for which it remains effective—often six months to a year. If the property is not sold within this period, the agreement naturally concludes, freeing the seller to either relist the property, possibly with a different broker or take the property off the market. There are instances where the broker and seller agree to end the listing agreement before expiration. The seller may have had a change of heart about selling the property, or both parties might acknowledge that their working relationship isn't proving effective. In such cases, a mutual agreement can be reached to terminate the listing agreement, ideally documented in writing to avoid any future disputes. If the broker or the seller fails to uphold their responsibilities as outlined in the listing agreement, it can lead to termination due to a breach of contract. For instance, if the broker does not make a diligent effort to sell the property as promised or if the seller withholds relevant information about the property, it may constitute a breach. Typically, the party who is not in breach would have the right to terminate the agreement. However, what counts as a breach should be explicitly defined in the agreement itself to avoid ambiguity. Lastly, the listing agreement naturally concludes when it fulfills its purpose—the property sale. Once the broker finds a buyer, the transaction is completed, and the seller pays the agreed-upon commission, the listing agreement is considered performed. However, it's essential that the agreement clearly specifies what constitutes a sale or transfer of the property. For example, the sale is complete once the seller accepts a written purchase offer or at the closing when the property's title is officially transferred to the buyer. The listing agreement must comply with fair housing laws, prohibiting discrimination based on race, color, religion, sex, disability, familial status, or national origin. The broker is ethically required to ensure equal professional service to all, without prejudice, maintaining the seller's compliance with these laws. In the context of antitrust laws, brokers must avoid discussions or agreements on set commission rates, which can be seen as price-fixing. The listing agreement must also avoid any non-compete clauses or practices that restrict free trade or promote monopolistic behaviors, ensuring ethical competition in the market. Brokers and sellers must adhere to legal requirements for property disclosures in the listing agreement, disclosing all known material defects and conditions that could affect the property's value or desirability. Ethically, this honesty fosters transparency and trust and protects buyers' interests, mitigating legal disputes. In the context of Initial Public Offerings (IPOs), a listing agreement is a contract signed between the issuing company and the stock exchange where the company's shares will be listed. The listing agreement has a different role here than in real estate, but its main purpose is to ensure compliance with regulations and to set out the terms and conditions for listing. 1. Regulatory Compliance: A listing agreement lays out the various terms, conditions, and covenants which a company agrees to comply with, as per the regulations of the securities and exchange board. This is crucial for maintaining transparency, investor protection, and overall market integrity. 2. Corporate Governance: The agreement typically contains requirements regarding corporate governance, such as the company's board structure, disclosure norms, and other responsibilities. This can play a significant role in how the company is managed after the IPO, potentially influencing investor confidence and the company's reputation. 3. Price and Quantity of Shares: The listing agreement may specify details about the IPO, such as the number of shares to be issued and the price range for the shares. It could also include details about any lock-up periods during which certain shareholders are prohibited from selling their shares. 4. Rights and Responsibilities: The agreement sets out the rights and responsibilities of the issuer (the company launching the IPO) and the stock exchange. This can include details about fees, listing procedures, and the obligations of both parties. 5. Delisting Procedures: It may also set out conditions under which the company's shares could be delisted from the exchange, which can impact investors' decisions to buy or sell the shares. The listing agreement plays a vital role in IPOs, governing the relationship between the company and the stock exchange, ensuring regulatory compliance, and influencing how the company operates post-IPO. It can significantly impact the IPO's success and its longer-term performance. Disputes can arise if a broker or seller misrepresents the property, whether intentionally or unintentionally. This could involve aspects such as the property's condition or its potential for returns. Brokers have a fiduciary duty to act in the best interest of their clients. If a broker violates this duty, they can be held liable. Disagreements over the broker's commission can lead to disputes. This often happens if the contract needs to be more explicit about when the commission is earned or how it's calculated. Negotiation is typically the first step taken to resolve a dispute in a listing agreement. It involves open communication between the seller and the broker to address the issue at hand. This method relies on both parties' goodwill and cooperative engagement, often leading to mutually agreeable outcomes. Negotiation is usually cost-effective and less time-consuming, keeping the parties' business relationship intact. Mediation may be the next step if the negotiation fails to bring a resolution. Mediation involves the participation of a neutral third party, known as the mediator. The mediator facilitates discussions between the disputing parties, helping them to understand each other's viewpoints and guiding them toward a mutually acceptable resolution. It is important to note that a mediator does not impose a decision but rather aids in the problem-solving process. This method is less formal and less adversarial than court proceedings, preserving business relationships while also saving time and cost. Arbitration is another dispute resolution process involving a neutral third party, known as an arbitrator. However, unlike mediation, the arbitrator decides on the dispute after hearing arguments and reviewing evidence from both parties. Depending on the agreement, arbitration can be binding, where the arbitrator's decision is final and enforceable by law, or non-binding, where the decision serves as a recommendation but isn't legally enforceable. Arbitration is typically faster and less expensive than litigation but more formal and binding than mediation. Litigation is the last resort for resolving disputes arising from a listing agreement. It involves a court process where a judge or a jury makes a final, legally binding decision. While litigation offers a definitive resolution, it's usually a lengthy, expensive, and public process. It is also adversarial in nature, potentially damaging the business relationship between the disputing parties. Therefore, parties typically consider litigation only when all other dispute resolution methods have failed or when the dispute involves significant legal issues or high stakes. A listing agreement is a legally binding contract between a property owner and a real estate broker. It outlines the terms and conditions of the property listing and the responsibilities of both parties. Understanding the listing agreement is crucial for both sellers and brokers. It protects both parties' rights and provides a clear roadmap for the sale of the property. With technology transforming the real estate industry, staying informed about these changes can help both sellers and brokers navigate the market successfully. For sellers, it's crucial to understand all aspects of the listing agreement before signing. For brokers, staying informed about legal and technological changes can help provide better services to clients. Proper understanding and management of real estate transactions, including listing agreements, can contribute significantly to wealth management. Ensure you have the right knowledge and the right professionals by your side to maximize your returns.What Is a Listing Agreement?

Types of Listing Agreements

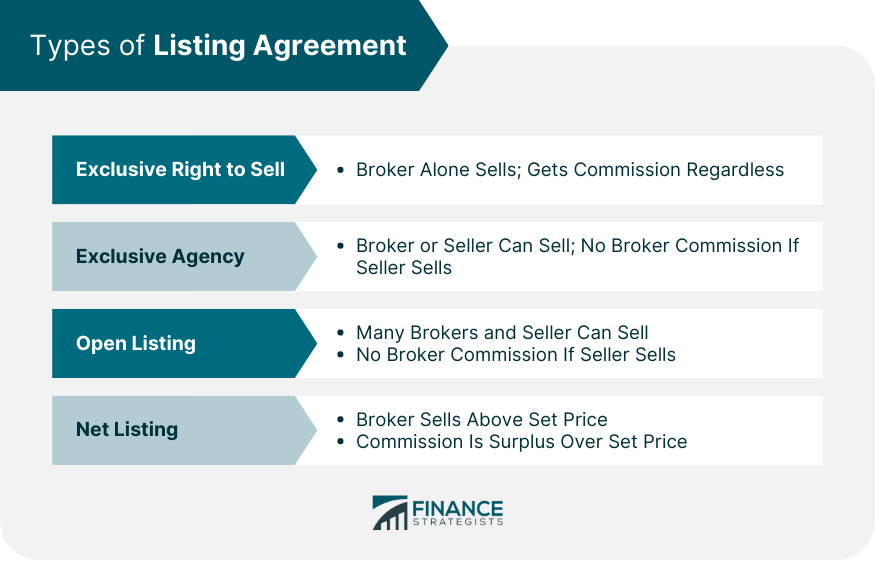

Exclusive Right to Sell

Exclusive Agency

Open Listing

Net Listing

Components of a Listing Agreement

Identification of Parties

Property Description

Listing Price

Duration of the Agreement

Duties and Obligations of the Seller

Duties and Obligations of the Broker

Commission Arrangement

Listing Agreement Process

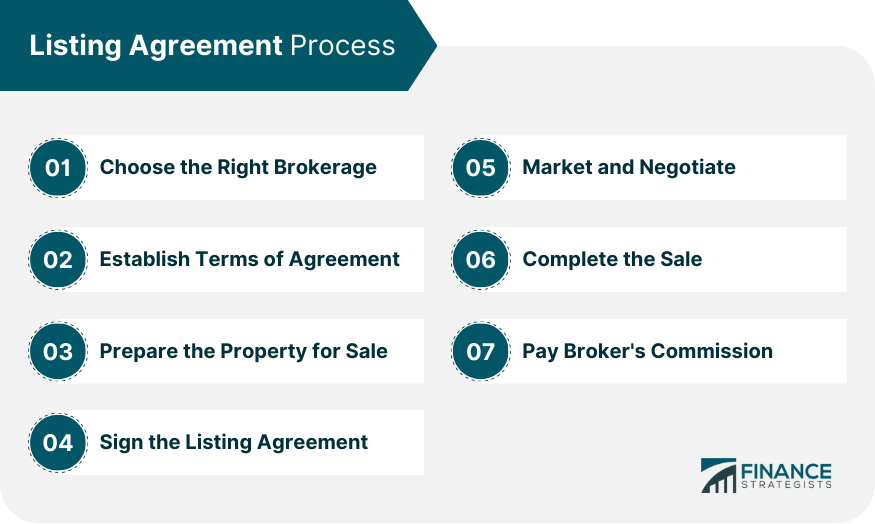

Step 1: Choosing the Right Brokerage

Step 2: Establishing Terms of Agreement

Step 3: Preparing the Property for Sale

Step 4: Signing the Listing Agreement

Step 5: Marketing and Negotiating

Step 6: Completing the Sale

Step 7: Paying Broker's Commission

Termination of the Listing Agreement

Expiration

Mutual Agreement

Breach of Contract

Performance

Legal and Ethical Considerations in the Listing Agreement

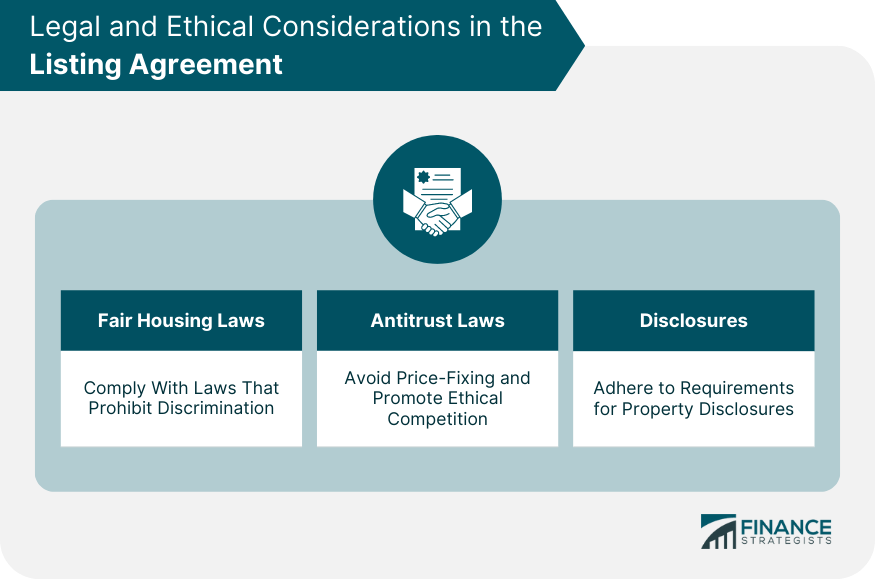

Fair Housing Laws

Antitrust Laws

Disclosures

Role of the Listing Agreement in IPOs

Common Issues and Disputes in Listing Agreements

Misrepresentation or Fraud

Breach of Fiduciary Duty

Commission Disputes

Resolving Disputes in Listing Agreements

Negotiation

Mediation

Arbitration

Litigation

Final Thoughts

Listing Agreement FAQs

Typically, a listing agreement lasts 6 to 12 months but can be any length the seller and broker agree upon.

Yes, a listing agreement can be canceled before its expiration date, usually by mutual agreement of the seller and broker or due to a breach of contract by either party.

Typically, the seller pays the broker's commission from the property sale proceeds.

If the property doesn't sell within the term of the listing agreement, the contract usually expires, and the seller can choose to relist the property, possibly with a different broker.

Technology is increasingly important in the listing agreement process, from online property listings to digital signatures and document management. Future technologies like blockchain and virtual reality may further transform the process.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.