A share repurchase or a stock buyback is a corporate action wherein a company reacquires its shares from the marketplace. This reduces the number of outstanding shares, making each remaining share represent a larger slice of corporate ownership and thus more valuable. Companies perform share repurchases for a variety of reasons, such as capital structure optimization, returning excess cash to shareholders, or increasing earnings per share. A company can fund its buybacks with accumulated profits, new debt issuance, or existing cash reserves. By buying back its shares, a company can reinvest in itself, reallocating its capital back into the business. This can result in an increase in share prices as the demand for the stock increases, enhancing the wealth of the remaining shareholders. An open market repurchase is a method where a company buys back its own shares on the open market over an extended period. The company decides the timing and the amount of shares to repurchase, usually guided by the price of the stock. Open market repurchases are the most common form of share buybacks. The main advantage of this method is its flexibility - the company can alter the pace of the repurchase based on prevailing market conditions and its financial situation. In a fixed price tender offer, the company announces that it will repurchase a certain number of shares at a specific price, usually a premium to the current market price. Shareholders can then decide to 'tender' their shares, selling them back to the company. This method allows a company to repurchase a significant portion of its shares in a short period. However, it can be more costly than an open market repurchase due to the premium paid and the associated administrative costs. In a Dutch auction tender offer, the company announces a range of prices at which it is willing to buy back shares. Shareholders can decide how many shares they want to tender and at which price within the range. Once the tender period ends, the company determines the lowest price within the range that would enable it to buy the number of shares sought in the offer. All shares tendered at or below this price are bought at the same price. The Dutch auction allows the market to set the repurchase price, potentially making the process more efficient and fair to shareholders. The first step in the share repurchase process involves obtaining authorization from the company's board of directors. A repurchase of shares cannot happen without the board's approval as it fundamentally changes the company's capital structure. The board's resolution specifies the maximum number of shares to be repurchased and provides a broad outline of the method to be used. However, it does not obligate the company to repurchase any specific number of shares. Following the board's approval, the company announces its plan to repurchase shares. The announcement typically includes the number of shares to be repurchased, the method of repurchase, and the reasons behind the decision. The announcement often leads to a positive reaction in the stock market, driving up the share price. This is because the market perceives the repurchase as a signal of the company's confidence in its future prospects. After the announcement, the company can begin executing the share repurchase. In an open market repurchase, the company's broker will buy shares on the open market over a period, usually guided by a rule-based plan to avoid market manipulation. In a tender offer, either fixed price or Dutch auction, the company announces the offer to shareholders and provides a window of time during which they can tender their shares. At the end of this period, the company repurchases the tendered shares at the specified price or the determined price in a Dutch auction. When a company buys back its shares, it reduces the number of shares outstanding. This increases the company's EPS, all else being equal, making the company appear more profitable on a per-share basis. Repurchasing shares to boost EPS is particularly appealing for companies during periods of stagnant earnings growth. By reducing the denominator in the EPS calculation, the company can increase its EPS without increasing its net income. Companies with significant cash reserves might choose to repurchase shares if they do not have other profitable investment opportunities, or if they believe their shares are undervalued. A share repurchase can be an effective way to return cash to shareholders. Unlike dividends, which are taxed as income, share repurchases are taxed at the typically lower capital gains rate, making them a tax-efficient way to distribute cash. Share repurchases are also a method of returning capital to shareholders. In addition to dividends, share repurchases are a way to distribute profits back to investors, demonstrating the company's commitment to shareholder value. When a company buys back its shares, the remaining shares represent a larger slice of the company, effectively increasing the value of each share. This can benefit shareholders by pushing up the share price, assuming market conditions remain constant. By buying back its own shares, a company can reduce the number of shares available for purchase in the open market, making it more difficult for a potential acquirer to gain a controlling stake. The repurchase also sends a signal to the market that the company believes its shares are undervalued, potentially deterring potential acquirers. However, this tactic can be costly and could lead to an over-leveraged balance sheet if the company borrows money to finance the repurchase. Cash financing involves the use of a company's available cash or cash equivalents to fund the share repurchase. This method is typically employed when the company has ample cash reserves and few high-return investment opportunities. Using cash to finance a share repurchase signals that the company is financially healthy, which can boost investor confidence and potentially lead to a higher share price. However, it's important for the company to maintain a balance and ensure it retains enough cash for operational needs and unforeseen expenses. In debt financing, the company borrows money to repurchase its shares. This could involve issuing corporate bonds or taking out a bank loan. Debt financing allows a company to buy back its shares without depleting its cash reserves. However, taking on debt increases the company's leverage and its financial risk. If the company's earnings are insufficient to cover the interest payments on the debt, it could face financial distress or even bankruptcy. Equity financing, in the context of share repurchases, involves the issuance of a new class of shares or securities, such as convertible bonds or preferred shares. The proceeds from the issuance are then used to repurchase the common shares. This method can be complicated and costly due to the associated legal and administrative expenses. Additionally, issuing new securities can lead to dilution of ownership for existing shareholders if the new securities are later converted to common shares. Share repurchases often lead to an increase in the company's share price. When a company announces a share repurchase, it signals to the market that it believes its shares are undervalued. This can boost investor confidence and drive up the share price. Moreover, the act of buying back shares increases the demand for the stock, which can push up the price. The increase in share price can be particularly beneficial for shareholders who choose not to sell their shares back to the company. Contrary to the dilutive effect of issuing new shares, share repurchases have a 'concentrating' effect on ownership. By reducing the number of shares outstanding, a repurchase increases the proportionate ownership of each remaining shareholder. This means that each share represents a larger slice of the company, increasing the value of each share. However, this also means that the shareholders who sell their shares to the company give up their future rights to the company's earnings. Share repurchases can have a significant impact on a company's financial ratios. They can increase the company's earnings per share and return on equity by reducing the number of shares outstanding. At the same time, if the company borrows money to finance the repurchase, it can increase its debt-to-equity ratio, signaling a higher financial risk. Moreover, repurchasing shares reduces the company's cash reserves, which can lower its current and quick ratios, potentially indicating a weaker liquidity position. From a tax perspective, share repurchases can be more advantageous for shareholders than dividends. While dividends are taxed as ordinary income, the proceeds from a share repurchase are taxed as capital gains, which usually have a lower tax rate. However, the tax implications of a share repurchase can vary based on the shareholder's tax situation and the jurisdiction's tax laws. Therefore, shareholders are advised to consult with a tax professional before deciding to participate in a share repurchase. Executives, whose compensation often includes stock options or shares, may be tempted to boost the short-term stock price at the expense of long-term corporate health. In addition, the pressure to meet earnings per share targets can lead to an over-reliance on share repurchases, potentially diverting capital away from long-term investments or from retaining a cash buffer for economic downturns. Rather than investing in research and development, employee training, or other growth opportunities, companies might opt to repurchase shares, which offers a more immediate boost to the stock price. Moreover, companies may end up repurchasing shares when the price is high, only to see the price fall later, implying that the capital could have been better invested elsewhere. Another criticism of share repurchases is that they often occur when the company's stock price is high, not when it is low. This is counterintuitive since companies should ideally buy low and sell high. The timing of share repurchases can be influenced by external pressures, such as the need to meet earnings per share targets or to make use of excess cash. However, buying back shares at a high price reduces the value gained from the repurchase and could lead to a destruction of shareholder value if the stock price later falls. Finally, critics argue that share repurchases can discourage companies from making necessary investments. Since repurchases provide a quick way to boost the stock price, companies might opt for them instead of investing in new projects, products, or markets. This focus on repurchasing shares rather than investing in the business can hinder a company's long-term growth and innovation. Therefore, it's crucial for companies to strike a balance between returning capital to shareholders and investing in future growth. A share repurchase is a corporate action where a company buys back its own shares from the open market or through tender offers. Companies engage in share repurchases for various reasons, such as to return capital to shareholders, improve earnings per share, utilize excess cash, or defend against hostile takeovers. There are different types of share repurchases, including open market repurchases, fixed price tender offers, and Dutch auction tender offers. The choice of method depends on various factors such as the company's financial situation, the share price, and the desired speed of the repurchase. The process of share repurchase involves obtaining authorization from the board of directors, announcing the repurchase plan to the public, executing the repurchase, and finally reducing the number of outstanding shares. While they can boost earnings per share and return on equity, they can also increase the company's financial risk if funded by debt. Moreover, share repurchases have tax implications for both the company and the shareholders.What Is Share Repurchase?

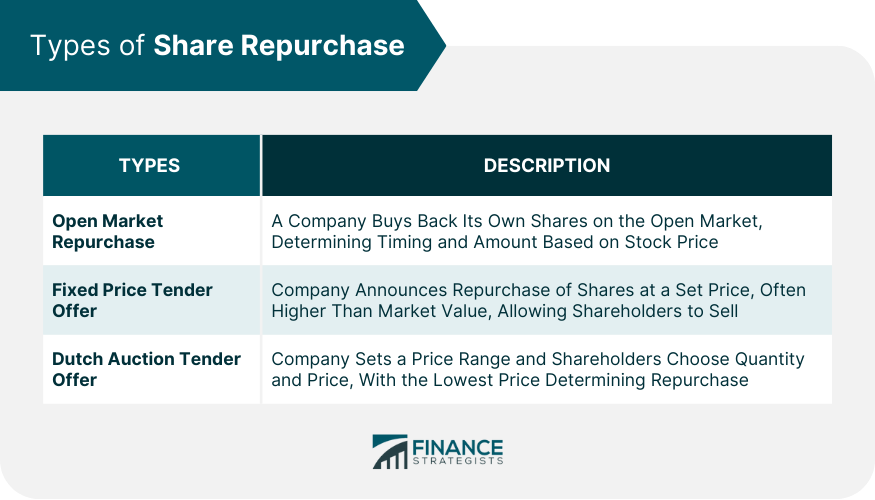

Types of Share Repurchase

Open Market Repurchase

Fixed Price Tender Offer

Dutch Auction Tender Offer

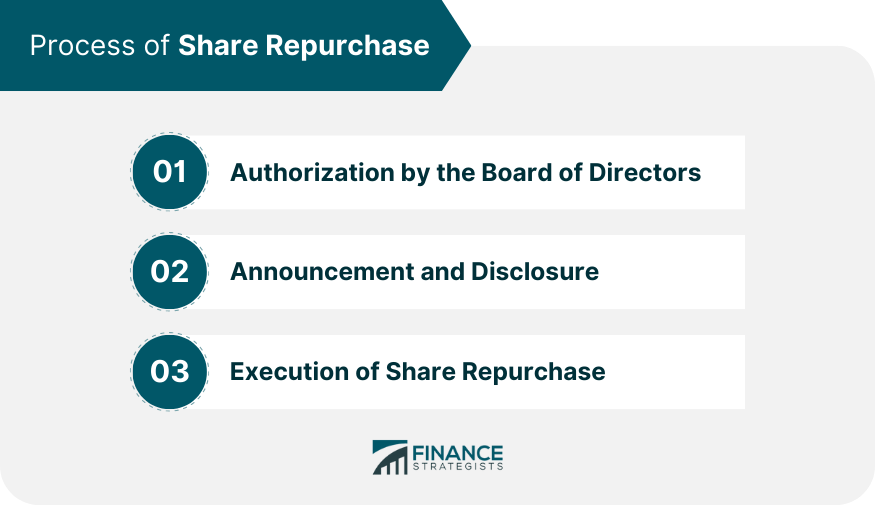

Process of Share Repurchase

Authorization by the Board of Directors

Announcement and Disclosure

Execution of Share Repurchase

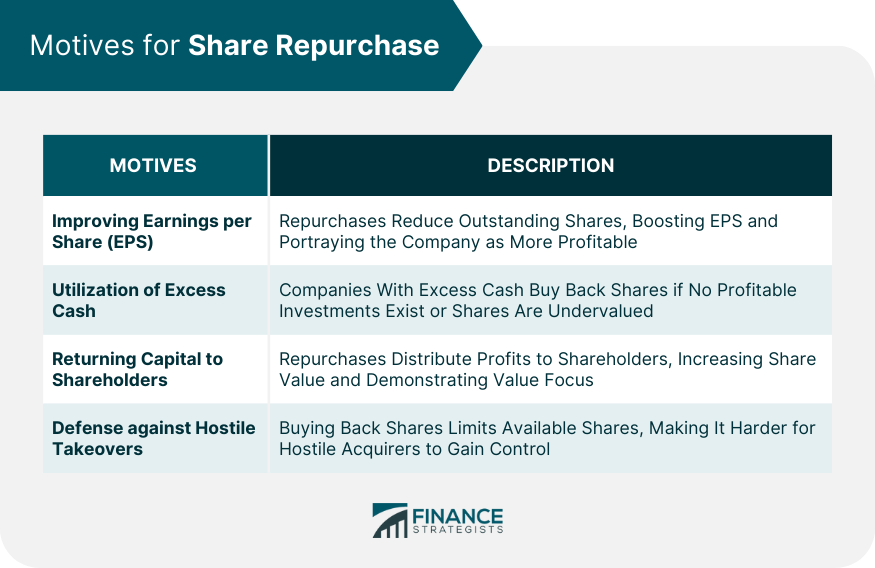

Motives for Share Repurchase

Improving Earnings per Share (EPS)

Utilization of Excess Cash

Returning Capital to Shareholders

Defense Against Hostile Takeovers

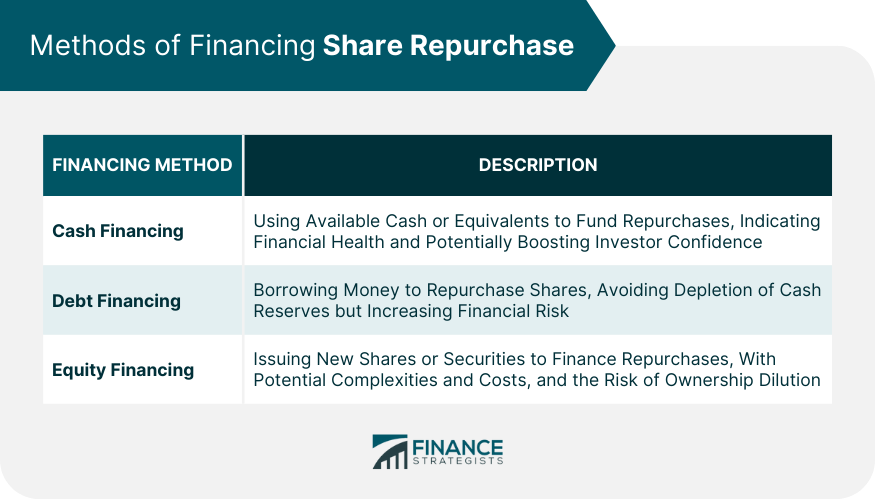

Methods of Financing Share Repurchase

Cash Financing

Debt Financing

Equity Financing

Impact of Share Repurchase

Effects on Share Price

Dilution of Ownership

Impact on Financial Ratios

Tax Implications

Criticisms of Share Repurchase

Short-Term Focus

Misallocation of Capital

Market Timing Concerns

Lack of Investment

Conclusion

Share Repurchase FAQs

A share repurchase, or a stock buyback, is a corporate action wherein a company reacquires its shares from the marketplace.

Companies repurchase shares to return capital to shareholders, improve earnings per share, utilize excess cash, or defend against hostile takeovers.

The main types of share repurchases are open market repurchases, fixed price tender offers, and Dutch auction tender offers.

A share repurchase can increase a company's earnings per share and return on equity by reducing the number of shares outstanding. If the repurchase is funded by debt, it can increase the company's debt-to-equity ratio.

Critics argue that share repurchases can encourage a short-term focus, lead to a misallocation of capital, raise concerns about market timing, and discourage necessary investment.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.